While mostly overlooking a dense economic calendar last week, investors

were forced to base their trading behavior on breaking news headlines

and events. Mortgage rates benefited from a "flight to safety", but it

was a roller coaster ride. There were large spikes and big drops. An

abundance of chaos if you will. Much of the storyline has yet to

develop in Japan, Northern Africa, and the Middle East. Thus we'd expect

breaking headline news to dictate the direction of mortgage rates this

week too.

Equity futures rose sharply overnight as Japanese emergency forces were able to restore power to nuclear plants, prompting the Prime Minister to speak of "light at the end of the tunnel."

S&P 500 futures are 14.75 points higher at 1,289.00 and Dow futures are 112 points higher at 11,911

"Continued signs of progress in cooling Japan's nuclear reactors and news that some Japanese factories are resuming production have U.S. equity futures pointing to a strong open and Treasuries on the defensive," said economists at BMO Capital Markets.

The 10-year Treasury is yielding 3.303%, or 3.3 points higher than Friday's closing yield of 3.28%. The 2s/10s curve is UNCH at 268bps wide. And the FNCL 4.5 MBS coupon is -2/32 at 102-11.

While civil war looms in Libya, light crude oil is 1.90% higher at $103 per barrel. Gold prices are higher too - up 1.09% at $1,431.70 per ounce.

Analysts say equities could also be receiving a nice boost from AT&T's surprise move to buy T-Mobile USA from Deutsche Telekom for a cool $39 billion.

"The new combined entity, if it can garner regulatory approval, will be largest carrier in the U.S. by leaps and bounds," reports CNN. "AT&T and T-Mobile USA combined have over 25% more subscribers now than Verizon (125+ million vs. 93+ million)."

AT&T shares have fallen 2.21% in the past month but are up 0.72% in early morning trading. Rivals are mixed: Sprint is down 0.20% but Verizon stock is up 1.44%.

Key Events This Week:

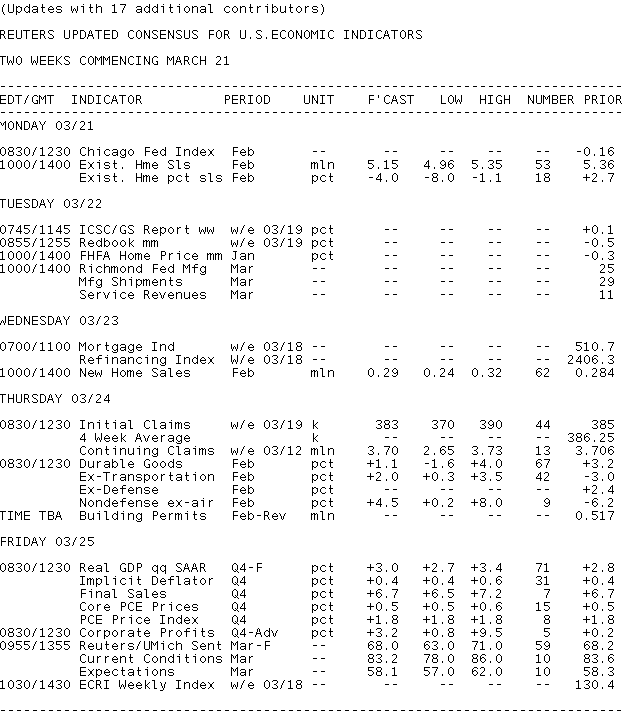

Monday:

10:00 - Housing market weakness is anticipated to be a theme of this week, beginning with Existing Home Sales. The pace of already-lived in home sales is forecast to decline 4% to an annualized rate of 5.15 million units in February, say economists polled by Reuters. The decline would reverse a 2.7% rise in January. Predictions are largely based on the pending home sales index, which fell 3.2% in December and 2.8% in January.

"The market for existing homes remains depressed," said economists at IHS Global Insight. They point out the MBA purchases index declined nearly 8% in February and predict a worse-than-consensus 7% drop in existing homes.

"The published data show existing home sales up 39% from July 2010 to January 2011, but the figures remain suspect," they added. "Data compiled by Core Logic, a company that also tracks home sales, indicated that the National Association of Realtors' existing home sales numbers were too high by as much as 20%. The NAR says that it is studying the issue and that it may put out revised numbers later this year."

Economists at Janney Capital Markets point out that weather might be playing a negative part in the slowing pending and likely declining existing sales data.

"The 30 - 60 day lag time between home purchase and closing suggests that February's numbers will be impacted by inclement weather in late December into January," they wrote in a weekly note. "Underlying housing market fundamentals remain somewhat iffy, as exemplified by high foreclosure rates (4.63% of all loans in 4Q 2010 was highest on record), still-falling home prices (Case-Shiller prices fell 0.9% in December), and weak consumer incomes."

Tuesday:

8:00 - Susan Pianalto, president of the Cleveland Fed, speaks on the economy in 2011 and beyond to the University of Akron Economic Summit.

10:00 - A consensus of forecasts isn't available for January's FHFA House Price Index, but the index fell 0.3% in December and there's no reason to expect a rebound just yet. A better measure could be Monday's existing home sales index, which includes prices.

Wednesday:

9:00 - Federal Reserve Chairman Ben Bernanke speaks on "Community Banking in a Period of Recovery and Change" before the Independent Community Bankers of America National Convention and Techworld, Audience Q&A expected.

10:00 - Can New Home Sales recover after declining to one of the lowest levels on record? That's the question the market faces after the index dropped 12.6% in January to an annualized pace of 284,000. The consensus looks for a slight increase to 290k in February, but predictions are wide, ranging from 240k to 305k.

The market will also look at number of unsold new homes, which fell to 188,000 units last month - the lowest since late 1967.

"The new home sales numbers are jumpy, subject to revisions, and not well estimated," said economists at IHS Global Insight. "We recommend focusing on recent trends rather than on the latest monthly estimates. A three-month moving average shows new home sales still stuck at the bottom, with sales starting to pick up in the West, stuck at the bottom in the South, but still declining in the Northeast and Midwest."

They added that poor housing permits figures indicate the sector "remains stuck at the bottom, and we project no change in new home sales this month."

Economists at Nomura Global Economics are more optimistic with a forecast of +7.4%.

"That view is consistent with the two-point rise in the present single-family house sales component of the NAHB housing market index in February," they added. The NAHB index rose to 17 from 15.

Thursday:

8:30 - New Orders for Durable Goods are anticipated to climb a robust 1.5% in February. The January index took flight with a 2.7% increase led by civilian aircraft orders. That helped break a three-month downward trend, yet excluding transportation the pace of new orders actually fell 3.6% in month. Orders for equipment fell 14.4%, machinery dropped 13.0% and computer orders declined 9.6%.

"As overall durable goods data were distorted by a big jump in aircraft orders in January, a better indicator of underlying behavior is orders ex-transportation, which we expect to have expanded by 1.2% in February," said economists at Nomura Global Economics, who look for a 0.1% increase overall. "The new orders component of February's ISM manufacturing index, which reached its highest level since January 2004, supports our positive outlook."

Aircraft orders are expected to improve for a second month, following a dismal December reading, said economists at IHS Global Insight.

"The underlying trend for durables orders remains strongly upwards, as indicated in all major national and regional surveys of manufacturers," they added.

Janney Capital Markets had mixed forecasts on various categories, with higher industrial metals prices driving primary and fabricated metals orders upward during the month.

"The biggest headwind we see for durables orders is a brief slowdown in goods exports in January," they said. "Our modeling suggests [this] will limit orders' expansion in February, though the impact is likely to be short lived, especially given impressive prospects for developing market demand for capital goods."

8:30 - Initial Jobless Claims are expected to register at 385,000 for the second week in a row, after falling by 16k in the prior week. The current four-week average is 386k - the lowest since July 2008. Economists at BTMU say these strong figures suggest private payroll growth of +200k.

"There has been a downward trend in claims since the start of 2010," economists at BTMU said, adding that the trend has been obscured because of holiday and weather distortions from November through January.

11:00 - Treasury announces the terms of 2-year, 5-year, and 7-year debt auctions to be held next week.

Treasury Auctions

1:00 - 10-Year TIPS

Friday:

5:00 - Narayana Kocherlakota, president of the Minneapolis Fed, speaks on bubbles and unemployment to an Idep-Institut D'Economie Publique conference in Paris.

8:30 - GDP growth is forecast to rise one-tenth to 2.9% in the third and final look at the fourth-quarter. New data suggests higher growth in inventories and faster growth in consumer spending, but neither is strong enough to bring GDP back to its first estimate of 3.2%.

"Although the international trade report indicates a larger trade gap and therefore slower economic growth, better-than-expected business investment and wholesale inventories point to a slight upward revision to 4Q10 estimate," said analysts at BBVA, predicting a 3% figure.

9:15 - Dennis Lockhart, president of the Atlanta Fed, speaks on the economic outlook to the Bonita/Estero Market Pulse Conference in Ft. Myers, Florida.

9:55 - Consumer Sentiment isn't expected to recover from the sharp drop seen in the mid-March reading. The Reuter's/University of Michigan index fell to 68.2 from a late February level of 77.5 as gasoline prices shot past $100 per barrel. What has improved consumers position in the past two weeks? Not much. The index is anticipated to slide to 68.0, and that looks optimistic.

"Gasoline prices have edged a bit higher, and the Japanese earthquake has introduced new uncertainties and has hurt global stock markets," said economists at IHS Global Insight. We expect the final sentiment reading to dip a bit further, to 67.0 from the preliminary 68.2."

Note that in the mid-March reading, expectations drove the decline with a 13.3 point drop-off to 58.3, while the current conditions component fell 3.3 points to 83.6.

12:15 - Charles Plosser, president of the Philadelphia Fed, speaks on a framework for long-run monetary policy to the Shadow Open Market Committee in New York.

CURRENT GUIDANCE: We're still very much "stuck" at a 4.875% best execution rate, but borrowers with long term outlooks or who are otherwise not in an urgent need to obtain a loan can afford to wait to see if rates become "unstuck" in a friendly direction. It's still something we see as possible. Short term outlooks or those who must lock soon regardless of market movements are in a different position, however. Any time rates are near their best levels in over a month and you have to make a lock decision soon, risks are heavily in favor of locking. Especially in this environment driven by headline news. More volatility, less certainty = more reason to be defensive.