Mortgage rates got slightly more expensive today. Best-execution rates were unchanged.

It was a quiet session overall. Little movement was seen in the secondary mortgage market. Stocks started strong, bonds opened weak. Both then reversed course and meandered back toward unchanged levels on the day. It was a quiet day. The slowdown wasn't unwelcome though....

While mostly overlooking a dense economic calendar this week, investors were forced to base their trading behavior on breaking news headlines and events. Mortgage rates benefited from a "flight to safety", but it was a roller coaster ride. There were large spikes and big drops. An abundance of chaos if you will. The market needed a break. And we think that break began yesterday, on St.Patrick's Day. It won't last long though. Much of the storyline has yet to develop in Japan, Northern Africa, and the Middle East. Thus we'd expect breaking headline news to dictate the direction of mortgage rates next week too.

-------------------------

A flight to safety happens when investors are nervous about owning risky assets like stocks, but do not want to miss out on earning a return on their funds, so they allocate their money into risk-free government guaranteed U.S Treasury debt to provide a safe-haven AND an investment return. As benchmark Treasury yields fall on "flight to safety" buyer demand, prices of mortgage-backed securities move higher in unison. This allows lenders to reprice their rate sheets for the better and gives originators an opportunity to offer fence-sitting borrowers lower mortgage rates or more competitive closing costs.

CURRENT MARKET: The "Best Execution" conventional 30-year fixed mortgage rate is BACK to 4.875% after falling to 4.75% on Wednesday (not universally, but in some cases). For those looking to permanently buy down their rate to 4.75%, this quote carries higher closing costs but given the recent availability of 4.75% as a Best Execution rate, these costs may be lower than they previously were. Still, the upfront cost of permanently buying down your rate to 4.75% is not worth it to every applicant, we would generally only advise the permanent floatdown if you plan to keep your new mortgage outstanding for longer than the next 10 years. Ask your loan officer to run a breakeven analysis on any origination points they might require to cover permanent float down fees. On FHA/VA 30 year fixed "Best Execution" is back to 4.75%. 15 year fixed conventional loans are best priced at 4.125%. Five year ARMS are best priced at 3.50%, but there is much more stratification in this sector with higher or lower rates making equally as much sense depending on the lender and on the amount of time you intend to keep the loan.

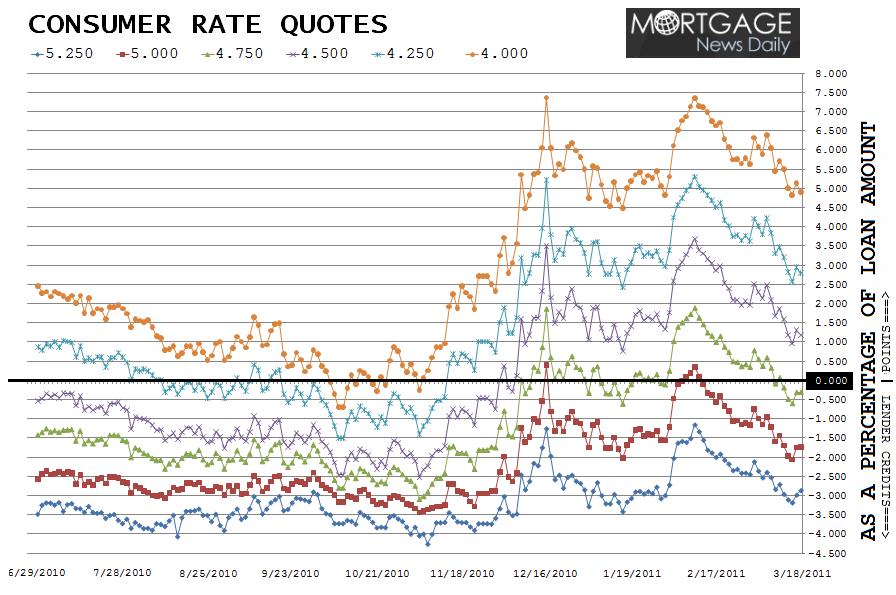

To illustrate the recent behavior of mortgage rates, we offer the chart below. It graphs the average origination closing costs associated with specific mortgage note rates as quoted by the five major mortgage lenders.

If the note rate line is moving up, the closing costs associated with that rate quote are rising. In December, closing costs rose rapidly. Mortgage rates did improve from those levels, but then moved sideways for 7-weeks. And then the range broke following the January Employment Situation Report and consumer rate quotes rose back to their December highs. As one can see, borrowing costs have steadily improved since then but have more recently run into a wall near one-month lows. 4.75 is on the brink of being back in the game for consumers but hasn't been able to sustain a break below the 0.00% barrier since early December. We've run into resistance! Again!!

Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis are the origination closing costs, as a percentage of your loan amount, that a borrower would be required to pay in order to close on that note rate. If the note rate graph line is below the 0.00% marker, the consumer may potentially receive closing cost help from their lender in the form of a lender credits. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown costs and origination fees. PLEASE SEE OUR MORTGAGE RATE DISCLAIMER BELOW

LAST FRIDAY'S GUIDANCE: The failure of the bond market to extend its recent rally really serves to drive home a point we've been harping on for several weeks now: WE'RE STUCK. If you're floating, you're doing so for marginal improvements in UPFRONT COSTS ....not RATE. See disclaimer below please. When it comes to the outlook for lower rates in the months ahead, we're still optimistic about that expectation but realize it will require a steady drip of bond friendly (economy-unfriendly) news and events . In the short-term, or at least until "the levy breaks" and all hell breaks loose around the planet, we don't expect lender rate quotes to look much better than they do right now.

CURRENT GUIDANCE: Still very much "stuck" at a 4.875% best execution rate, but borrowers with long term outlooks or who are otherwise not in an urgent need to obtain a loan can afford to wait to see if rates become "unstuck" in a friendly direction. It's still something we see as possible. Short term outlooks or those who must lock soon regardless of market movements are in a different position, however. Any time rates are near their best levels in over a month and you have to make a lock decision soon, risks are heavily in favor of locking. Especially in this environment driven by headline news. More volatility, less certainty = more reason to be defensive.

READ MORE: Mortgage Pricing Hits Wall. Loan Demand Declines...

"Best Execution" is the most efficient combination of note rate

offered and points paid at closing. This note rate is determined based

on the time it takes to recover the points you paid at closing

(discount) vs. the monthly savings of permanently buying down your

mortgage rate by 0.125%. When deciding on whether or not to pay points,

the borrower must have an idea of how long they intend to keep their

mortgage. For more info, ask you originator to explain the findings of

their "breakeven analysis" on your permanent rate buydown costs.

Important Mortgage Rate Disclaimer: The "Best Execution" loan pricing

quotes shared above are generally seen as the more aggressive side of

the primary mortgage market. Loan originators will only be able to offer

these rates on conforming loan amounts to very well-qualified borrowers

who have a middle FICO score over 740 and enough equity in their home

to qualify for a refinance or a large enough savings to cover their down

payment and closing costs. If the terms of your loan trigger any

risk-based loan level pricing adjustments (LLPAs), your rate quote will

be higher. If you do not fall into the "perfect borrower" category, make

sure you ask your loan originator for an explanation of the

characteristics that make your loan more expensive. "No point" loan

doesn't mean "no cost" loan. The best 30 year fixed conventional/FHA/VA

mortgage rates still include closing costs such as: third party fees +

title charges + transfer and recording. Don't forget the intense fiscal

frisking that comes along with the underwriting process.