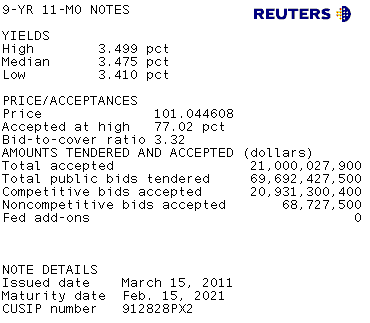

Treasury just sold $21 billion 10-year notes. The auction went well....

The bid to cover ratio, a measure of auction demand, was an above average 3.32 bids submitted for every 1 accepted by Treasury. This is the highest bid to cover ratio since April 2010 (3.72). 77% of the issue was awarded at the high-yield of 3.499%, which was almost 2bps below the 1pm "When Issued" yield. That is an indication of strong demand.

Indirect accounts were awarded 53% of the competitive bid and 75% of what they tendered, both metrics are above the ten auction average and in-line with the five auction average....but well below the outlier February award of 71.3%.

Directs took down 6.5% of the competitive bid and 19.7% of what they tendered. Both metrics were below average.

Dealers took care of the rest, adding $8.5 billion in new inventory or 40.5% of the competitive bid and 17.7% of what they bid on.

Plain and Simple: Demand was strong. Good 10-year note re-opening!

Market Reaction...

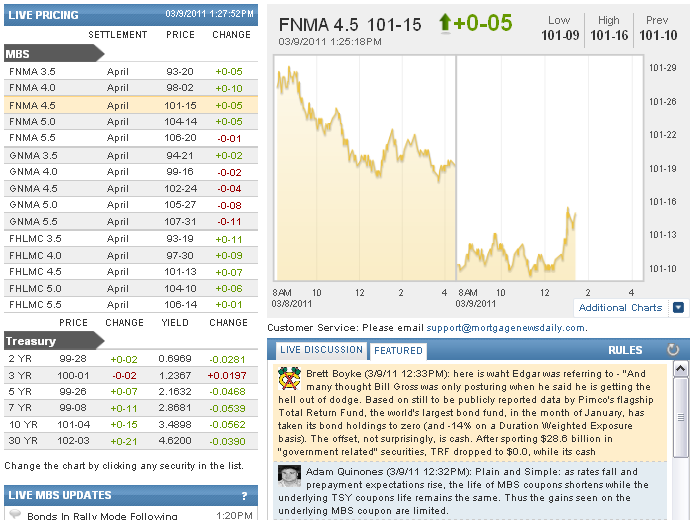

OTR benchmark 10s are hovering near the auction stop at 3.49%. This represents a 4bp improvement in yields vs. pre-auction marks.

The 2s/10s curve has broken 280bp resistance, likely as traders unwind steepeners before the long bond auction tomorrow. Let's hope that lasts and the curve retests spread resistance at 270bps wide.

FNCL 4.5 MBS coupons are +5/32 at 101-15. This breaks a tight sideways trading range and leaves "rate sheet influential" MBS coupons just off the intraday highs, which were established right after the auction results flashed.

On average among the five major lenders C30 loan pricing is 11.4bps better vs. yesterday's repriced offers. 4.875% is still Best Execution but note rates below 4.875 saw the largest rebate improvements. The cost to permanently buydown the borrower's rate from 4.875 to 4.75 is 1.02 points on average. That is extremely expensive as it would require the mortgagor keeping their note outstanding for 10+ years before recovering the upfront buydown fee. On a positive note, the spread between primary and secondary loan pricing tightened 7bps today. That implies lock desks lessened the amount of margin they have baked into rate sheets.

What does that tell us about the potential for reprices?

It means lenders have already priced aggressively relative to current MBS indications. So it's gonna take more rally before lenders award reprices for the better. Our target is 101-20 on C30 paper. That doesn't apply to all lenders though. These observations are made based on the loan pricing of the five major lenders. Regionals are a totally different story. Let us know if you hear of any rate sheet recalls.