Mortgage rates did bad yesterday.

Mortgage rates did real bad yesterday.

Some folks call it "capitulation", others refer to it as "liquidation". I will K.I.S.S and just say...it was REAL bad.

It was so bad that I didn't double check my loan pricing model...I triple checked it. I even called for a quote. (I love calling lenders and playing dumb. Watch out originators. I might get you)

In the end, the bad news was confirmed. Mortgage rates had a REAL BAD DAY. And it didn't get any better today. Loan pricing deteriorated further this morning as benchmark yields continued their seemingly relentless trek higher. The best par 30 year fixed mortgage rates are now in a tight range between 4.75% and 5.00%. There is a steep increase in borrowing costs below 4.75%.

Important Mortgage Rate Disclaimer: Loan originators will only be able to offer these rates on agency conforming loan amounts to borrowers who are have a middle FICO score over 740 and enough equity in their home to qualify for a refinance or a large enough savings to cover their down payment and closing costs. If the terms of your loan trigger any risk-based loan level pricing adjustments (LLPAs), your rate quote will be higher. If you do not fall into the "perfect borrower" category, make sure you ask your loan originator for an explanation of the characteristics that make your loan more expensive. "No point" loan doesn't mean "no cost" loan. The best 30 year fixed conventional/FHA/VA mortgage rates still include closing costs such as: third party fees + title charges + transfer and recordation + escrows (things like upfront MIP (if required), property taxes, homeowners insurance, accrued interest)".

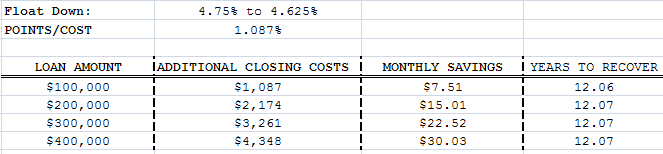

Looking at the situation from a more practical perspective, the buydown structure for loan pricing below 4.75% is officially unattractive for borrowers looking to float down their mortgage rate. Of the major lenders, the average cost to buy your note rate down from 4.75% to 4.625%....is 1.087% of your loan amount.

Below is a breakdown of the borrower's cost to float their 30 year fixed mortgage rate lower from 4.75% to 4.625%. I would only advise executing this float down if you are sure that you will still be paying on this same mortgage in 12.07 years. Otherwise it is not worth the increase in upfront closing costs.

Plain and Simple: There is a clear line of demarcation between 4.625% and 4.75%. If you are looking to close in the next 2 weeks...4.75% is your likely target. Very-well qualified borrowers should shoot for no points.