Mortgage brokers have apparently reclaimed both their reputations and their market share in recent years according to Archana Pradhan, a risk management analyst for CoreLogic. She writes in the company's blog that brokers' share of the conventional conforming mortgage market hit 16 percent earlier this year. While this is only half its share before the housing crisis when it accounted for about one-third of originations, it has doubled since 2011.

Mortgage brokers' reputation for loan quality took a substantial hit during and immediately after the crisis as foreclosure rates jumped. Their market share began to slip in 2008 as some lenders stopped offering credit through this channel. It had fallen to 7 percent by 2011. Now that their business is returning, Pradhan says their loans are performing well.

According to CoreLogic's Loan Performance Insights Report, the serious delinquency rate nationally, that is loans that are 90 or more days past due or in foreclosure, was 1.3 percent in July. This is down 0.6 point since the prior July. By comparison, that portion of loans originated by mortgage brokers had substantially lower rates, at least for those with loan to value ratios between 70 to 80 percent and debt-to-income ratios of 30 to 40 percent. That rate in July was 0.8 percent, down from 1.0 percent a year earlier. The rates are a 12-year low.

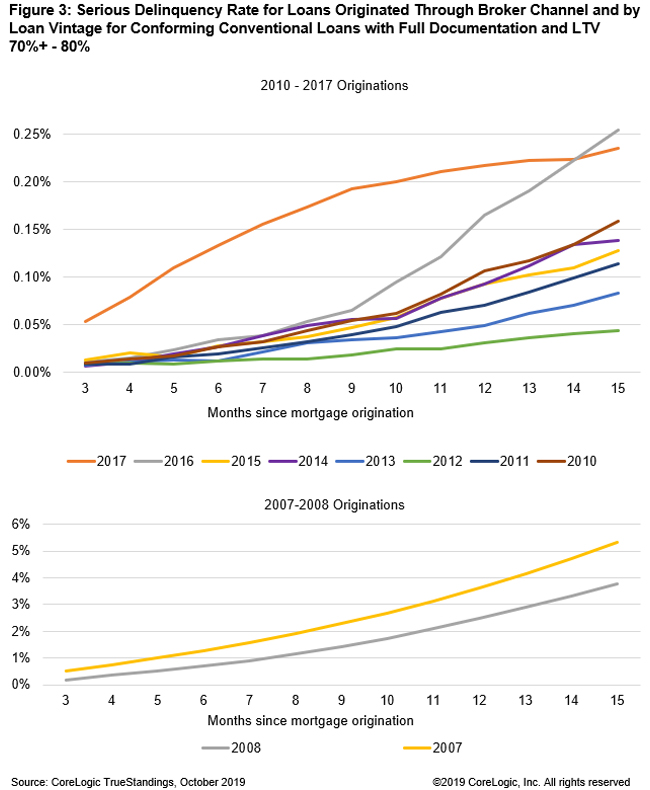

While rates are very low, they still don't reflect the higher quality of post-crash originations. The bulk of loans that are seriously delinquent today were originated between 2003 and 2009. The same applies to those loans originated by mortgage brokers; those older vintages account for about 70 percent of their seriously delinquent originations. Only 16 percent of their loans in that bucket were originated after 2010.

Figure 3 shows the performance of loans originated through the broker channel both just before the housing crisis and since 2010. While the delinquency rate crossed 2 percent within a year of loan closing in both 2007 and 2008, since 2010 delinquencies, even 15 months out, have remained fractional. It is, however, worth noting that delinquencies in the last two years pictured, 2016 and 2017, were significantly higher than in the previous six years.