Black Knight says that, amid all of the aid and stimulus provided to keep the economy rolling along during the pandemic, one aspect that doesn't get a lot of attention is refinancing. Black Knight points out in its current Mortgage Monitor that 14.3 million homeowners have refinanced since the beginning of the pandemic, 600,000 of them in each of the past four months. This puts the country on track for as many as 8.9 million refis this year, on top of the record 9 million in 2020.

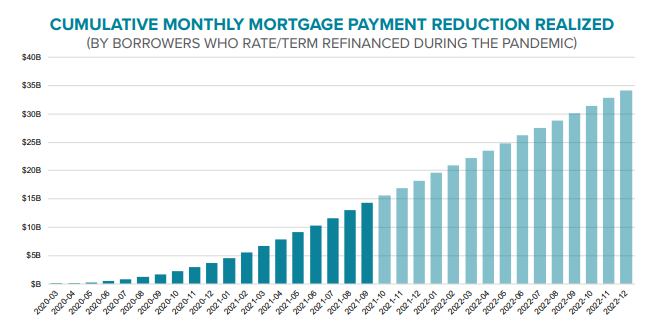

Due to record low interest rates, nine million of those refinances were of the rate/term variety, and homeowners who completed them saved an aggregate of $1.3 billion a month on their mortgage payments. Assuming these homeowners stay in their homes through the end of next year, the aggregate savings will rise to nearly $35 billion with the potential of saving nearly $16 billion per year thereafter. Those savings go back into the economy, permitting homeowners to buy cars, take vacations, or save for retirement.

And, as Ben Graboske, Black Knight's president of Data & Analytics says, "Keep in mind, that's on top of the $322 billion in equity that homeowners tapped via 5.5 million cash-out refinances during the same period.

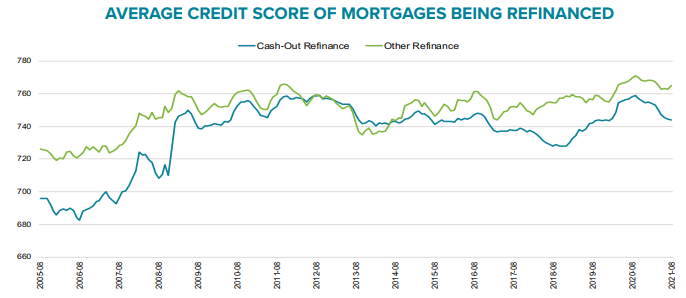

Historically, rate/term refinances have higher unpaid principal balances (UPBs) than cash-out refis, and typically have higher credit scores as well. Black Knight says it is common for credit scores to dip as rates rise because borrowers with high scores and high UPBs tend to act quickly when rates begin to fall, driving score up as they lock in low rates early in the cycle. Then both loan balances and scores drift lower as refi markets cool. The average score for rate/term refis has declined 6 points from its recent peak but is down 15 points for cash-out loans. Black Knight also notes that the average UPB of cash-out refinancers is $215,000, more than $100,000 lower than balances for rate/term refinances.

Rising interest rates in recent weeks have eliminated the refinance incentive for 3.4 million homeowners, but the company estimates there are still 11.5 million who could save .75 percent by refinancing. Still, the company expects the refinancing profile to change, shifting to a larger share of cash out transactions.

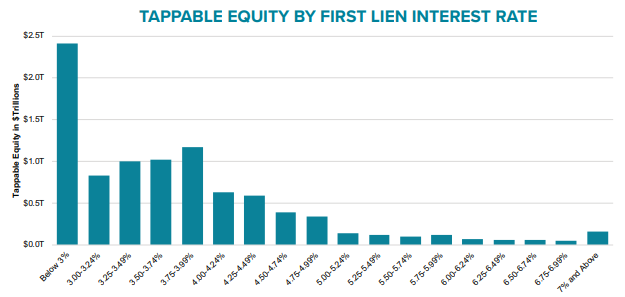

The company puts the tappable equity nationwide at an all-time high of $9.1 trillion. This is the amount of cash homeowners could extract from their homes without exceeding a loan-to-value ratio of 80 percent. Seventy percent of that equity is held by homeowners with credit scores of at least 760.

Also, a quarter of this equity belongs to borrowers who have interest rates below 3.0 percent, while more than half belongs to homeowners with rates above 3.5 percent. This means there is still plenty of cash-out lending opportunity. Further, in late 2018, when rates were near 5.0 percent, 70 percent of those completing cash-out refis accepted rate increases to do so, indicating some of the 11 million homeowners with sub-3 percent rates might still be refinance candidates.

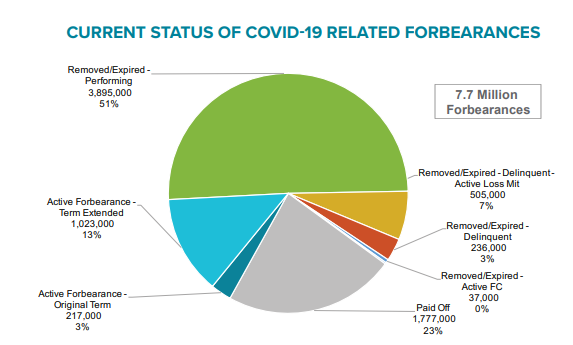

With more and more forborne homeowners nearing the end of their maximum permitted term, the Monitor also looked at the performance of those loans that have already left the program. Over the course of the pandemic, approximately 15 percent of all mortgage holders, 7.7 million, have participated in forbearance at some point and 1.3 million remain in active plans.

Eighty-four percent of all participants have exited their plans with 3.9 million borrowers or 51 percent of them reperforming on their loans. Another 23 percent have paid their loans off either through refinancing or selling their homes. Just over a half million of those formerly forborne borrowers remain in post-program loss mitigation although that number has jumped from 368,000 the prior month due to the large number of recent plan exits.

Of those 505,000 loans that remain in mitigation, 46 percent are FHA loans. This includes about three-quarters of the 165,000 FHA/VA loans that exited in early October. In contrast, only half of GSE (Fannie Mae and Freddie Mac) and one-third of Portfolio/PLS mortgages that left in October remain in loss mitigation. The distinction is due to both the large volume of recent FHA expirations and the elongated timeline for FHA workouts.

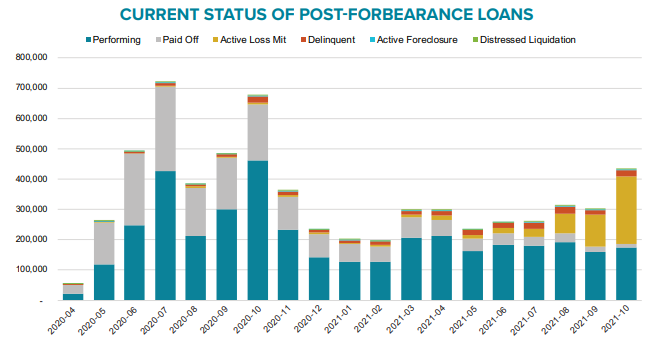

About 433,000 borrowers left forbearance during the first 19 days of October, the largest reduction since October 2020 when the first participants reached the 12 month point on their plans. Many of the October terminations were of borrowers who had reached the end of the 18 months of forbearance permitted. Black Knight says it will take time to fully assess how well those loans will perform but so far 40 percent are performing, and another 3 percent have been paid off.

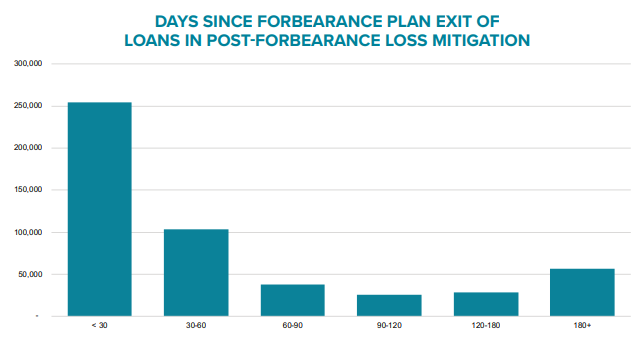

As to the universe of post-forbearance loans, only 3 percent of those who exited in 2020 are currently past due and, when all who have exited the program over its lifetime are included, that share is 12 percent. However, two-thirds of those delinquent homeowners are currently in loss mitigation.

There are, however, some disturbing signals. About half of those loans in active loss mitigation are those that have exited in the last 30 days and more that 100,000 mortgages that left the program more than 90 days ago remain delinquent and in mitigation. The company says this trend bears close attention given this lack of early success in returning to full performance.