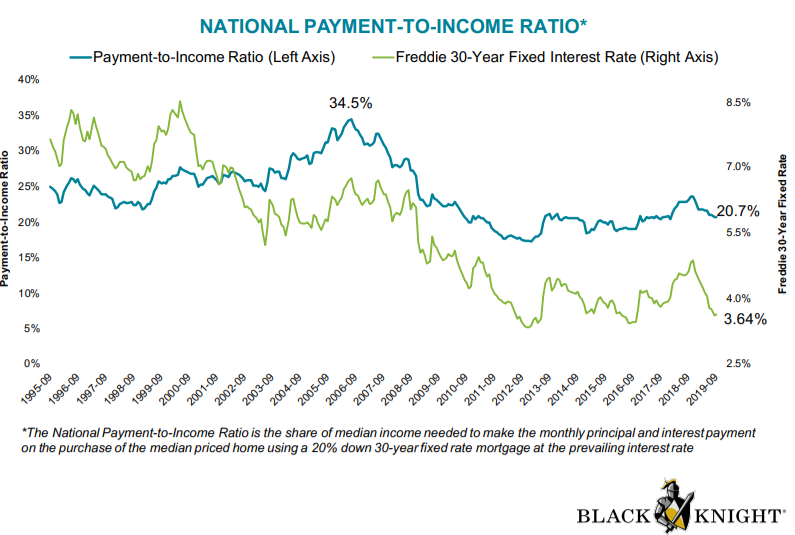

Even with home prices in most areas now well above their pre-Great Recession highs, affordability is not terribly low by historic measures. Black Knight, in its current issue of Mortgage Monitor, says, with the 30-year fixed rate in effect at the end of September, 3.64 percent, the principal and interest payments on an average priced home required 20.7 percent of the national median income. This was the second lowest payment to income (P&I) ratio in 20 months. It was a bit lower in early September when rates dipped briefly below 3.5 percent, sending affordability to a 32-month high.

Last November rates peaked near 5.0 percent and affordability hit a nine-year low with a P&I of 23.7 percent. This prompted a noticeable slowdown in home price appreciation. Since then, declining rates have brought the P&I payment down to $1,122, 4.5 percent below the long-term average from 1995 to 2003 and 10 percent lower than in November, even as home prices have increased by 4.0 percent. The new rate environment has boosted buying power by 16 percent or $46,000, while keeping monthly payments the same.

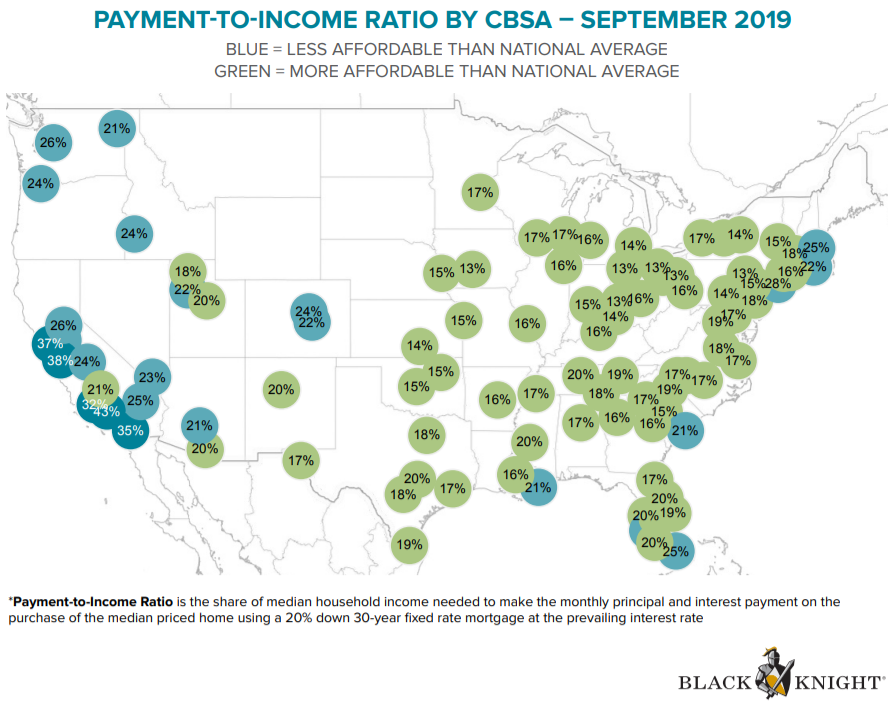

The increase in affordability has been broad based, but it is certainly not universal. Last November 11 states had become less affordable than their long-term averages, today only California and Hawaii remain in that category. Still, pockets of tight affordability remain, especially on the West Coast. California accounts for seven of the 10 least affordable markets in the nation with Los Angeles leading the list. Its P&I ratio in September was 42.9 percent, more than twice the national average, but down from 48.3 percent in November 2018 and from an outstanding 70.8 percent in July 2008 just before the housing crisis hit. San Jose is the second least affordable market at 37.9 percent followed by San Francisco, San Diego, and Honolulu, but affordability has improved by about 5 percentage points for all when compared to last November.

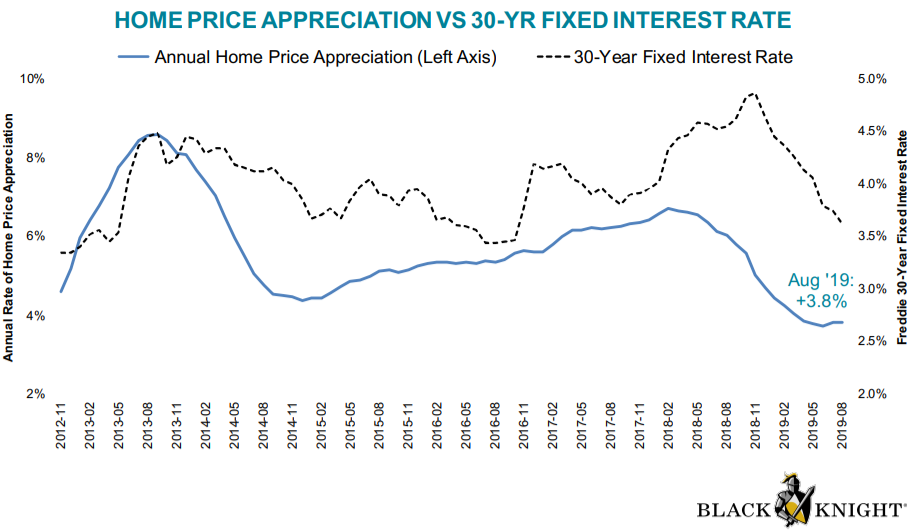

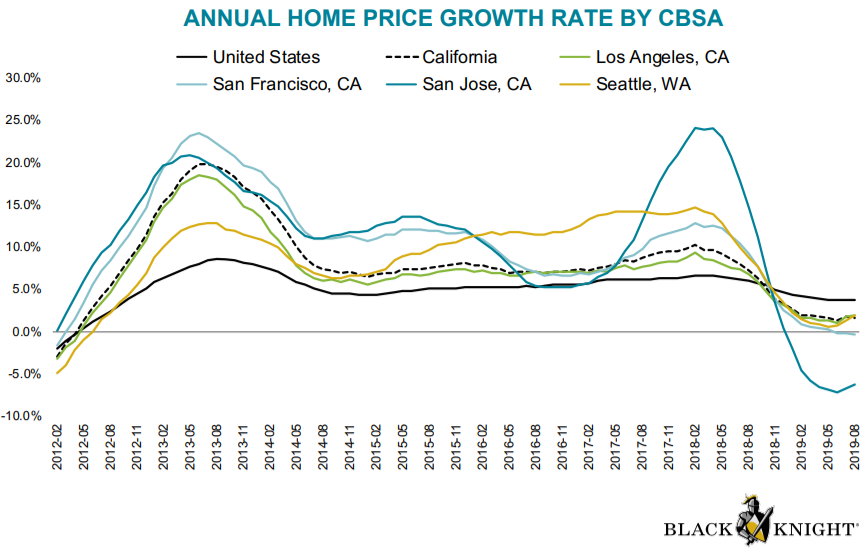

While home prices have continued to rise, declining affordability certainly has had a demonstrable impact on their growth. The annual appreciation rate in August was 3.8 percent, unchanged from July when it increased for the first time in 17 months. By the time July broke that streak prices had slowed to an annual rate of 3.7 percent, the lowest growth rate in nearly seven years.

The affordability/price growth relationship can be clearly seen by what has happened to areas that previously enjoyed the greatest appreciation once interest rates started to rise. California's growth slowed from an annual rate of 10.3 percent in early 2018 to just 1.3 percent this past July while San Jose, Seattle, and San Francisco fell from the among the 10 fastest appreciating market to among the 10 lowest. In fact, San Francisco and San Jose were the only markets to post actual annual price pull-backs in August.

Black Knight Data & Analytics President Ben Graboske said, "Despite falling interest rates and steadily improving affordability over the preceding eight months, annual home price growth held flat in August. It remains to be seen if this is merely a lull in what could be a reheating housing market, or a sign that low interest rates and stronger affordability may not be enough to muster another meaningful rise in home price growth across the U.S. That the strongest gains in - and strongest levels of - affordability were in August and early September could bode well for September/October housing numbers.

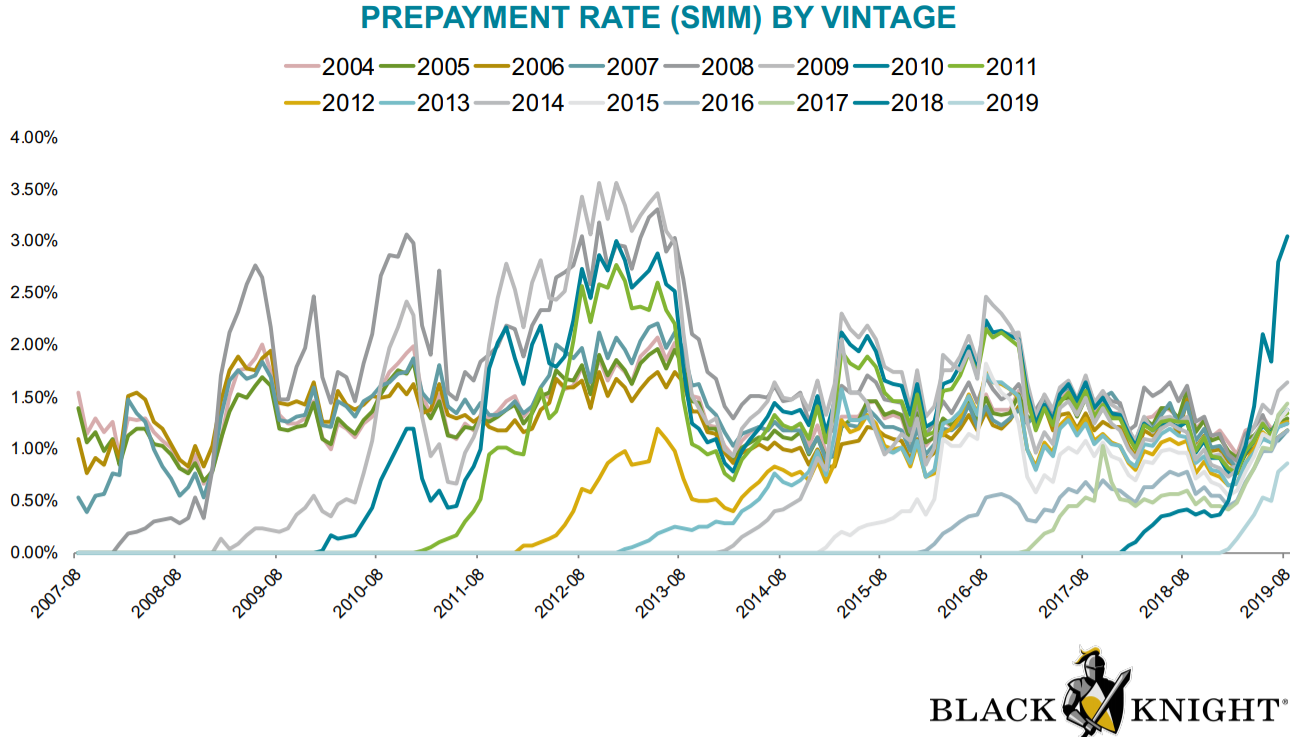

The Monitor also updates figures on mortgage prepayments and the pool of eligible refinance candidates in light of the volatile mortgage rates. Both stats have risen in six of the last seven months. Prepayments have continued to increase with the largest gains among FHA and VA mortgages which were up 8 percent and the 2018 vintage of loans which rose by 9 percent. There was also a 7 percent jump in prepays among borrowers with mid-range (620 to 679) credit scores.

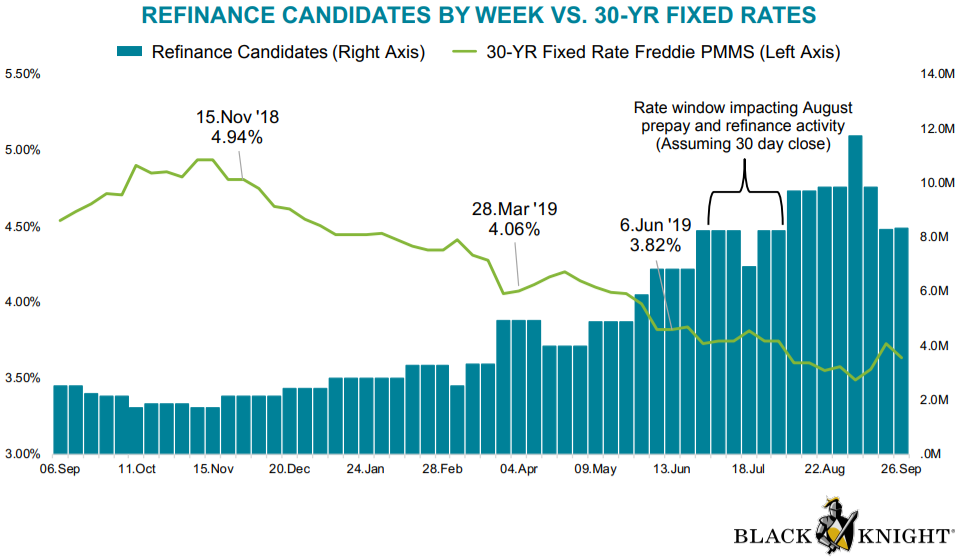

The company says that, assuming a 30-day window from application to closing, there appears to have been, throughout July, an average of 7.9 million homeowners who could both qualify for and benefit from refinancing, up 10 percent from the June number. In August the number of refinance candidates (which one would expect to drive prepayments in September) rose by nearly 20 percent to 9.46 million and hit a peak of 11.7 million in early September when rates fell below 3.50 percent. Rates jumped over the next two weeks, reducing the refinance pool to 8.36 million by September 26.

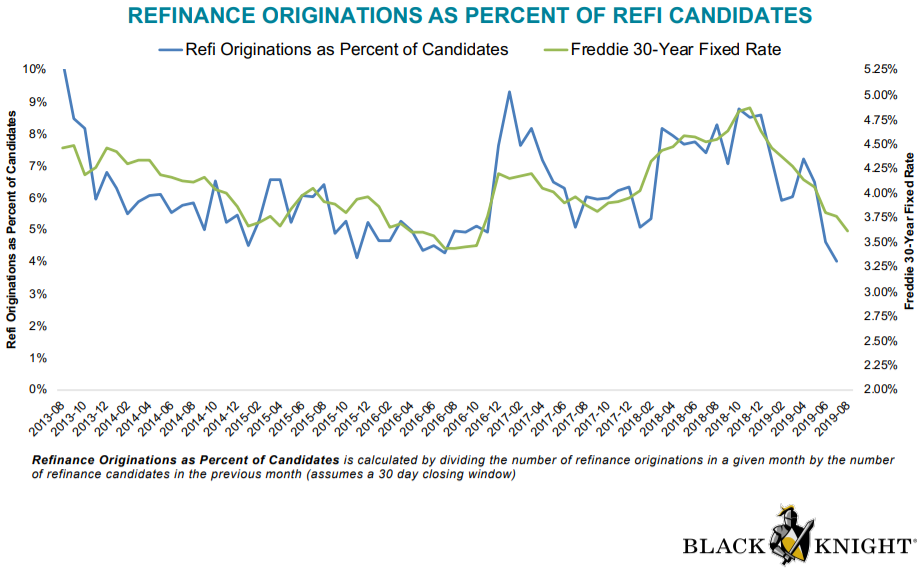

Are those candidates actually refinancing? Black Knight says that when interest rates rise, the ratio of originations to refinance candidates also tend to go up. This is because lower credit quality rate/term refinances and "out of the money" cash out refinances make up a much larger share of the refi market. When rates fall, originations rise, but the ratio of originations to candidates falls. The current ratio has fallen down near 4.0 percent as it did in 2016, the last time interest rates were in the 3.5 percent range. While the company cautions this is only a rough estimate, it does provide some guidance as to future origination volumes. They say that refi lending hit a 21-month high in July and if the 4 percent ratio holds, there might be as much as an additional 20 to 40 percent increase.