Ginnie Mae, is a wholly owned U.S. government corporation that guarantees and securitizes pools of mortgages originated through FHA, Veterans Administration, and Rural Housing Administration programs. Since the housing crisis Gennie Mae has experienced a shift in is lender (issuer) base; the share of non-banks originating the loans underlying its mortgages-backed securities (MBS) has increased significantly. Now the Office of Inspector General (OIG) for the Department of Housing and Urban Development (HUD), has published the results of an audit which claims Ginnie Mae, in its oversight role, has not adequately responded to that shift.

While Ginnie Mae guarantees and securitizes the above types of loans, it depends on its issuers to take full responsibility for servicing, remitting, and reporting activities for the mortgages in every pool. If the borrower fails to make a timely payment on its mortgage, the issuer must use its own funds to ensure that the investors in the MBS receive timely payment. If it cannot do so, Ginnie Mae, in accordance with its guaranty, defaults the issuer, acquires the servicing of the loans, and uses its own funds to manage the portfolio and make any necessary advances to investors. OIG says the corporation's risk for loss is a counterparty one, and occurs almost entirely at the point of issuer default.

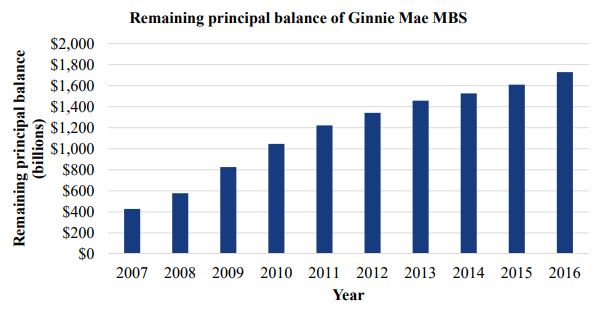

Following the financial crisis, the demand for government-insured loans increased. This created a larger demand for Ginnie Mae's product and the corporation's outstanding principal balanced increased 300 percent, from $427.6 billion in 2007 to $1.7 trillion in 2016.

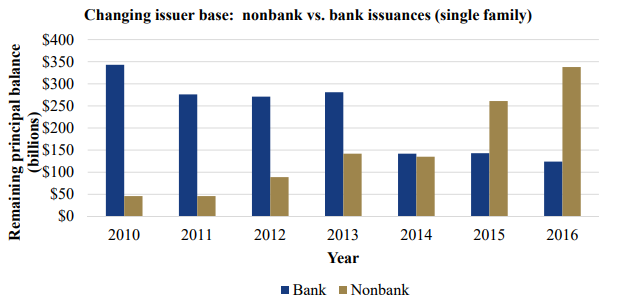

As the housing crisis developed, many banks, defined by OIG as an institution licensed to receive deposits and make loans, retreated from mortgage lending. This tipped the balance of Ginnie Mae's issuer base to non-banks, that is, institutions that offer only mortgage related services. In 2014, Ginnie Mae reported that six of its top 10 issuers were nonbanks and they accounted for more than $392 billion in unpaid principle. Nonbanks overall accounted for 73 percent of Ginnie Mae's single-family issuances. The corporation had not seen such large nonbanks in its previous history nor had them make up such a large portion of its issuer base.

When banks were the dominant issuer, Ginnie Mae outsourced a significant portion of its risk management to their regulators, i.e. the Federal Deposit Insurance Corporation, Federal Reserve, Office of Comptroller of the Currency and the National Credit Union Association. OIG says that while the Consumer Financial Protection Bureau has some authority for non-banks when it comes to consumer issues, those institutions are not subject to the same safety and soundness regulations as, nor is there a regulator equivalent to those overseeing banks. This means Ginnie Mae must provide the first line of defense when it comes to the financial and operational soundness of these entities. This responsibility falls to the its Office of Issuer and Portfolio Management.

Nonbanks tend to have complex financial and operating structures and frequently use sub-servicers instead of servicing the loans in their portfolios. They also rely on credit lines for funding, which may limit their liquidity and ability to meet the financial obligations of being a Ginnie Mae issuer. Banking institutions have standardized corporate ownership and lines of business, substantial liquidity, and the ability to service the loans in their portfolios.

OIG's audit found the Ginnie Mae did not adequately respond to changes in its issuer base. First, it did not consider the impact the growth of nonbanks could have on its organization. These included strategic issues, such as determining the maximum-size issuer default Ginnie Mae could adequately manage, and operational issues, like determining the total impact of a large or multiple-issuer default and determining individual issuers' ability to adapt to changing market conditions, such as rising interest and delinquency rates.

Ginnie Mae did not develop a written default strategy or prepare its executives with guidelines to follow in their management of issuers. In 2011 Ginnie Mae abandoned its desk manual, which included its operating procedures, after determining it no longer reflected current operations. While it hired a contractor in 2014 to review those operations, only this past July did it begin implementing the new policies and procedures that emerged. Several account executives told the auditors they did not have adequate policies and procedures to manage issuers and that they learned how to perform tasks from each other.

Neither did the corporation develop a written default strategy to include identifying, analyzing, and planning for all default scenarios and determining whether its staff and master sub-servicers had the capacity to force default and absorb issuers with more than 100,000 loans. (As of July 2017, Ginnie Mae had 13 nonbank issuers that fell into this category, four of them with more than 400,000 loans.) The company did not begin to implement a written strategy to address large issuers or all default scenarios until this past summer. It now plans to work on the default strategy for home equity conversion mortgages, then on a strategy for multifamily loans.

As a result, the audit says, Ginnie Mae may not identify problems with issuers in time to prevent default." In addition, the audit indicates that Ginnie Mae might not be able to properly service the loans it acquires in a default and may require financial assistance from the U.S. Treasury to pay investors in the event of a large issuer default.

The audit does acknowledge that Ginnie Mae has made progress in addressing the increased counterparty risk posed by nonbanks; creating a new Office of Enterprise Risk, developing a robust watch list, and implementing operational and desktop reviews in which stuff and can request and review more in-depth documentation of issuer operations. It has also created a Spotlight program, which identifies issuers with size, growth, complexity, or nontraditional structures that warrant a more intensive level of ongoing engagement. These changes however, do not address the operational challenges that Ginnie Mae would face if default occurs.

OIG recommends that Ginnie Mae develop and implement:

- Controls to ensure that account executives have policies and procedures that are continually reviewed and updated to reflect changes in operations.

- Controls to determine the impact of large or multi-user defaults, the maximize size Ginnie Mae can handle, and an issuers ability to adapt to changing market conditions.

- Controls to continually assess skills required to meet goals and a plan to accommodate changing organizational needs.

- Training programs to ensure employee skills levels can meet changing organizational need and including secondary market training.

The audit report provoked some blowback from the MBA. Its president and CEO David H. Stevens issued a statement noting that, while the report is correct in stating the importance of Ginnie Mae adapting to the changes in its user base, both the report and subsequent media coverage have mischaracterized the role and risk of nonbank issuers.

Stevens says these nonbanks, or independent mortgage bankers, have been Ginnie Mae issuers for decades and provided critical funding for borrowers when banks scaled back lending in the last recession. They are now subject to stronger state and federal regulations than ever before and better information sharing between regulators at all levels, "facts conspicuously absent from both the OIG report and some media coverage."

Stevens concluded, "Improvements to Ginnie Mae's issuer oversight should focus on the growth in the number and diversity of issuers and the need for adequate resources and tools for this function. To this end, MBA continues to call for Ginnie Mae to have access to sufficient resources to adequately monitor its counterparties-both bank and nonbank. Rather than focusing on different business models and market share numbers, the focus should be on ensuring that Ginnie Mae is given the resources needed to oversee the market in a responsible manner."