In the last half of 2017 the three credit bureaus, Equifax, TransUnion, and Experian, agreed to change the way they handle collection accounts. These accounts represent a wide variety of debt - unpaid gym memberships, unpaid traffic tickets, delinquent rent, even unreturned library books. However unpaid medical bills account for about 52 percent of those debts. Another 23 percent are utility bills, and about 6 percent are debts that have defaulted and been sold to third party collection firms. About 40 percent of consumers with a credit report have had a debt in collections on their record at some point.

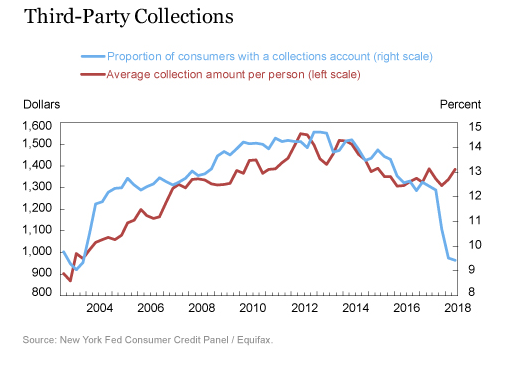

The New York Federal Reserve's Liberty Street Economics group says that collection accounts become more prevalent during the Great Recession, but since there has been a declining trend showing that the percentage of consumers with a collections account on their credit report (Equifax reports were used for this study) declined from over 14 percent in 2013 to 12 percent in 2017. Now that share has dropped to 9 percent and that change mentioned at the top of this article is most likely the cause.

The National Consumer Assistance Plan (NCAP) went into effect in the second half of last year and required a more frequent, detailed, and accurate reporting of collection accounts, including marking them paid when they have been. NCAP prohibits reporting debts that are not associated with a contract or agreement to pay. Also prohibited are reporting of debts without sufficient information to link them to the consumer, that is a name, address, and some other method of identification such as a Social Security number.

Probably the most important change is the one that prohibits reporting a medical debt that is less than 180 days old. Some such debts have been a problem because of the slow-pay practices of some insurance companies. Many consumers have reported they were unaware their claims had not been paid until after their accounts have been turned over to bill collectors.

Four NY Fed staffers, Andrew Haughwout, Donghoon Lee, Joelle Scally, and Wilbert van der Klaauw, write in the Liberty Street blog that during the 12 months ended in June 2018, the time period when NCAP was implemented, the number of persons with a collection account on their credit report fell from 33 million to 25 million while the number of collection accounts dropped from more than 66 million to about 47 million. The aggregate balance declined by $11 billion.

The authors say that, as might be expected, many of these individuals had relatively low credit scores to begin with; 80 percent had scores under 660 before the law kicked into effect. Nine percent had no scores at all, only reports that consisted primarily of collections. They also had higher delinquency rates on other debts than the general population as well.

The authors found the impact of removing collection accounts was relatively small because of the low credit scores and flawed credit histories of most beneficiaries. There was an average increase of 11 points in the Equifax Risk Score. However, as shown in the chart below, there was a wide variation in score changes. Some even saw their score decline, probably due to negative factors unconnected to the policy change.

However, what the authors call "a nontrivial" 18 percent of affected individuals saw their credit scores increase by more than 30 points. Those who saw the largest boost to their scores were generally those with initially very low credit scores. For example, those who saw a 40 or more point increase in their score began with an average of 529 ended with an average of 588.

Of those with "subprime" scores under 620, only 20 percent received enough of an increase to lift them over that mark, and they may also have benefitted from the other changes to credit reporting such as removal of tax liens and judgements.

The article stresses that the changes brought about by NCAP

were "a clean-up, not a purge." The authors conclude, "These borrowers

will certainly benefit in the long run from the cleanup of their credit

reports, since higher scores are associated with better access to credit, to

the job market, and even to the rental housing market. But the immediate impact

of the removal of collections will be muted if the beneficiary's credit record

continues to be tarnished with other negative information."

They also say that in the long-run the numbers of collections accounts may

rebound as creditors adjust to the changes and begin collecting the identifying

information necessary to validate the accounts.