Home equity reports have not been particularly interesting over the last few years. Home prices kept rising, owners kept whittling down their loan-to-value (LTV) ratios and avoiding the serial cash-out refis we have seen in earlier boom times.

With the current crisis, an equity buffer becomes pretty important. The narrow margins that allowed mortgaged homeowners to quickly plunge underwater when home values dropped in the Great Recession cost many their homes. Equity not only allows a homeowner more options - refinancing into a lower cost mortgage, flexibility in selling the house or in negotiating a loan modification - but also gives them an incentive to stay in the home.

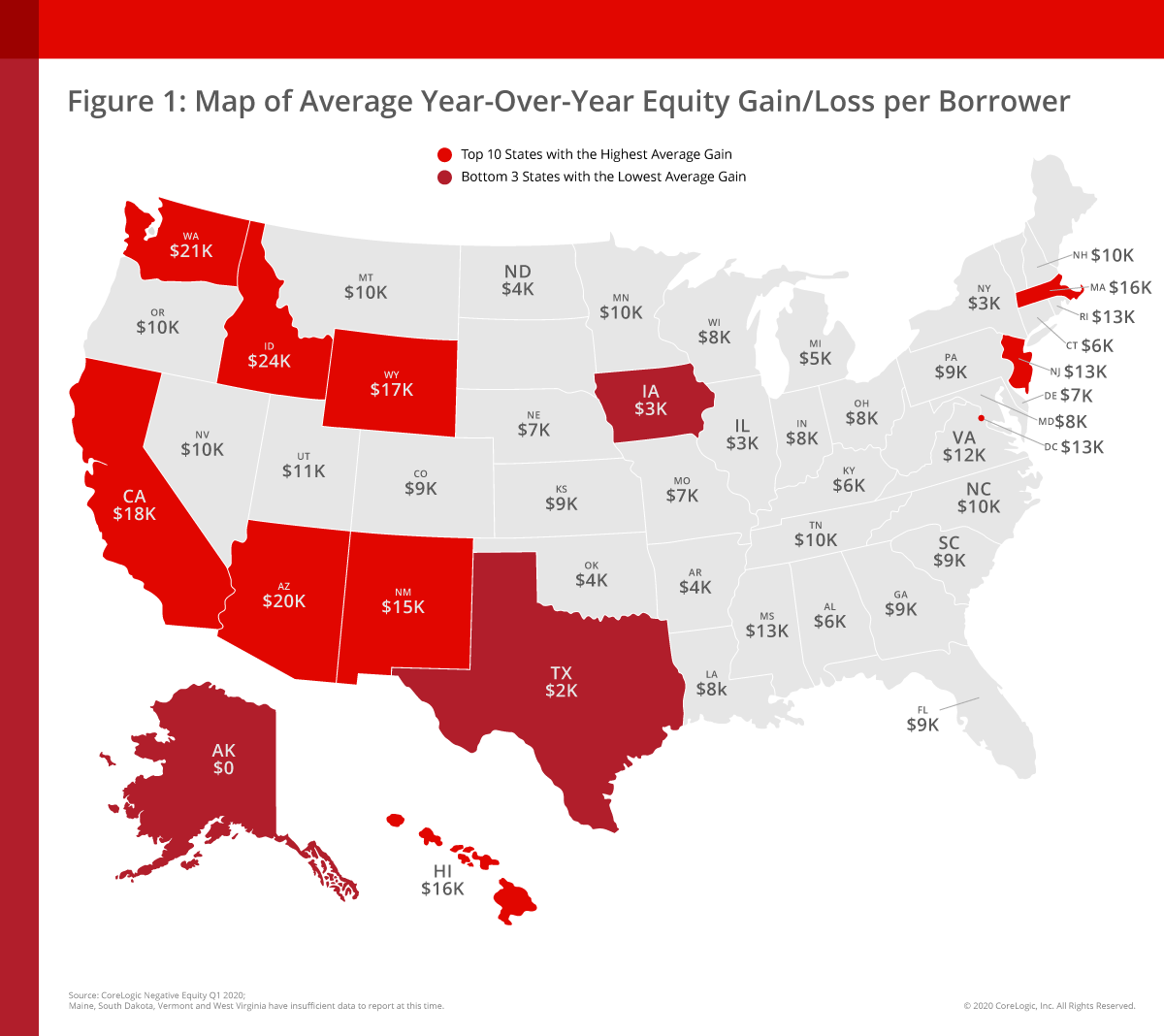

CoreLogic reports that home prices, as yet unaffected by the COVID-19 pandemic, continued to rise in the first quarter of 2020, pushing home equity higher. Nationwide, homeowners with a mortgage, roughly 63 percent of all homeowners, saw their equity increase by 6.5 percent since the first quarter of 2019, a $9,300 per household increase, and an aggregate of $590 billion nationally. States with the largest gains include Idaho, where in the first quarter equity grew by an average of $24,400, Washington, with an average of $20,800 and Arizona at $19,900.

"Many homeowners will experience a recession during their lifetime, and it is reasonable to compare the current recession to those in the past," said Frank Martell, president and CEO of CoreLogic. "But the comparison is not apples to apples - every recession is different. Primary drivers of the Great Recession were an overbuilt housing stock, risky mortgages and the collapse of home prices, creating a massive increase in negative equity that proved difficult to recover from. Today's housing environment has low vacancy and delinquency rates and a large home equity cushion. While the CoreLogic HPI forecasts a decline in home prices in the coming year, we can also expect the majority of homeowners to remain above water."

From the fourth quarter of 2019 to the first quarter of this year the number of homeowners in negative equity, that is owning more on their mortgages than their homes are worth, decreased by 3.1 percent to 1.8 million homes or 3.4 percent of all mortgages properties. This is a 16 percent decrease year-over-year. As the economy climbed out of the recession in the first quarter of 2010, 25.9 percent or 12.1 million homes were still underwater. The total gain since the end of the great recession in 2010 is $6 trillion with the average homeowner accruing about $106,100 in equity since then.

The national aggregate value of negative equity was approximately $284 billion at the end of the first quarter of 2020, down by $1.9 billion from the fourth quarter of 2019 and down year over year by approximately $22.6 billion, or 7.4 percent year-over-year.

Those borrowers with LTVs between 95 and 105 percent are fragile at this point. Any positive or negative price changes are likely to move them into or out of negative territory. CoreLogic estimates that, with a 5 percent price increase, 310,000 homes would gain equity, a 5 percent decline in prices would drive 420,000 underwater

"The pandemic recession will likely lead to price declines in many areas during the next year and weaken home equity gains," said Dr. Frank Nothaft, chief economist for CoreLogic. "However, price declines will be far less than those experienced during the Great Recession, when the national CoreLogic Home Price Index fell 33 percent peak-to-trough. Our latest forecast shows the national index to have a peak-to-trough decline of 1.5 percent."