Black Knight's "first look" at March loan performance data explored the somewhat traditional dip in delinquencies each March due to calendar events like the arrival of tax refunds and the decline of winter utility bills. That was amplified this past March by a rebounding economy and labor market, low interest rates, $378 billion in stimulus payments, and that, for the first time since December, a month that did not end on a Sunday. Only 217,000 mortgages that were current in February became 30 days past due in March, the lowest transition rate on record, and some 671K previously delinquent mortgages cured during the month, making it a "top 5" month of the past decade in that respect as well. Thus, the delinquency rate dropped 16.4 percent to 5.02 percent, the largest monthly decline in 11 years.

The Black Knight's March Mortgage Monitor looks again at this exceptional performance. Black Knight Data & Analytics President Ben Graboske, said, "Not only did March see the largest single-month improvement in delinquencies in 11 years, but all indications suggest more is yet to come. He adds that the improvement in payments has continued into early April, with 91.6 percent of borrowers making their monthly payments by April 23. This could mean another improvement in the delinquency rate when month-end date is reported.

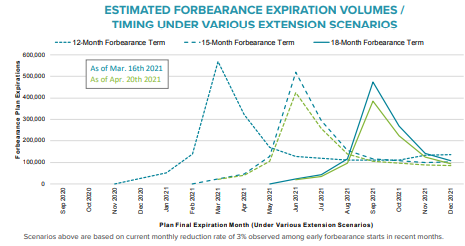

The Monitor also looks at the results thus far of the forbearance programs initiated in response to the pandemic. Two-thirds of the 7.1 million homeowners who were in forbearance plans (14 percent of all those with mortgages) at some point since March of 2020, have now left the program, leaving 2.31 million active participants. Exits picked up in March, as some 1.2 million loans were reviewed for extension or removal with many of them reaching the end of a 12-month term. About 280,000 additional loans were scheduled to expire at the end of April so there may be additional declines in forbearances in late April and early May.

Black Knight notes that, what it is calling "bellwether" forbearances, those homeowners who entered the program early on and will determine the impact of the first 18-month expirations in the fall, have made up a significant share of those leaving the program, a good sign for the overall recovery. As of mid-March, it was projected that about 475,000 plans would still be active at the 18-month expiration point in September with another 275,000 reaching it in October. Progress in April has reduced those numbers to 385,000 and 225,000, respectively. The company says it will be watching closely as about 890,000 homeowners are expected to face a 15-month review at the end of June.

As Graboske says homeowners who have left forbearance have, by and large, been doing well. About 45 percent (3.14 million) of those who left are reperforming and 1.07 million left and paid off their mortgages through a home sale or refinance.

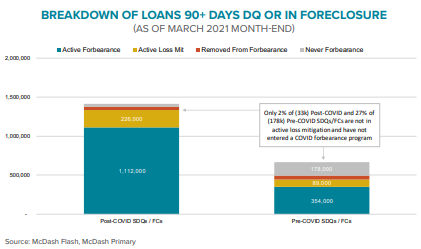

Of most concern are about 160,000 formerly forborne loans which remain delinquent and are not in loss mitigation. The majority of these, more than 100,000, were already delinquent before the pandemic began.

The status of former program participants is overwhelmingly positive across all investor types, but the largest share of those "concerning" loans, delinquent but not in mitigation, are among those serviced for private label securities.

Black Knight says that, as delinquencies have improved, there has been more overlap with the forbearance program as more seriously past due homeowners take advantage of its options. Of 2.1 million borrowers in the 90-day plus bucket, including those that have been in foreclosure, some 90 percent have been in forbearance or are currently in loss mitigation with servicers. Of those who became seriously delinquent after the onset of the pandemic, that share is 98 percent.

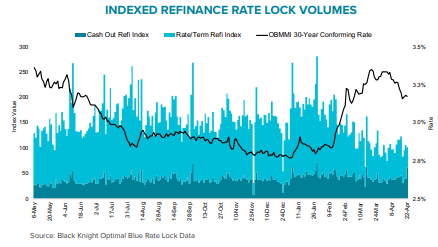

The number of candidates who can both qualify for and benefit from refinancing fell by 40 percent during the first quarter of the year as mortgages rates rose from their record late 2020 lows to over 3.30 percent by mid-March. The Monitor says 7.6 million high qualify refinance candidates lost incentive to refinance based on mortgage rates.

Incentive has bounced back by 30 percent in the past two weeks with 3.4 million homeowners regaining refinancing benefits. Rate/term lock activity accompanied the drop in incentives, declining by 35 percent from December to March and have not yet fully rebounded. However, the company says the rate lock level seen in January shows why prepayment activity was at a 17 year high in March.

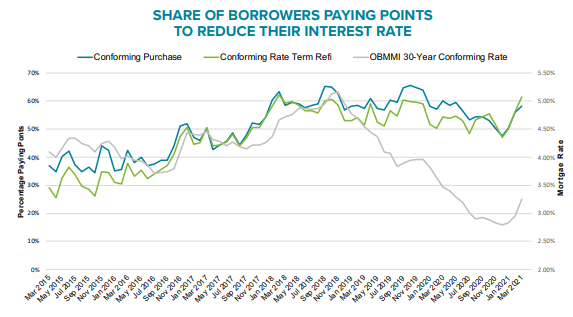

The Monitor says its data shows some interesting trends among rate locks. As rates rose in February and March, so did the share of borrowers who paid points to buy down their interest rates. That share had dropped below 50 percent in December for the first time since 2017 but it has edged up in recent months as borrowers presumably try to counter rising rates. In March about 61 percent of refinancing borrowers and 58 percent of purchase locks involved paying of points. The purchase share, the highest since May 2020, was up from 47 percent in December while the refi share was the highest in 2.5 years. On the chart below, the grey line represents the Optimal Blue Mortgage Market Indices (OBMMI). This is calculated from actual locked rates with consumers across over one-third of all mortgage transactions.

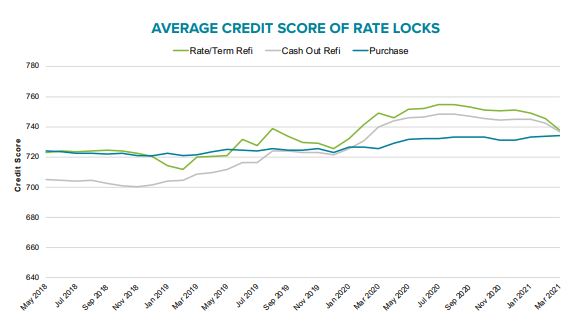

Black Knight also notes that credit scores, which hit all time highs for both purchases and refinances, have begun to decline among refis. They call this typical in a rising rate environment as the most qualified borrowers tend to be the first to refi when rates start to drop and the first to exit the market when they begin to rise.

The average credit score among rate/term refinances is down 13 points and there has been an 8 point decrease among cash-out refinances. Scores among purchase loans has risen 3 points so far this year.