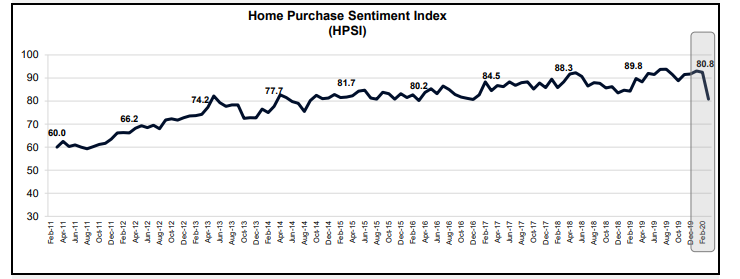

American's attitudes regarding buying and selling homes and about their own financial outlook made an abrupt U-turn last month and Fannie Mae's Home Purchase Sentiment Index (HPSI) wiped out more than three years of gains. The index, a distillation of responses to six questions from the monthly National Housing Survey (NHS) lost 11.7 points, falling to 80.8 in March.

Five of the six index components declined both from February and compared to March 2019, with four falling from the earlier surveys by double digits. This sent the HPSI falling to its lowest reading since December 2016 and down 9.0 points since March 2019.

One of the most resilient components of the index has been the question regarding job security. Respondents who say they are not concerned about losing their job has consistently stayed in the upper 80 percent range for several years. In March it dropped to 77 percent and net positive responses plummeted 18 percentage points to 54 percent.

Consumers also reported that homebuying and home-selling conditions have worsened and took a more pessimistic view of home price growth. The percentage of Americans who say it is a good time to buy decreased from 59 percent to 56 percent while the percentage who say it is a bad time to buy increased 4 points to 36 percent. As a result, the net share of Americans who say it is a good time to buy decreased 7 percentage points and was 2 points lower than last March.

A similar question regarding selling a home fared even worse. Those who said it is a good time to sell decreased from 67 percent to 52 percent while those who disagreed grew from 22 percent to 36 percent. As a result, the net share of those who say it is a good time to sell dropped 29 points, 27 points year-over-year.

The net percentage of those who expect further increases in home prices fell 22 points from February and 22 points year-over-year to a net of 17 percent with 39 percent thinking prices would rise and 22 percent expecting them to fall. The balance thought there would be no change.

The percentage of Americans who say their household income is significantly higher than it was 12 months ago decreased from 32 percent to 27 percent and that 5-point decline was reflected in the net which fell to 16 percent.

The only component which increased

during the month was the one reflecting expectations about the direction of interest

rates. The percentage of Americans who say mortgage rates will go down in the

next 12 months grew 12 points to 20 percent and those who expected them to stay

the same declined from 46 percent to 33 percent. Thirty-nine percent expect

higher rates, only 1 point more than in February. As a result, the net share of

Americans who say mortgage rates will go down over the next 12 months increased

11 percentage points, still a net negative of 19 percent.

"In March, the HPSI dropped to its lowest level since December 2016, with

Americans reporting greater concern about their job security than at any point

in the last six years," said Doug Duncan, Senior Vice President and Chief

Economist.

"Attitudes about the current home-selling environment deteriorated markedly, falling to their lowest level since January 2017. A survey record one-month drop in optimism about the direction of the economy appears to have weakened consumers' views of both the current home-selling and homebuying environment, though the latter is likely buffered in part by low mortgage rates. When asked why it's a bad time to buy or sell a home, approximately 7 percent of consumers offered COVID-19 as an unprompted response, one of the highest percentages of non-standard answers in the survey's history. We expect these developments to weigh heavily on housing activity during the spring/summer homebuying season."

The NHS, from which the HPSI is constructed, is conducted monthly by telephone among 1,000 consumers, both homeowners and renters. In addition to the six questions that are the framework of the index, respondents are asked questions about the economy, personal finances, attitudes about getting a mortgage, and questions to track attitudinal shifts. The March survey was conducted between March 1, 2020 and March 22, 2020. Most of the data collection occurred during the first two weeks of this period.