CoreLogic's December 2020 Loan Performance Insights report was upbeat, citing positive signs of recovery after a rocky year in which a pandemic and related job losses sent delinquency rates skyrocketing. Last year started with the lowest share of loans 30 or more days past due since the company began collecting the data in 1999. Then, as COVID-19 spread along with shelter-in-place directives, the rate doubled, going from 3.6 percent of all mortgages in March to 7.3 percent. As time passed, those early stage delinquencies transitioned into the serious category of 90 or more days past due, quadrupling the size of that bucket by August to 4.3 percent.

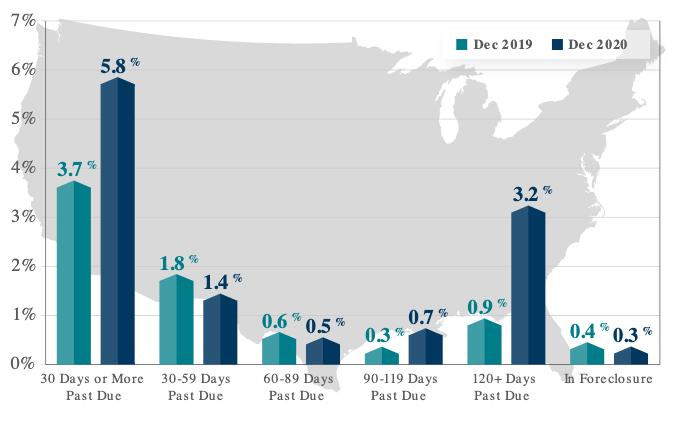

In December, loans that were non-current including those in foreclosure was 5.8 percent. This is still 2.1 percentage points higher than in December 2019, but the national rate has been falling since June. The number of loans in the earliest stage of delinquency, 30 to 59 days, was lower than a year earlier, 1.4 percent compared to 1.8 percent. The next stage, 60 to 89 days past due, AKA adverse delinquency, was down by 0.1 point year-over-year to 0.5 percent.

Serious delinquencies are still elevated at 3.9 percent and that percentage was unchanged from November. A year earlier the rate stood at 1.2 percent. The share of mortgages in some stage of foreclosure is 0.3 percent.

The share of mortgages that transitioned from current to early stage delinquency in December was 0.8 percent. This is the same transition rate as in December 2019.

"Places with large job losses during the last year also experienced big jumps in mortgage delinquencies," said Frank Nothaft, chief economist at CoreLogic. "By state, Hawaii and Nevada had the largest 12-month spike in delinquency rates, both up 4.1 percentage points. They also had large increases in unemployment rates, up 6.6 percentage points in Hawaii and 5.5 percentage points in Nevada compared with 3.1 percentage points for the U.S. In Odessa, Texas, unemployment rose by 8.6 percentage points and delinquencies posted a 9.8 percentage-point jump."