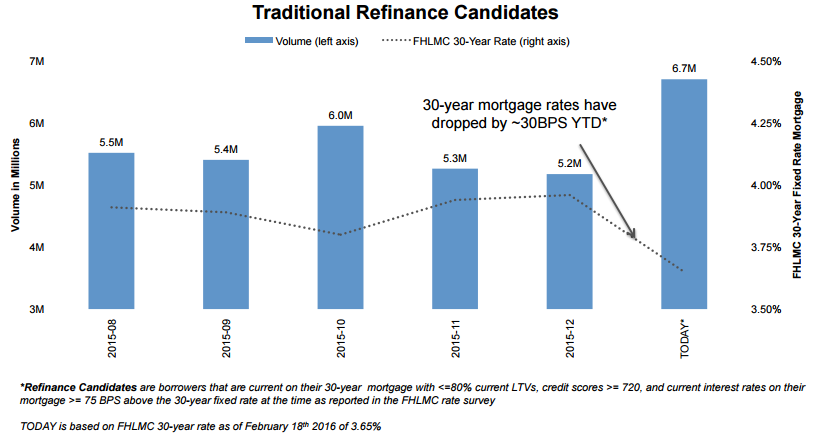

The sharp drop in interest rates that began 2016 has had a very real impact on the so-called "refinanceable" population of homeowners. Black Knight Financial Services says that the 30 basis point decline the market experienced in the first six weeks of the year increased the numbers of those who potentially could qualify and benefit from refinancing by 30 percent, to 6.7 million potential borrowers. If they decided to act they could save $20 billion per year, an average of $3,000 per homeowner. Black Knight bases its estimate on the number of existing mortgages with rates in the 4.5 percent range.

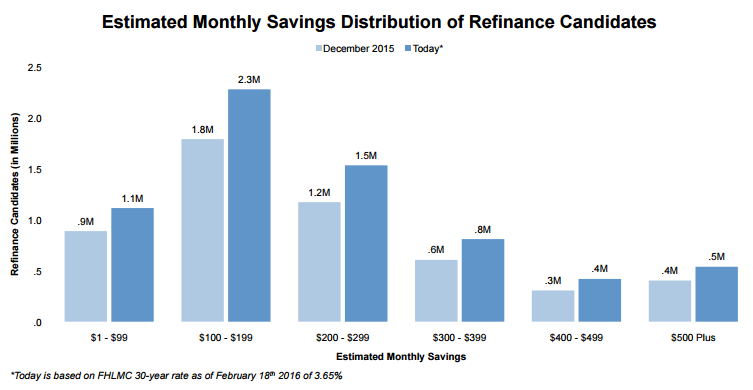

In its current edition of its Mortgage Monitor Black Knight's says that 3.3 million borrowers could save $200 per month by refinancing. Of these nearly one million of those could save $400 or more each month. At the time the analysis was performed the rate was at about 3.65 percent and compared to the end of 2015 the number of borrowers who could save over $200 per month had increased by 800,000.

The Monitor published an analysis of the refinance market about two months ago, shortly after the Federal Reserve raised the target rate of fed funds by 25 basis points. At that time, the population that could benefit from refinancing was estimated at 5.2 million homeowners and the conventional wisdom was that long term rates would rise in response so that refinance eligible number would be in decline.

As Black Knight Data & Analytics Senior Vice President Ben Graboske explained, "Global economic shocks then sent investors looking for the safety of U.S. Treasuries, driving down yields on benchmark 10-year bonds. Mortgage interest rates began to fall in defiance of prevailing wisdom, and the refinanceable population grew by 30 percent in the first six weeks of 2016. As a result, an additional 1.5 million mortgage holders could now likely both qualify for and benefit from refinancing, bringing the total number of potential refinance candidates to 6.7 million. Given that refinance originations fell by 27 percent from Q1 to Q4 2015, and prepayment rates - historically a good indicator of refinance activity - hit their lowest level in two years in January - this expansion of potential candidates could very well provide a welcome and unexpected lift to the market as we move forward in 2016."

The rate decline has also given a boost to the Home Affordable Refinance Program which is due to expire at the end of 2016. Black Knight estimates that the rate decline in the first six weeks of the year boosted the number of candidates for those loans by 40,000.

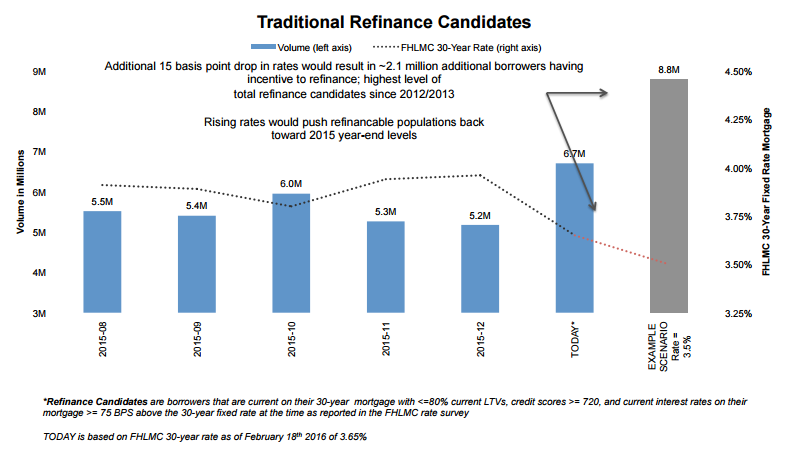

Black Knight also analyzed a scenario under which mortgage rates might ease back by another 15 basis points, taking the 30-year fixed rate down to 3.5 percent. It estimates that would provide entry for another 2.1 million borrowers into the refinanceable population. At 8.8 million, that would make for the largest refinanceable population since 2012-2013, when rates were at historic lows."

The Monitor cautions that the refinanceable population is an extremely rate sensitive one and if rates begin to rise its numbers will quickly dissipate.

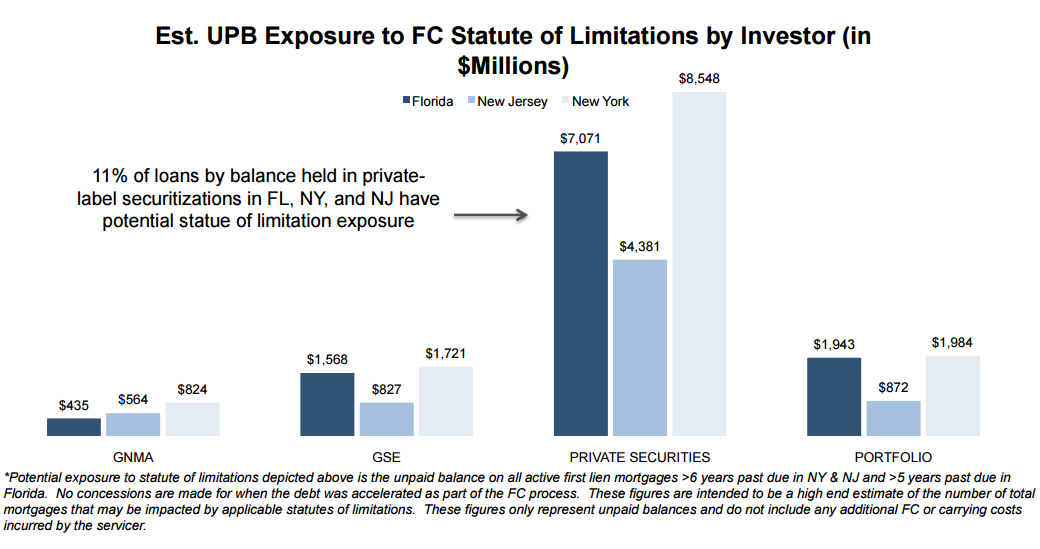

Under the heading of snoozing and loosing, Black Knight says that lenders in three states could find themselves unable to complete foreclosure proceedings. In Florida, New Jersey, and New York the courts are deliberating how statutes of limitations laws might be applied to foreclosure actions. A ruling that they do apply could affect up to 98,000 seriously delinquent loans that are more than five years past due in Florida and more than six years in the other two states.

Florida, despite reducing its foreclosure inventory by 38 percent over the past 12 months still has roughly 40,000 loans with statute of limitations exposure. Potential exposure levels in New York and New Jersey have risen over the past 12 months - currently sitting at 35,300 and 22,000 respectively - due to limited resolution in severely delinquent loan populations in both states.

Without taking into account additional carrying costs and/or fees incurred by mortgage servicers, Black Knight estimates the current potential unpaid principal balance (UPB) risk exposure in these three states at approximately $30 billion, concentrated primarily in private-label securities. As it stands today, roughly $1 out of every $10 of principal in private-label securitizations in these three states is tied to a mortgage that is delinquent by more than allowed by the relevant statutes of limitations.

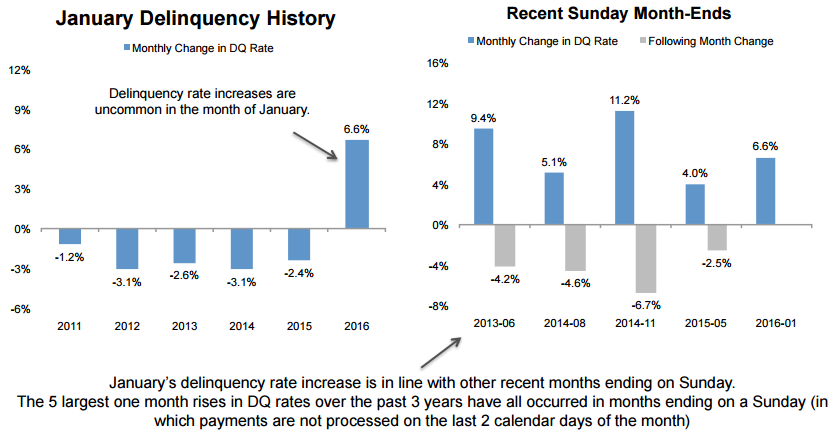

While Black Knight had released loan performance data for January in its "first look" report late last month, the Monitor contains a more in-depth analysis of one striking figure from that report. Mortgage delinquency rates shot up by 6.6 percent from December bringing the national delinquency rate above 5 percent for the first time in 11 months. It was the first increase in any January since the housing crisis began.

On average delinquency rates over the last four years have declined by 2 percent or more in January but Black Knight says the January 2016 spike appears to be calendar rather than loan performance driven. When a month ends in a Sunday there is typically an increase in delinquencies as servicers are unable to process payments that arrive in the last two days of the month. The five largest month-over-month delinquency increases seen over the last three years have all come a Sunday-ending month. These figures usually partially reverse themselves the following month although a residual typically remains.