A new policy paper from the Urban Institute (UI) looks at the recent amendments to the senior preferred stock purchase agreement (PSPA) agreed to by outgoing Treasury Secretary Steven Mnuchin and Mark Calabria, Director the Federal Housing Finance Agency (FHFA) on January 14, 2021. The PSPA governs Treasury's financial relationship with the GSEs Fannie Mae and Freddie Mac. The changes were intended to enable the eventual release of the GSEs from conservatorship by allowing them to build capital and provides milestones for their release.

The changes also serve to constrain the GSEs' activities well after their release by putting limits on their business practices including limits on the amount of "high risk" mortgages they can purchase as well as those that finance second homes or investor properties. It also caps the use of the cash window.

The authors of the report, Laurie Goodman, John Walsh, and Jung Hyun Choi of UI and Edward Golding of the Massachusetts Institute of Technology, conclude that the changes made by the amendments should be revised or abandoned.

The PSPA now limits the GSEs' purchases of high-risk single-family loans to 6 percent of their purchase money and 3 percent of their refinance mortgages. A high risk loan has at least two of the following characteristics: a loan-to-value (LTV) ratio higher than 90 percent, a borrower debt-to-income (DTI) ratio above 45 percent, and a borrower credit score below 680. No more than 7 percent of purchases can be mortgages on second home or investor properties. All limits are measured as 52-week moving averages.

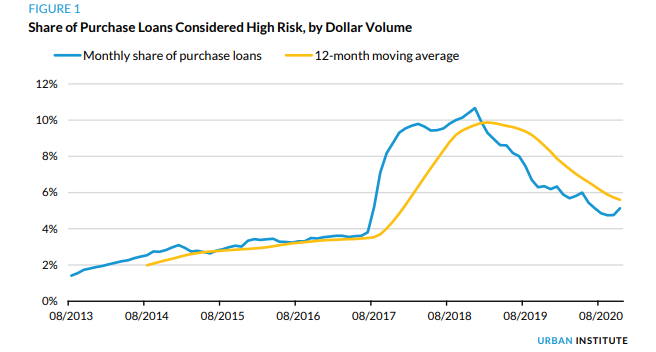

Figure 1 shows the dollar volume share of purchase loans originated since 2013 that are high risk, on both a month-by-month basis and as a 12-month moving average (52-week numbers are not publicly available.) According to the monthly results, 5.13 percent of purchase loans were high risk in November 2020, which is below the 6 percent threshold. The 6 percent limit has been irrelevant since the beginning of the pandemic which has diminished the presence of high-risk loans but would have curtailed purchases from late 2017 through January 2020. As vaccines become more available, the economy improves, and interest rates rise enough to slow refinancing, the numerous pandemic disincentives will fade, and the 6 percent limitation will again be binding.

The situation with high-risk refinancing is somewhat similar. Only 0.48 percent of refinance loans are high risk now, but it was above 3 percent per month between October 2017 and January 2019 and for the 12-month moving average between June 2018 and September 2019. The median FICO score on refinance loans now stands at 770, reflecting a refinance wave in which capacity constrained originators processed their lowest-risk refinances first.

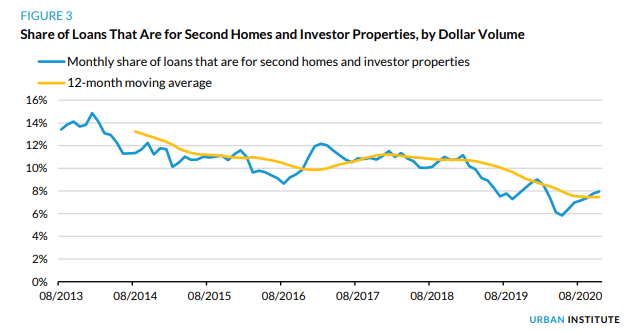

The current share of loans for second homes and investor properties is above 7 percent, so the new threshold is already constraining and would have been as a moving average continuously since 2013. Moreover, the loan-level pricing adjustments on investor loans make them a lucrative part of the GSE portfolio, more than compensating for their risk. They also allow for cross-subsidizing the rest of the GSE purchases. The rental units in one-to-four-unit structures account for half of all rental units, many of which are rented by low- and moderate-income households. Placing limitations on these markets are likely to indirectly affect Biden administration's policy objectives by reducing the resources by which the GSEs can cut the cost of borrowing for underserved borrowers.

The caps on high-risk purchases and refinances, while not binding now, will be when the environment is not driven by refinances. And the already binding caps on second homes and investor properties will result in fewer of these loans, limiting some of the more profitable books of business and hence the resources to subsidize underserved market segments.

The authors say that even were there policy justifications to the limits on these market segments, they make little sense. They are inefficient, difficult to manage, and redundant means of controlling risk. Generally, it is preferable to directly price for risk rather than using hard limits which give no credit for compensating factors, such as a very high credit score offsetting high LTV and DTI ratios.

The limits are also going to be prohibitively difficult to manage as a 52-week moving averages. If a GSE has room within the limit and attractive opportunities to exceed it for a short time, the resulting production will factor into decisions the entire subsequent year, requiring production below the ceiling for a short time, regardless of the circumstances. Thus, the GSEs will need to manage with a cushion, the size of which will depend on the metric's volatility. Using data from August 2013 through November 2020 the authors determined a high standard deviation for both high risk purchase and refinance mortgage between moving averages which suggests that cushions could be sizeable.

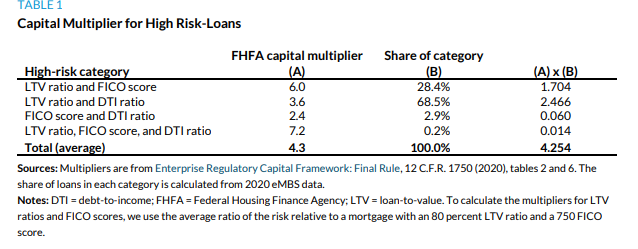

Further, the authors contend the ceilings are redundant if their objective is to guard against risk. The FHFA has already implicitly priced for the PSPA restricted mortgage products in its final risk-based capital rule. The rule is complicated and has many moving pieces but is a straightforward way to approximate the extra capital charge for high-risk products. Using that rule and its capital multiplier with the share of 2020 loans in each high-risk bucket, they estimate that those loans will require 4.25 times the capital of low-risk loans.

While the authors say they have been critical about the limitations of the capital rule, its multipliers do capture the relative risk of loan characteristics. The multiplier of 4.25 for high-risk products is enough to protect against the incremental risk. It also amplifies an already overly stringent average capital level of around 3 percent, resulting in a 12.75 percent capital requirement for these loans. This should guard against excessive risk building up in the GSEs.

Thus, FHFA is already accomplishing the same goal through its capital rule as the PSPA attempts with its cruder ceiling. The automated underwriting systems measure these characteristics as well. Less than 0.2 percent of the high-risk loans in 2020 violated all three of the triggers.

The PSPA's 7 percent limits on investor properties and second homes do not seem based on concern for risk, as the capital rule establishes the capital multipliers for these products at 1.2 and 1.0, respectively. The pricing adjustments more than cover any added risk, and investor loans are the GSEs' cash cows.

In addition to being an inefficient risk control, these limits will have a disproportionate impact on borrowers of color. Table 2 presents the median FICO scores, combined LTV (CLTV) ratios for purchase and refinance mortgages, and DTI ratios by race and ethnicity in 2019. Black and Hispanic borrowers have lower FICO scores and higher CLTV ratios and DTI ratios than either non-Hispanic white or Asian borrowers.

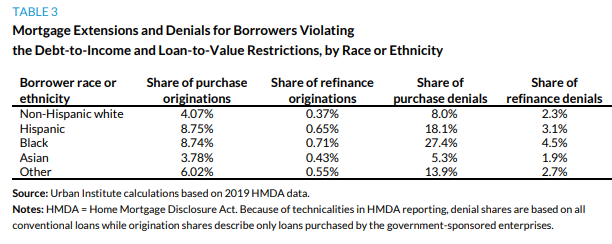

While Table 2 shows substantial differences in FICO scores by race and ethnicity, Home Mortgage Disclosure Act (HMDA) data do not include that information, so Table 3 includes only CLTV and DTI ratios. For GSE purchase mortgages made in 2019, more than twice the share of Black and Hispanic borrowers than white borrowers would be considered high risk, as determined by FICO scores and LTV ratios only, making it more difficult to expand the credit box to those borrowers.

Among the conventional loan purchase denials, 27.4 percent of Black and 18.1 percent Hispanic borrower were considered high risk, as measured by LTV and DTI ratios only compared with 8.0 percent of white and 5.3 percent of Asian borrowers. The refinance denials also show a higher share of Black and Hispanic borrowers in this high-risk category, as defined by the PSPAs, although the absolute numbers are much lower.

The PSPA restriction on high-risk loans would thus drag down the already low share of Black and Hispanic borrowers who use GSE mortgages. In 2019, mortgages to Black and Hispanic borrowers represented 5.8 and 10 percent of all mortgages extended, but only 3.5 percent and 8.9 percent of GSE mortgages, respectively.

Some borrowers who will fall out of the GSE channel because of this constraint will get loans from FHA, so the constraint would not reduce the total risk to the taxpayer, merely shift it to a different government guarantor, one with less flexibility in loss mitigation than the GSEs.

The analysis also found that the amendments could prohibit revival of one of the more successful housing crisis relief programs. The Home Affordable Refinance Program (HARP). allowed streamlined no-doc refinancing for 3.4 million borrowers with existing GSE mortgages. It cut the probability of default for these borrowers 40 to 60 percent, but few HARP loans would qualify for refinancing today.

The possibility of reprising HARP makes sense in the current pandemic environment as it could lower default rates and the use of forbearance, while providing a further stimulus channel without cost to the taxpayer. However, the GSEs would be unable to control the number of high-risk loans so the amendment would make such a program, one which would benefit the high-risk borrowers the most, difficult, taking a powerful policy tool off the table.

The PSPA amendment's limitations on the use of the cash window could undermine the new Single Security. After January 1, 2022, the GSEs will be unable to acquire more than $1.5 billion in loans from any single seller over any four-year period. Assuming an average loan size of close to $300,000, this is about 5,000 loans per originator or 10,000 across the two GSEs. While HMDA data do not capture all GSE originations, UI estimates that approximately 107 originators in 2020 (58 in 2019) had volumes in excess of 10,000 loans per year and could be affected by this limit. If this was prompted by a desire to ensure equal pricing for large and small lenders, these price disparities had already been addressed in previous FHFA guidance.

This move comes at a clear cost. The success of the Single Security, which can contain Fannie Mae or Freddie Mac loans, requires that the prepayment speeds be close for every coupon-issue year cohort. The cash window allows the GSEs to put any given loan into any of multiple pools to maintain prepayment consistency across them. Taking away this pooling flexibility will, over time, make the management of the single security more difficult, creating some risk that investors may start to reject it, compromising the liquidity of the agency mortgage-backed security market.

At the very least, the FHFA could have calibrated its cutoff to target just the top 5 or 10 or even 20 originators, rather than potentially hitting more than 100. A more appropriate target might be 50,000 loans per GSE, rather than one-tenth that amount. This higher target would have affected 6 originators in 2019 and 19 in 2020. As the appropriate limit can change with market conditions, imposing limits through rulemaking would give FHFA the flexibility to easily change it.

The UI paper concludes that the limits imposed in the PSPAs are neither efficient nor effective in managing risk and come at considerable cost, undermining policymakers' ability to support the mortgage market on several fronts. They both disproportionately affect borrowers of color and unnecessarily constrict policy choices going forward. The authors urge the Biden administration to revise the limits to better meet their policy objectives or abandon them for the sake of more dynamic, flexible tools in rulemaking or directives.