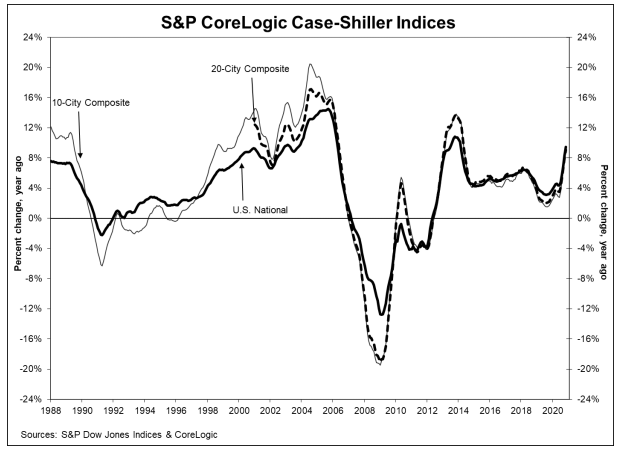

The annual increases in U.S. home prices is nearing dizzying levels. The November data from the Federal Housing Finance Agency (FHFA) crossed into double digits for the second consecutive month while the months numbers from S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index came close.

The Case-Shiller index, which covers all nine U.S. census divisions, gained 9.5 percent compared to the previous November. The annual increase in October was 8.4 percent. On a seasonally adjusted monthly basis the National Index rose 1.4 percent and was 1.1 percent higher on an unadjusted basis.

Appreciation in Case-Shiller's two composite indices also accelerated - each rose more than a single percentage point from the annual gains in October. The 10-City composite's increase came in at 8.8 percent compared to 7.6 percent in October. The 20-City Composite rose 9.1 percent, up from 8.0 percent. Data from Wayne County Michigan continues to be insufficient due to earlier COVID related shutdowns to include Detroit's housing transactions in the indices.

The 10-City Composite posted a 1.2 percent monthly gain and the 20-City rose 1.1 percent before adjustment. Both were up 1.4 percent afterward. All 19 cities reported monthly gains for both their adjusted and unadjusted indices.

The fastest appreciating cities covered by Case-Shiller continue to be Phoenix, Seattle, and San Diego. Home prices in Phoenix were up year-over-year by 13.8 percent in the 18th straight month it has led the field. Seattle's prices rose 12.7 percent and San Diego's gain was 12.3 percent. All 19 cities reported higher price increases in the year ending November 2020 versus the year ending October 2020. Prices growth was strongest in the West (10.1 percent) and Southwest (9.7 percent) regions, with the historically lagging Northeast (9.3 percent) also turning in an impressive month."

CoreLogic Deputy Chief Economist Selma Hepp said of the numbers, "Housing continued to exceed expectations, even during the early winter months when demand tends to cool down. With existing home sales up over 20 percent from a year ago, S&P CoreLogic Case-Shiller Index clocked a 9.49 percent surge in November - a new high since February 2014. According to CoreLogic Buyer/Seller Market Indicator, which measures the ratio between sold price and list price, buyer competition reached a new peak nationally in October and November when the ratio climbed to 0.996 - the highest level since 2008, when the data series began. The high Buyer/Seller Market Indicator suggests home sellers were generally getting their asking price. With buyer demand continuing to outpace the previous year's levels amid historically lowest inventory of for-sale homes, the pressure on home prices is going to fuel home price growth in the first half of 2021."

"The trend of accelerating home prices that began in June 2020 has now reached its sixth month with November's emphatic report," says Craig J. Lazzara, Managing Director and Global Head of Index Investment Strategy at S&P Dow Jones Indices. "The National Composite Index gained 9.5 percent relative to its level a year ago, accelerating from October's 8.4 percent increase. The 10- and 20-City Composites... also rose more rapidly in November than they had done in October. The housing market's strength was once again broadly-based: all 19 cities for which we have November data rose, and all 19 gained more in the 12 months ended in November than they had gained in the 12 months ended in October."

Lazzara said, while the effects of the pandemic on housing prices was unclear last spring, after a brief deceleration in May and June they began to climb again. "November's report continues that acceleration in a particularly impressive manner. The National Composite last matched this month's 9.5 percent growth rate in February 2014, more than six and a half years ago. From the perspective of more than 30 years of S&P CoreLogic Case-Shiller data, November's 9.5 percent year-over-year change ranks near the top decile of all monthly reports.

"Recent data are consistent with the view that COVID has encouraged potential buyers to move from urban apartments to suburban homes. This may represent a true secular shift in housing demand or may simply represent an acceleration of moves that would have taken place over the next several years anyway. Future data will be required to address that question."

Home prices have now exceeded the previous price peaks, established in the summer of 2006, by 25.9 percent nationally and by 15.5 percent for cities in the 20-City Composite and 11.2 percent for those in the 10-City index.

The S&P CoreLogic Case-Shiller Home Price Indices are constructed to accurately track the price path of typical single-family home pairs for thousands of individual houses from the available universe of arms-length sales data. The National U.S. Home Price Index tracks the value of single-family housing within the United States. The indices have a base value of 100 in January 2000; thus, for example, a current index value of 150 translates to a 50 percent appreciation rate since January 2000 for a typical home located within the subject market.

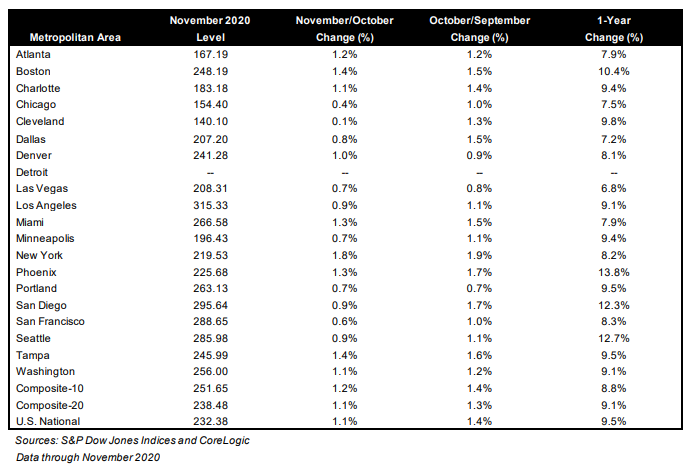

As of November 2020, the National Index was at 232.38 compared to 229.93 in October. The 10- and 20-City Composites had readings of 251.65 and 238.48 up from to 248.58 and 236.77 the prior month. Los Angeles has the highest index reading at 315.33 and Cleveland (absent data on Detroit) the lowest at 140.10.

FHFA reported that the annual increase in its Housing Market Index (HPI) was 11.0 in November compared to 10.2 percent in October. The monthly increase was 1.0 percent, down from the 1.5 percent gain from September to October .

All nine census divisions posted both annual and month-over-month price gains. The seasonally adjusted monthly changes ranged from 0.3 percent in the West South Central division to 1.6 percent in the Pacific division. The 12-month changes varied from 8.7 percent in the West South Central division to 14.0 percent in the Mountain division.

"House prices have risen by at least one percent for six consecutive months," said Dr. Lynn Fisher, FHFA's Deputy Director of the Division of Research and Statistics. "The acceleration has been slowing but annual gains now outpace the prior housing boom. Current conditions can be explained by fundamentals, including low rates and tight housing supply, which have been intensified by the pandemic."

FHFA's HPI is based on the sales prices of homes financed by the GSEs Fannie Mae and Freddie Mac. The index was benchmarked at 100 in January 1991 and was at 310.1 in November compared to 307.0 in October.