While COVID-19 has wreaked havoc on most of the economy last year, Wells Fargo's Securities Economic Group says many of the responses to the pandemic - lockdowns, remote schooling, and remote work - served to "flip the script" on housing, increasing demand for some types of properties and locations. At the same time, massive job losses have caused a spike in the delinquent mortgage and rent payments, although forbearance and moratoriums have held foreclosures and evictions to a minimum. A new report from the economists puts forward and answers five questions about the direction of housing over the next year.

What is the risk that the red-hot housing market will turn into a bubble?

Concerns about a bubble stem mainly from surging home prices; the median price of an existing single-family home is up 15.1 percent over the past year. This, however, has come from some unusual supply and demand dynamics rather than increased speculation. Remote working and learning and other increases in at-home time has spurred demand for more living space. Apartment renters are looking to buy; homeowners are seeking larger homes.

These changes have resulted in an outward shift in housing demand that by itself drives home prices higher at a time when the housing supply has also been disrupted. More people want to buy homes, fewer want to sell them, shifting the supply curve inward, pushing the inventory of available homes to an all-time low. The report says, "Folks that were thinking about downsizing are now holding onto their current homes because they need them for workspace or to house their adult children returning from school or urban apartments." Rather than selling, many are investing in upgrades, increasing demand for remodelers, and driving up sales at home improvement centers.

There are other constraints on the housing supply. Mortgage forbearances through the CARES Act allowed homeowners options for repayment at the end of forbearance, resulting in fewer foreclosures. Since distressed sales are typically discounted, the lack of foreclosures tends to exaggerate the year-over-year rise in home prices. "The shift in preferences to larger homes and lack of foreclosures is one reason that average and median home prices have increased much more than prices in repeat-sales indices, such as the S&P CoreLogic Case-Shiller and FHFA Home Price Index," the report says.

Lender discipline is possibly the greatest difference from the bubble years. Mortgage underwriting tightened at the onset of the pandemic and remains relatively tight today, with higher FICO scores and fewer cash-out refinancings. Homeowner equity per the Federal Reserve is $20.4 trillion, nearly two-thirds of single-family housing values, and low interest rates have allowed many homeowners to refinance into lower payments while enhancing their creditworthiness.

What happens when forbearance ends?

The economists expect increasing foreclosures when moratoriums end, but not a serious surge. They say forbearance has proven remarkably successful with the number of forborne loans edging lower since peaking in the spring. Many of those exiting forbearance are either making payments or modifying their mortgages. Data from Black Knight shows the number of properties that are delinquent but not in foreclosure has risen 81 percent to 3,381,000; 2.2 million are 90 or more days past due. These numbers, while problematic, include mortgages still in forbearance, many of which will see terms extended, with little negative impact. To the extent that foreclosures increase they are not expected to weigh too heavily over the market. Distressed loans are not nearly as concentrated as they were during the bubble years and the housing market is undersupplied. The economists say there may be issues in states like Mississippi and Louisiana that are slow growing and those that are dependent on tourism like Nevada and Hawaii.

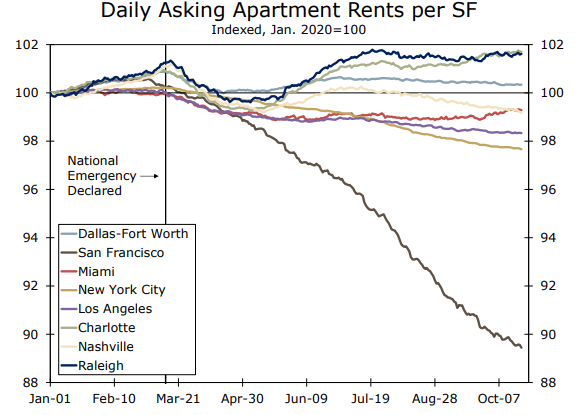

Has the pandemic ended the "urban renaissance" and will this hurt the apartment market?

Many urban areas bloomed after the housing crisis as tech companies moved in from the suburban locations they had previously preferred. The trend spread from the West across the nation and urban areas outgrew the suburbs during the first five years of the last decade, fueling not only demand for apartments but for dining and entertainment. Sports facilities returned to cities, attracting apartments, offices, and entertainment venues. Industrial properties were repurposed and revitalized, property values shot up and apartment construction shifted to luxury units. As many existing residents were priced out, a backlash against gentrification took hold, again in the West, but quickly spread. In the second half of the decade growth in the suburbs outpaced central cities again.

Affordability has long been a problem for the apartment market. Per the Harvard Joint Center for Housing Studies, about a quarter of apartment renters have been severely rent burdened over the past decade and another 10 percent moderately so.

The growth in renter households over the last ten years has been driven by higher income earners, particularly in cities. But when the pandemic lockdowns hit, and the workforce relocated to their kitchens, those attractive urban amenities, the bars and sports arenas were shuttered and renters fled high-cost areas, moving in with families or finding lower cost housing, frequently in the suburbs. Demand cooled substantially in most major urban apartment markets.

The Wells economists expect this move to lower-price markets to carry into the early years of economic recovery. They also see those industries forced by the nature of their activities to remain office based, to become less concentrated in areas like Manhattan and the Silicon Valley. Several markets, such as Austin, Atlanta, and Raleigh have already developed startup communities. This, along with the increased ability to work remotely, will help the transfer out of high-cost cities to persist at least in the medium term. The demand for apartments will also shift toward those sizable mid-sized metro areas and toward their surrounding suburbs and exurbs.

Will the surge in delinquent rents weigh on the economic recovery?

As unemployment spiked in the spring so did concerns people paying their rents. Many state and local governments quickly enacted eviction moratoriums which moved concerns to whether landlords would be able to meet their own financial commitments.

The Census Bureau reports approximately 7.24 million renters, 16.2 percent of the 44.7 million renter households, were behind on rents in early September. A large proportion of those behind in their rent reported via the weekly Household Pulse they were not at all confident they will be able to make their October rent, while 14.9 percent (1.08 million) and 30.5 percent (2.21 million) said eviction was either "very likely" or "somewhat likely" in the next two months. Wells Fargo points out, however, that just over 60 percent of those who are behind in their rent live in single-family homes, duplexes, triplexes and quadplexes which, in turn, account for about 55 percent of the rental housing stock. These are primarily owned by individual "mom-and-pop" investors. A much smaller share are behind in rent in professionally managed, multifamily properties. Comparable Census data reports 90.1 percent of households in those units made full or partial payments by September 20 although there has been some recent slippage.

The distinction between "mom-and-pops" and professionally managed properties is important. A disproportionate share of lower-income households rent from "mom-and-pops" and account for the bulk of rental delinquencies. This is hardly surprising, as workers employed in high-contact industries, including restaurants, bars, hair salons and fitness studios, have endured a disproportionate share of job and income losses.

Conversely, much of the demand for professionally managed apartments comes from higher-income households, which are better able to work remotely. Despite a lower negative impact, the attraction of the high-priced rental apartment is not what it was pre-pandemic. The economists see vacancies rising slightly, especially in markets with a lot of new apartments coming on line. It will be hard to raise rents until there are better employment numbers. Large, rapidly growing, dense, urban areas could suffer as recent data shows renters are pivoting toward suburban and less dense metro areas.

Workers in high-contact occupations have been heavily damaged and, while relief programs such as the CARES Act provided significant help early in the pandemic, much of the assistance has expired. Renters have had to borrow from relatives or incur credit card debt to try to keep rent and other obligations current or have moved in with friends or relatives.

The recently enacted $900 billion relief package will provide some assistance to renters but won't make renters or landlords anywhere close to whole. The Federal Reserve of Philadelphia projects that, by the end of 2020, 1.34 million renter households (about 4 percent), will owe $7.2 billion in back rent, or about $5,400 per household. Mom-and-pop rentals are likely to struggle in 2021. Even with stronger overall economic growth, rising rental delinquencies may pressure owners of smaller rental properties to sell.

Where will the housing market go in 2021 and what are some possible wildcards?

The Wells Fargo economists provide multiple answers to the last question. They see home sales and new home construction strengthening further this year and, as vaccines gain the upper hand, the stage will be set for a strong spring and summer.

New home sales are projected to increase 16 percent this year to 940,000 sales, the most since 2006. Existing home sales will rise 4.0 percent and existing condominiums and co-ops 2.6 percent. The numbers would be higher if inventories were larger but that should improve moderately in 2021. As the pandemic eases, more people will put their homes on the market, relocate for new employment, or resume plans to downsize. Foreclosure and distressed sales will also increase from their current low levels.

Single-family construction is expected to build on last year's 11 percent gain in single-family starts, rising another 7.1 percent in 2021. There have been concerns that some of the recent surge in home buying came from a temporary, pandemic-driven need for more space to work remotely and accommodate children's education needs. Even if these influences decline, stronger job and income growth, low mortgage rates, and demographic influences should loosen mortgage underwriting and send demand higher.

The lack of affordable homes remains the biggest challenge for the housing market and the authors believe buyers will look to the suburbs and exurbs of their current market or relocate to more affordable second-tier large metro areas, and rapidly growing larger metro areas. There is evidence of a marked acceleration in relocations, home sales, and new construction in these areas. Growth is also strong in many mid-sized and smaller markets, driven by both the need to find more affordable communities to live in and the greater ability to work remotely.

The intensifying pandemic and ongoing rollout of vaccines remain the biggest wild cards for the housing outlook, as well as the overall economy. Rising infections and overwhelmed hospital systems are expected to keep many potential buyers on the sidelines in the early weeks of 2021 until widespread vaccinations take hold. Shortages of buildable lots, some key building materials and skilled workers will also remain a challenge for homebuilders, particularly tract builders targeting middle-income and lower-middle-income buyers.