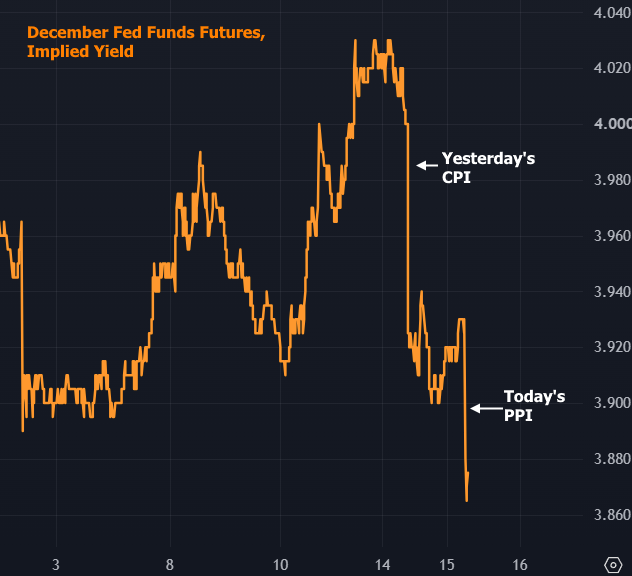

The Producer Price Index (PPI) is not normally a huge market mover, but it has its moments of moderate impact. Today is such a moment as PPI did its best to mimic yesterday's sharply lower CPI. There were also big revisions to previous months which brought annual PPI a full 1.0% lower from last month's initial reading (5.5% today vs a 6.0 previous reading, revised from 6.5% when initially reported). Fuel prices loom large in this data, as evidenced by Core monthly PPI at 0.2 vs 0.3. Unlike yesterday, most of today's shift was seen in revisions to previous months--especially May (headline revised from 1.1 to 0.6). Laundry list of little numbers aside, bonds like it. Fed Funds Futures improved. Treasuries and MBS have gone from modestly weaker to moderately stronger after the report.

As with yesterday, expect shorter term yields to improve more, and be cognizant of the risk that a breakout in oil prices could give bonds second thoughts about the AM rally.