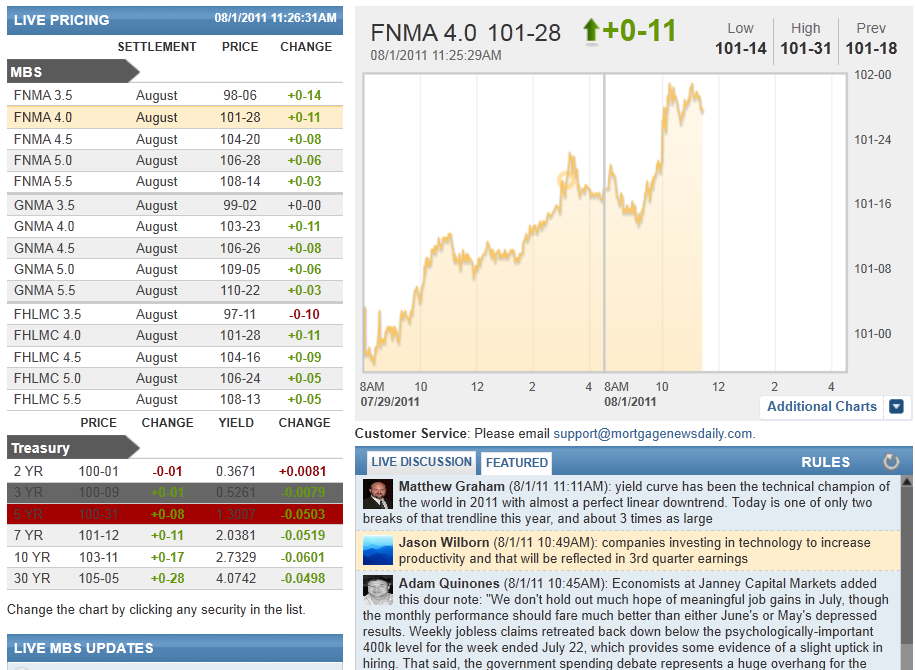

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:02 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:44AM :

Senate Aims for Monday Vote on Debt Limit

(Reuters) - The U.S. Senate will try to vote sometime on Monday on legislation to raise the federal government's debt limit and cut deficits over the next decade, Senate Majority Leader Harry Reid said on Monday.

"We expect to vote on a compromise hopefully during today's session sometime," Reid said at the start of the Senate's session.

(Reporting by Richard Cowan and Donna Smith)

10:20AM :

ALERT:

Rallying Big on Weak Econ Data and Debt Deal Hope

By far and away, MBS and Treasuries are at their strongest levels since last Fall after the weak ISM report fueled fires stoked by the promise of an impending debt-ceiling resolution. Fannie 4.0's are up 13 ticks at the moment at 101-30 and 10yr yields have dropped over 7 bps to 2.72. Naturally, rates will be better today, but we wouldn't expect them to fully reflect the amount of gains in MBS until things settle down in general. If you already had rates, reprices for the better are possible if current levels prove to be more than fleeting.

10:08AM :

ECON: ISM Manufacturing Falls to Lowest Level Since 2009

The Institute for Supply Management's Purchasing Manager's Survey fell to 50.9 in July after a 55.3 reading in June. Economists had been expecting 54.9 and today's index level is the lowest since 8/2009. New orders were down slightly, from 51.6 to 49.2 and the "Prices Paid" component was significantly lower, moving from 68.0 in June to 59.0. The report also reinforces the ongoing bleakness of the employment picture with that component of the index falling from 59.9 to 53.5.

10:03AM :

ECON: Construction Spending Hits 6 Month High

(Reuters) - U.S. construction spending unexpectedly rose in June to touch a six-month high as an increase in private outlays offset a drop to a four-year low in public spending, a government report showed on Monday. Construction spending advanced 0.2 percent to an annual rate of $772.32 billion, the Commerce Department said. May's construction spending was revised to a 0.3 percent increase rather than the previously reported 0.6 percent decline. Economists polled by Reuters had expected construction spending to be flat in June. Overall construction spending fell 4.7 percent from a year ago. Private construction spending rose 0.8 percent to a seven-month high as an increase in nonresidential outlays offset a second straight month of declines in spending on residential projects. Spending on public construction projects dropped 0.7 percent to $278.91 billion, the lowest level since March 2007. The decline reflected weak spending on federal projects, which dropped 2.2 percent. State and local government spending fell 0.6 percent to the lowest level since November 2006. (Reporting by Lucia Mutikani; Editing by Neil Stempleman)

9:58AM :

US CDS Costs Drop as Debt Deal Nears

(Reuters) - The cost of insuring U.S. debt with credit default swaps fell on Monday, with short-dated swaps dropping the most, as investors regained confidence the U.S. would avoid a near-term debt default.

Five-year credit default swaps (CDS) on U.S. government debt fell to the lowest since July 11 at 50 basis points, down 10 bps on the day, according to data provider Markit.

Thinly traded one-year swap costs, meanwhile, dropped 30 basis points to 45 basis points, their lowest since July 5. The move reversed the curve inversion that held for most of July.

The short-term debt insurance costs rose above those of the more liquid 5-year swaps in early July as investors fretted a near term default was more likely.

One-year debt costs reached a record 82 basis points on Thursday. That would mean it cost $82,000 to insure $10 million in Treasuries.

The drop in CDS costs on Monday reflected increasing confidence that lawmakers will to pass a deal, which raises the $14.3 trillion debt ceiling and cuts about $2.4 trillion from the deficit over the next decade. For more, see (Reporting by Karen Brettell and William James; Editing by Theodore d'Afflisio)

9:27AM :

ALERT:

MBS Gains Largely Intact. Slightly Weaker Than Friday's Close

Fannie Mae 30yr Fixed 4.0 MBS coupons are down 3 /32nds from Friday's last levels, from 101-18 to 101-15. But 101-15 marked a gain of 48/32nds on Friday, and with lots of technical trading around 101-10 last week, this morning's levels are thus far reinforcing Friday's gains. It's a somewhat similar picture for 10yr notes as 2.82 was the last week's lowest yield before the aggressive rally in the last 2 hours of Friday. So despite 10's being slightly higher in yield this morning, they remain under 2.82 so far. The bottom line is that day-over-day indications may be showing a slight loss, but gains have held about as well as they could. Assessing how well we're doing this morning is one thing, but far more uncertain is how trading will evolve over the next few days. Markets already know there will be more political headlines during that time than they'd care to digest, and then those must be balanced against Friday's NFP, both in terms of reacting to the report itself and positioning for it over the course of the week. It may be a very interesting week, and most likely one that lends itself better to a "watch and react" philosophy as opposed to planning on likelihoods of various outcomes. Nimbleness is the virtue for now.

8:54AM :

Debt Deal Avoids Default. Downgrade Still at Risk. Vote Forthcoming

(Reuters) - Congressional leaders scrambled to line up Republican and Democratic votes on Monday for a White House House-backed deal to raise the U.S. borrowing limit and avert an unprecedented debt default. With votes expected later in the day, the Democratic-led Senate is expected to pass the deal, which raises the $14.3 trillion debt ceiling and cuts about $2.4 trillion from the deficit over the next decade. But it may face tougher opposition in the House of Representatives where both conservative Tea Party supporters and liberal lawmakers have expressed dissatisfaction with the agreement. Congressional leaders were consulting their membership to determine who would vote for the deal and who would be against it. Liberals have vowed to oppose it out of concern it would cut spending for popular social programs. In addition to the $2.4 trillion deficit cut, a new congressional committee is to recommend by late November a further $1.5 trillion in cuts through tax reform and other deficit-reduction measures. While the deal means the United States is unlikely to default, it is far from certain whether the plan agreed by the White House and lawmakers goes far enough in reducing the deficit to appease credit ratings agency S&P, which has threatened to strip America of its top-notch AAA rating.

7:48AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Jason Wilborn : "companies investing in technology to increase productivity and that will be reflected in 3rd quarter earnings"

Andrew Horowitz : "Too many other factors can lead to a weak GDP figure, plus as both MG and AQ have said it is a number that looks backwards too far it is not a forward indicating number"

Adam Quinones : "NFP = tactical play motivation. GDP = strategic play motivation. NFP =checkers. GDP = chess"

Brent Borcherding : "I hear that, and I'm definitely on the wrong side of this one. I just think we've seen some + NFP in the last year, that were good #s but didn't turn out to be a trend. GDP showed that there is a trend and it's ugly. I'm wrong, but that's how I saw it."

Matthew Graham : "that's my thing BB... GDP is super interesting, and given the epic overtones in the market right now, super important, but in terms of actually gauging likely future direction / challenges, NFP is the definitive specific metric on the most important component of the economic recovery"

Adam Quinones : "yep MG"

Matthew Graham : "i get that, and agree, but would you say that NFP speaks more to present + future whereas GDP more to present + past?"

Adam Quinones : "at this point we're gonna start hearing whispers out of Jackson Hole regarding another QE program."

Adam Quinones : "right now i think the GDP data is extra important for one big reason, the outlook for more QE is based on the Fed's call for stronger growth in 2nd half of year."

Brent Borcherding : "I know regularly you'd be right, and not saying you are not, but what kind of positive NFP report would out do a revised, .4% 1st Qtr and 1.3% 2nd Qtr GDP. The magnitude of those 2 disappointments seem impossible to equal in 1 NFP."

Matthew Graham : "BB, i'd almost always put more weight on NFP than GDP. I'm not sure anything gets more weight than NFP"

Adam Quinones : "yeh it seems, barring unexpected voting issues in the House, that markets are ready to shift the focus back to econ fundamentals. "

JudeB : "aq or mg, if debt deal gets approved, could we see bonds improve more or just hope for them to steady?"

Brent Borcherding : "MG--Are you putting more weight on NFP than GDP?"

Matthew Graham : "S&P rebounded to 1288+ now after hitting 1280's on initial slide"

Adam Quinones : "yeh. crazy AH. Hedge Ratios def shortening up today."

Matthew Graham : "(Reuters)TOM PORCELLI, U.S. ECONOMIST, RBC CAPITAL MARKETS, NEW YORK

"I think what makes this report -- what gives it sort of nasty undertones, is this new orders index slipping below 50. For an economy that's struggling here, this just adds credence to that notion.

"ISM is a sentiment indicator; it's not based on real activity. From that perspective you could maybe make an argument that a lot of the uncertainty that has been put forward by the debt debate may have found its way in there"

Andrew Horowitz : "AQ check out the 4.5/4 swap "

Matthew Graham : "RTRS - ISM U.S. MANUFACTURING PRICES PAID INDEX 59.0 IN JULY (CONSENSUS 64.5) VS 68.0 IN JUNE "

Matthew Graham : "RTRS- ISM U.S. MANUFACTURING NEW ORDERS INDEX 49.2 IN JULY VS 51.6 IN JUNE "

Matthew Graham : "RTRS - ISM REPORT ON U.S. MANUFACTURING SHOWS PMI AT 50.9 IN JULY (CONSENSUS 54.9) VS 55.3 IN JUNE "

Adam Quinones : "yeh it seems, barring unexpected voting issues in the House, that markets are ready to shift the focus back to econ fundamentals. "

Matthew Graham : "Best two sentence recap of debt deal developments I've read so far: "For all the down-to-the wire drama, the deal leaves the hardest

questions unanswered and sets in motion years of fiscal pain. It

imposes spending caps for the next 10 years, but leaves the details of

what programs would be cut to congressional committees.""

Adam Quinones : "yikes: (Reuters) - HSBC will shed 30,000 jobs as it retreats from countries where it is struggling to compete, Europe's biggest bank said on Monday after it reported a surprise rise in first-half profit."

Adam Quinones : "(Reuters) - Europe, Asian factory growth stalls in July: (Reuters) - Factories in Asia and Europe expanded in July at the weakest rate since major industrial powers were struggling through the 2009 recession, adding to concerns over world growth.

While stock markets rose on signs of a last minute solution that would avoid a U.S. debt default, manufacturing purchasing managers indexes (PMIs) provided the latest evidence of a slowing global economy.

The euro zone manufacturing PMI, which gauges "

Adam Quinones : "bad news for jobs..."

Adam Quinones : "The lack of movement in the bond market may reflect nervous sentiment about the broader economy after the latest GDP report indicated that Q1 and Q2 GDP grew at just 0.4% and 1.3%, respectively. Plenty of leading indicators this week have the potential to improve the economic outlook but they're more than likely going to confirm a dour situation and keep safe haven assets richly priced. "