Equity markets are rallying and bond yields are slightly higher after President Obama late Sunday stated that leaders of both parties reached an agreement to lift the debt ceiling, avoid default, and reduce the annual budget deficit.

(Reuters) - Congressional leaders scrambled to line up Republican and Democratic votes on Monday for a White House House-backed deal to raise the U.S. borrowing limit and avert an unprecedented debt default. With votes expected later in the day, the Democratic-led Senate is expected to pass the deal, which raises the $14.3 trillion debt ceiling and cuts about $2.4 trillion from the deficit over the next decade. But it may face tougher opposition in the House of Representatives where both conservative Tea Party supporters and liberal lawmakers have expressed dissatisfaction with the agreement. Congressional leaders were consulting their membership to determine who would vote for the deal and who would be against it. Liberals have vowed to oppose it out of concern it would cut spending for popular social programs

The S&P 500 looks to open 13 points higher (+1.03%) at 1,301.50 and Dow futures are up 134 points (+1.11%) at 12,220. Treasuries, a bit surprisingly, have hardly reacted to the news after a flight to quality brought the benchmark 10-year Treasury yield down 16 basis points on Friday. The 10-year note is just one basis point higher at 2.80% in early trading, while the two-year yield is stable at 0.36% and the 30-year yield is two basis points higher at 4.14%. Mortgages are performing poorly though. The Fannie Mae 4.0 MBS coupons is -3/32 at 101-15. Yield spreads are wider into lower prices.

The lack of movement in the bond market may reflect nervous sentiment about the broader economy after the latest GDP report indicated that Q1 and Q2 GDP grew at just 0.4% and 1.3%, respectively. Plenty of leading indicators this week have the potential to improve the economic outlook but they're more than likely going to confirm a dour situation and keep safe haven assets richly priced.

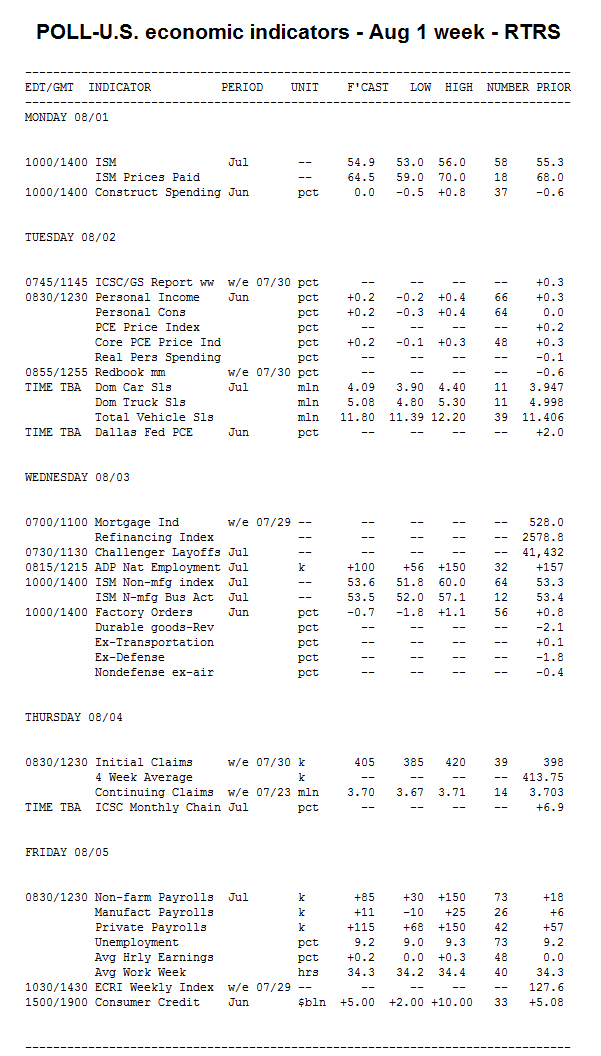

Key Events This Week:

Monday:

10:00 - Forecasts for July's ISM Manufacturing Index depend on whether one thinks there will be a rebound in exports. That component declined in June to its lowest level since the end of the recession; some forecasters assume it was just a temporary shock owing to the Japanese earthquake, so July should see a pickup; other see exports continuing to dwindle. But both camps agree the manufacturing sector continued to grow in July. The consensus forecast is 55.0, just down from 55.3 a month before and a faster pace than the 53.5 in May.

"Export orders unexpectedly slumped [in June], in part on talk of slow demand from a still-earthquake stressed Japan," said economists at Janney Capital Markets. "For July, there's a good chance that some of this downdraft reverses to a more normal level. We continue to view foreign demand for US-manufactured capital goods from developing nations as one of the strongest sources of strength for the manufacturing sector."

Forecasters at IHS Global Insight point out that orders and shipments averaged just 53.1 in June, setting a sluggish tone for this report, while employment in June jumped to 59.9, which they consider "solid" but unsustainable.

"The major drag, however, is likely to be inventories which spiked over 50 to 54.1 last month," they added "This volatile component cannot sustain such strength in a tepid world where production plans are being scaled back."

10:00 - Construction Spending fell 0.6% in May to mark its sixth straight loss, bringing spending to its lowest level in about 11 years and nearly 6% lower than one year ago. For June, forecasts range from a 0.4% decline to a 0.8% rebound; the median estimate is flat.

"We look for fairly stagnant construction spending in June," said economists at Citigroup. "Private expenditures probably increased, based on the rise in housing starts and the ongoing recovery in business investment. These gains likely were largely offset by another drop in public expenditures.

Citi added that if their June estimate is correct, then construction spending subtracted about one-quarter percentage point from second quarter GDP growth.

According to IHS Global Insight, there should be gains in single-family residential construction and private nonresidential construction, offset by another drop in public construction.

Treasury Auctions:

- 11:30 - 3-Month Bills

- 11:30 - 6-Month Bills

Tuesday:

8:30 - Weakness is the expectation on both sides of the Personal Income & Outlays report. With just 18,000 news jobs created in June, incomes are expected to advance a marginal 0.2% in June, following gains of 0.3% in the prior two months. Consumption is expected to be held back by anemic auto sales, still-high gas prices, and pessimistic consumer sentiment, translating into a 0.2% uptick following a flat May and 0.3% gain in April.

"The negligible 18k increase in nonfarm payrolls coupled with no growth in hourly earnings points towards falling nominal consumer incomes, a problem that's even greater in light of year-over-year increases in commodities prices," said economists at Janney Capital Markets. "Overall, the consumer picture isn't looking very pretty, and with fiscal stimulus off the table and a risk of deep federal spending cuts, the only thing that can help may well be time."

Meantime, the core PCE price index - the Fed's preferred measure of inflation - is anticipated to report a year-over-year rate of 1.4%, versus 1.2% in May.

"Spiraling inflation is currently not one of our fears, given the considerable slack that exists in the labor market and the sluggish level of wage and income growth," said economists at IHS Global Insight. "In addition, inflation expectations as measured by the Conference Board survey have fallen in July."

Treasury Auctions:

- 11:30 - 4-Week Bills

Wednesday:

8:15 - The ADP Employment Report came in higher than anticipated in June as it reported the creation of 157,000 private jobs. That caused economists to revise their estimates for the nonfarm payrolls quite a bit higher - one, for instance, revised his forecast to 175k from 100k - thus making the shock of sluggish growth all the more shocking. The report is less likely to be influential this month, but even so, everyone looks at the number. The median estimate this month is 100k, with estimates from 60k 150k.

"Our forecast of a 135k increase in ADP's private employment is consistent with our 85k call for nonfarm payrolls," said economists at Nomura Global Economics after noting the differences between the two reports' methodologies. No more commentary was available.

10:00 - The ISM Non-Manufacturing Index, a nationwide measure of the services, construction, and financial sectors, is actually supposed to pick up the pace a bit in July. Economists are forecasting a 53.7 score, up a little from 53.3 in June but a slower pace than the 54.6 two months before. With two days before the monthly employment report, this report is likely to get quite a bit of scrutiny.

"After declining by 1.3 points in June to 53.3, we forecast a small rise in the non-manufacturing index to 53.7 in July," said economists at Nomura Global Economics. "Service sector job creation, which accounts for the lion's share of the nation's jobs, has slowed over the past few months so the employment index within July's survey will be particularly important."

Thursday:

8:30 - Initial Jobless Claims will take some on added importance after the report finally broke through the 400k barrier last week. New claims fell 24k in the week ending July 23 to 398k, its lowest level since early April. The report, considered "clean" by the Dept. of Labor, brought the four-week average down to 414k. If that level gets closer to the 400k mark it will signal renewed hopes for job growth.

"We have now moved beyond the auto retooling period and the Minnesota government layoffs have been absorbed so we expect lower readings from the claims data in coming weeks," said economists at Nomura Global Economics.

Friday:

8:30 - With second-quarter GDP growth estimated at just 1.3%, July's Employment Situation needs to do post a big number to get people optimistic about this economic recovery. So far, job growth forecasts for range from 30k to 150k, and the median estimate at 90k. Those are all pretty weak, but predictions should change as new data is released during the week.

"The government picture is bleak given state and local cutbacks kicking in at the start of the fiscal year, combined with temporary layoffs of just over 20,000 in Minnesota during its government shutdown," said economists at IHS Global Insight. "Overall we expect 50,000 jobs to be created, with 115,000 private jobs offset by a loss of 65,000 government jobs."

Economists at Janney Capital Markets added this dour note:

"We don't hold out much hope of meaningful job gains in July, though the monthly performance should fare much better than either June's or May's depressed results. Weekly jobless claims retreated back down below the psychologically-important 400k level for the week ended July 22, which provides some evidence of a slight uptick in hiring. That said, the government spending debate represents a huge overhang for the labor markets. Imagine you're running a firm that get 50% of its revenue from government contracts. Would you hire long term employees when federal discretionary spending is at risk of dropping 5% or more? Realistically, no, which is only but one of the ways that federal fiscal decisions can negatively impact the private sector."

The Unemployment Rate, which ticked up one-tenth to 9.2% in June, is expected to hold steady this month. Some economists even think it could rise to 9.4%.

3:00 - Consumer Credit climbed for the seventh straight month in April with a $6.3 billion gain, but strong installment lending from the federal government and commercial banks were responsible for the increase, whereas revolving debt - mostly credit cards - fell back $0.9 billion. The June report is anticipated to show a $5 billion expansion, but the report is all about the details; what economists look for is a sign that consumers are ready to spend again. So far, this report says they aren't.

"After falling to record lows during the financial crisis, consumer credit began growing in October," said economists at Nomura Global Economics. "Growth has been one-sided, however, fueled by non-revolving credit, the majority of which represents auto and student loans. Revolving credit (i.e., credit cards) remains largely out of favor with households, increasing in only 2 of the past 33 months. In May, consumer credit expanded by $5.1 billion and consensus is looking for a similar $5.0 billion increase in June."