MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:01 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

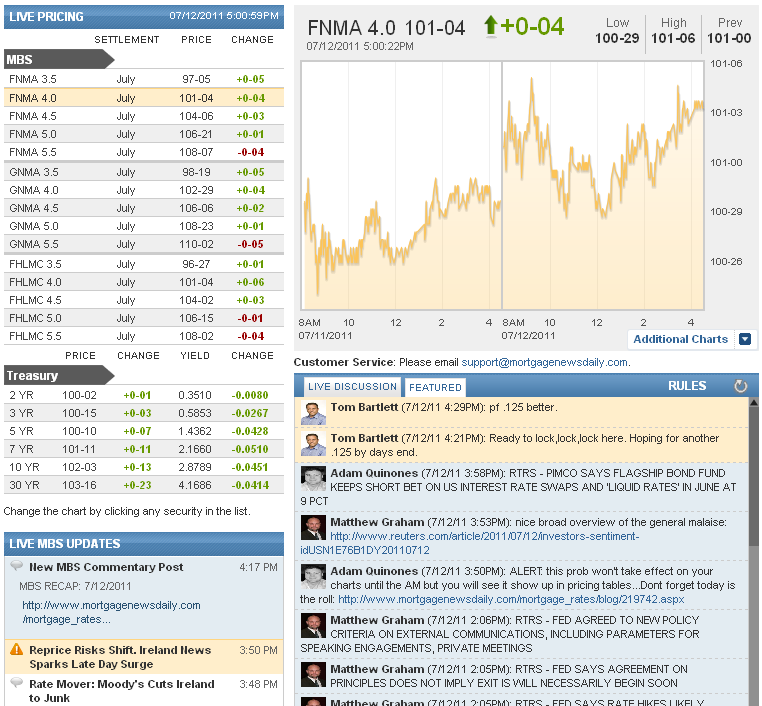

3:50PM :

ALERT:

Reprice Risks Shift. Ireland News Sparks Late Day Surge

Moody's downgrade of Ireland's credit rating junk status this afternoon breathed a small amount of fresh air into what had been a mostly sideways bond market. Fannie 4.0's are now in line with their highs of the day, currently up 3/32nds overall at 101-03. 10yr yields dropped to 2.89. No major significance here and not a huge uptick in volume. We're simply looking at EU-related headlines giving a boost to bond markets during hours not normally associated with the presence of salient market guidance. It means the reprices for the better are now more likely than reprices for the worse, though not guaranteed, or even that likely considering the lateness in the day and the upcoming MBS Settlement.

3:48PM :

Rate Mover: Moody's Cuts Ireland to Junk

This just hit news wires and it's helping U.S. interest rates move lower late in the session thanks to a "flight to safety". This is the definition of "contagion". (Reuters) - The euro fell against the U.S. dollar on Tuesday after Moody's Investors Service cut Ireland's credit rating to junk status, saying the country will likely need additional rounds of official financing before it can return to international capital markets. Moody's cut Ireland's ratings by one notch to Ba1 from Baa3 and kept a negative outlook on the rating. The euro EUR= last traded down 0.3 percent at $1.3987. The session low of $1.3835 was hit earlier in the global session. The euro also lost ground against the Japanese yen and Swiss franc, slipping 1.3 percent against the yen EURJPY= and 1 percent against the franc EURCHF= in late afternoon New York trade.

3:42PM :

The Day Ahead: Bernanke, TSY Auction, EU Contagion

Apart from the 7am MBA Applications Data, the only scheduled economic release of the morning will be Import Prices at 830am. Not a top-shelfer, but not deserving to be ignored either. Even so, it lacks the cachet of what's to follow. At 10AM Fed chairman Ben Bernanke testifies before the House Committee on Financial Services at the Semiannual Monetary Policy Report to the Congress in Washington. Nomura notes this is Bernanke’s first appearance since his June 22nd FOMC press conference. “In the wake of the very weak June employment report, his testimony is likely to reflect heightened concerns about the ‘frustratingly slow’ labor market recovery,” they wrote “As in the last meeting in March, he will likely emphasize the importance of improving the long-term fiscal situation, and encourage the House to raise the debt ceiling. That being said, he may suggest withholding fiscal tightening in the near term.” Soon after that, if the 10yr note auction offers similarly bullish results to today's 3yr auction, we could see more ratcheting down of benchmark yields and higher MBS prices. Keep in mind that sometimes this ratcheting merely takes the form of CONFIRMING previous gains. There's tons of econ on Thursday and Friday as well as another Treasury Auction to digest. Those factors may keep a lid on whatever reaction to tomorrow's 10yr auction might otherwise be seen if it existed in a vacuum. Sprinkling layers of complexity into the picture tomorrow is the ongoing potential for headlines out of the EU. Last night was big in terms of volume, but the domestic session brought prices and yields back very close to where they ended the previous day. As always, full details of this week's schedule of potential market movers can be found here:

3:15PM :

New MBS Commentary Post

2:49PM :

FOMC on Housing: Same Old Depressing Story

Below are excerpts from the FOMC Minutes that reference housing and the mortgage market. As any industry professional might expect, the Fed's findings were not pleasant. Here they are: "Activity in the housing market remained depressed, as both weak demand and the sizable inventory of foreclosed or distressed properties continued to hold back new construction. Starts and permits of new single-family homes were essentially unchanged in April and May, and they stayed near the very low levels seen since the middle of last year. Sales of new and existing homes remained at subdued levels in recent months, while measures of home prices fell further"….. "Despite efforts aimed at mitigation, foreclosures continued to add to the already very large inventory of vacant homes, putting downward pressure on home prices and housing construction"….."Moreover, the recovery remained subject to some downside risks, such as the possibility of a more extended period of weak activity and declining prices in the housing sector, the chance of a larger-than-expected near-term fiscal tightening, and potential financial and economic spillovers if the situation in peripheral Europe were to deteriorate further"……."The Federal Reserve continued its competitive sales of non-agency residential mortgage-backed securities held by Maiden Lane II LLC over the intermeeting period. Although the initial offerings of these securities were well received, investor demand at the most recent sales was not as strong, a development consistent with the declines in the prices of non-agency residential mortgage-backed securities over the intermeeting period."

2:29PM :

New Rules Clamp Down on Chatty Fed Officials

(Reuters) - The Federal Reserve is making a new push to control the often wayward communications of its top officials, issuing detailed rules on Tuesday that dictate specifically what they can and cannot do. The Fed -- the U.S. central bank -- has come under fire for speaking with a dissonant voice, and sometimes allowing details of its highly market-sensitive policy meetings to leak to the media or former staffers. "To the fullest extent possible, Committee participants will refrain from describing their personal views about monetary policy in any meeting or conversation with any individual, firm, or organization who could profit financially from acquiring that information," the Fed said in a statement.

Last year, the Fed announced Vice Chair Janet Yellen would chair a subcommittee on communications aimed at clarifying central bank policy on the matter. The report was a result of that effort.

2:28PM :

Auction Results Giveth, FOMC Minutes Taketh Away

The 3 or so 32nds of improvement seen in Fannie Mae 4.0's after the 3yr note auction have been followed by similar magnitude of losses after the FOMC minutes. In fact, we're right back to 1pm levels of 100-31. 10yr benchmarks have risen slightly in yield, but remain inside the higher yields just before auction time. Markets may be a bit exhausted from an all-nighter with Greece, and while they've paid respect to the seriousness of the data with some token volatility, there's no discernible directional move. In other words, high volume, choppy, but sideways... Still produces yawns, even though those yawns sound more exciting. You try one! "YAWWWN!"

2:26PM :

Fed Officials Divided on Further Stimulus

(Bloomberg) - Federal Reserve policy makers disagreed on whether additional monetary stimulus will be needed even if the outlook for economic growth remains weak, minutes of their meeting last month showed. “A few members noted that, depending on how economic conditions evolve, the committee might have to consider providing additional monetary stimulus, especially if economic growth remained too slow to meaningfully reduce the unemployment rate in the medium run,” the Federal Open Market committee said in the minutes of its June 21-22 meeting. “On the other hand, a few members viewed the increase in inflation risks as suggesting that economic conditions might well evolve in a way that would warrant” the FOMC “taking steps to begin removing policy accommodation sooner than currently anticipated.” Policy makers cut their forecasts for growth this year before a July 8 government report showed employers added jobs at the slowest pace in nine months in June. Chairman Ben S. Bernanke at a June 22 news conference said growth will pick up as energy prices subside and disruptions of parts from Japanese factories ease, while also leaving the door open to additional stimulus. Some members of the FOMC “saw the recent configuration of slower growth and higher inflation as suggesting that there might be less slack in labor and product markets than had been thought,” the minutes said. In that case, “the withdrawal of monetary accommodation may need to begin sooner than currently anticipated in financial markets.” All but one of the FOMC members agreed on the sequence for an exit from record monetary stimulus. The minutes said the discussion was part of “prudent planning” and didn’t imply that an exit would take place soon. The minutes said the committee will determine “ the timing and pace of policy normalization.” The first step will be to “cease reinvesting some or all payments of principal” on securities holdings in the Fed’s portfolio.

1:36PM :

MBS Improve After Auction. FOMC Minutes Ahead

Fannie 4.0s are up 1/32nd on the day now at 101-01. They had been at 100-29 just before auction results. With the auction being reasonably strong, but with FOMC Minutes still ahead at 2pm, not to mention the week's remaining auctions and econ, it's understandable that bond markets aren't rallying aggressively. 10yr notes are on a long term inflection point at 2.915 at the moment. It's a short term inflection point as well, having been the floor that prevented lower yields in last night's low volume, but then the ceiling blocking higher yields in today's strong volume. It will take ongoing bullish suggestions from data and auctions to confirm any lower in yield. "Confirm" in used here in the technical context meaning that it would take yields lower than 2.915, with good volume, and with enough staying power to endure the rest of the week's events and data. In other words, so far so good, waiting for the verdict from the rest of the week's expected guidance to know A) if we're going any lower and B) how strong the possibility is that 10yr yields would stay under 2.915.

1:19PM :

3 Year Auction Met With Healthy Demand

The high yield for today's auction came in at 0.670% high yield versus a 1pm "when-issued" yield of 0.683% (effectively, when-issued is analogous to a forecast of where markets think the high yield will be). Everything about the auction was in line with recent averages except for the notable uptick in direct bidder participation (direct bidders are financial institutions that place their bids directly with the Treasury, but who are not Primary Dealers). This is exactly what should have happened without the Fed buying Treasuries in the open market after the auctions (QEII is over). At 3.22, the bid-to-cover ratio was slightly higher than longer moving averages, but slightly lower than the 3.25 average of the last 4 auctions. Still, very much in line... Indirect bidding was right in line with recent averages (this group includes foreign and international monetary authorities that place their bids through direct bidders such as the NY Fed).

12:30PM :

Auction Concession, Stock Lever Slow Bond Rally

"Rate sheet influential" MBS prices are near their intraday lows and stocks have clawed back to unchanged on the day after experiencing sharp overnight declines. This equity reversal has been a slow, somewhat meandering process, one that interest rate traders haven't pushed back against, not with $66 billion in Treasury auctions ahead. The Fannie Mae 4.0 MBS coupon is now -4/32 at 100-29 and the benchmark 10-year Treasury note is -3/32 at 101-20. These price declines are enough to warrant reprices for the worse, especially if your lender released rate sheets early in the day (before 10AM eastern). The next event on the market's "to-do list" is a $32bn 3-yr note auction at 1pm. There are essentially two opposing forces at work in the auction process. The Treasury on one end, who’d like to be paid the highest price possible (lowest yield) and on the other end we find market participants that bid on debt inventory who’d like to walk away paying the lowest price possible (highest yield). So in that sense, with $66 billion in debt auctions approaching in the days ahead and the market having rallied prices significantly higher since the last round of auctions, market participants are simply trying to “give way,” or make room for that debt by trading prices lower (yields higher). This doesn’t mean that bond market sentiment is shifting bearishly for the month ahead, we're just witnessing a short-term strategy aimed at cheapening up prices before the auction process begins. There is another wildcard to contend with though: this will be the first Treasury auction since the Fed stopped buying Treasuries (end of QEII). If demand is as weak as it was in the previous auction cycle (just before the end of the 2nd quarter), reprices for the worse would be likely. The stock lever is also playing a role in price action though. S&P futures are currently flat at 1318. This is a key technical level, failure to break it would lead to stock selling and lower interest rates.

11:24AM :

REITs Raising Money to Fund Housing Finance

REIT's have clearly become, with their leverage of 5x1, the dominant pool of new capital that the government was looking for as the GSE's need to become a smaller portion of the mortgage market......(Bloomberg) - Annaly Capital Management Inc, the largest U.S. mortgage real estate investment trust, said it plans to sell 100 million shares in its third public stock offering this year. The proceeds will be used to buy mortgage-backed securities, the New York-based company said in a statement today. Annaly has sold 150 million shares this year for a total of about $2.6 billion, according to data compiled by Bloomberg. The REIT, led by Chairman and Chief Executive Officer Michael Farrell, in recent years has expanded from investing in government-backed mortgage bonds to overseeing distressed-debt buyers and a securities firm. Annaly also started financing middle-market companies and home lenders, and entered ventures to make commercial real estate loans, after the worst financial crisis since the Great Depression curbed sources of lending. Mortgage REITs led by Annaly and American Capital Agency Corp. (AGNC) raised almost $6 billion through stock sales in December, January and February, helping to bolster the market for mortgage-backed securities. Investment companies including Pacific Investment Management Co., Avenue Capital Management and Angelo, Gordon & Co. are creating mortgage REITs and also are selling shares.

11:17AM :

Ginnie Mae Has No FICO Minimum. Lenders Do.

When one hears about a particular lender claiming, "'ABC Mortgage' is now doing FHA loans with a 620 score!!!" the odds are that it is a negotiated deal with a larger investor. Yes, there are some cases where it is a portfolio lender or direct Ginnie Mae issuer, but for the typical conventional or government products, if something falls outside the overlay guidelines usually some negotiation has taken place. What is Ginnie Mae's minimum FICO for a FHA loan? A trick question - there is none. All Ginnie requires is that the loan be insured for final pool certification which must occur within a given period. So in effect, typically whatever minimum FICO overlay levels that are out there are a combination of FHA loan delinquency studies by servicers and negotiations with the companies that sell to them. But before you go calling the Wells' & Chase's of the world trying to wangle 500 FICO borrowers for condos, remember that investors are unlikely to disregard their underwriting and overlays entirely. It is a give & take process, and benefits accrue to high volume, loyal, well capitalized counterparties who know what they're doing - but there are rumors of cracks in the ice in certain underwriting areas IF they make sense - and you didn't hear this from me.

11:17AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "RTRS - PIMCO SAYS FLAGSHIP BOND FUND KEEPS SHORT BET ON US INTEREST RATE SWAPS AND 'LIQUID RATES' IN JUNE AT 9 PCT"

Matthew Graham : "nice broad overview of the general malaise: http://www.reuters.com/article/2011/07/12/investors-sentiment-idUSN1E76B1DY20110712"

Adam Quinones : "ALERT: this prob won't take effect on your charts until the AM but you will see it show up in pricing tables...Dont forget today is the roll: http://www.mortgagenewsdaily.com/mortgage_rates/blog/219742.aspx"

Matthew Graham : "RTRS - FED AGREED TO NEW POLICY CRITERIA ON EXTERNAL COMMUNICATIONS, INCLUDING PARAMETERS FOR SPEAKING ENGAGEMENTS, PRIVATE MEETINGS"

Matthew Graham : "RTRS - FED SAYS AGREEMENT ON PRINCIPLES DOES NOT IMPLY EXIT IS WILL NECESSARILY BEGIN SOON "

Matthew Graham : "RTRS - FED SAYS RATE HIKES LIKELY ACCOMPANIED BY CHANGES TO RATE ON EXCESS RESERVES, ADJUSTMENTS TO LEVEL OF RESERVES"

Matthew Graham : "RTRS - FED SAYS FURTHER TIGHTENING STEPS WOULD INCLUDE MODIFIED FORWARD GUIDANCE, TEMPORARY RESERVE DRAINS, FOLLOWED LATER BY RATE HIKES "

Adam Quinones : "to the Fed I say..yeh right...good luck selling MBS if you raise rates."

Matthew Graham : "RTRS - A FEW FED OFFICIALS EXPRESSED UNCERTAINTY ABOUT THE EFFICACY OF MONETARY POLICY IN CURRENT CIRCUMSTANCES "

Matthew Graham : "RTRS - A NUMBER OF FED OFFICIALS JUDGED RISKS TO INFLATION OUTLOOK AS TILTED TO THE UPSIDE "

Matthew Graham : "RTRS - FED EXPECTS INFLATION TO SUBSIDE TO LEVELS AT OR BELOW THOSE CONSISTENT WITH DUAL MANDATE "

Matthew Graham : "RTRS - FED: RECENT DETERIORATION IN JOBS OF PARTICULAR CONCERN BECAUSE LABOR MARKET UNCERTAINTY A KEY DRAG ON CONSUMER SPENDING "

Adam Quinones : "important one....RTRS - FED SAYS SALES OF SECURITIES LIKELY TO BEGIN SOME TIME AFTER FIRST INCREASE IN FED FUNDS RATE "

Matthew Graham : "RTRS- FED CONCERNED ABOUT GREECE AND SPREADING EUROPEAN DEBT WOES, COULD CAUSE "SIGNIFICANT STRAINS" IN U.S. "

Matthew Graham : "RTRS - A FEW FED OFFICIALS THOUGHT FED MIGHT NEED TO TIGHTEN POLICY SOONER THAN EXPECTED IF INFLATION RISKS RISE -- FED JUNE MEETING MINUTES "

Matthew Graham : "RTRS- FED: RECENT DETERIORATION IN JOBS OF PARTICULAR CONCERN BECAUSE LABOR MARKET UNCERTAINTY A KEY DRAG ON CONSUMER SPENDING "

Adam Quinones : "Far right thinning....WSJ - Rep. Ron Paul (R., Texas), a libertarian who wants to end the Federal Reserve, announced Tuesday he will not run for re-election to the House in 2012 and instead will focus on his presidential campaign.""

Adam Quinones : "16.5% award and 41% hit rate = above average award and aggressive bid"

Adam Quinones : "big story is uptick in aggression level from direct bidders."

Matthew Graham : "I don't know that I'm anticipating anything in particular, but it looks like a BTC over 3.0 and a small token of a "stop through" would be ideal. if we don't see both those things, could be challenging to rally this afternoon, but if we're somewhat close, it's just on to the next one + FOMC + econ data to get the bigger picture of the week."

Caroline Roy : "anticipating is the right word, we are all hoping"

Caroline Roy : "so you are hoping for a strong auction?"

Matthew Graham : "3.28 - 3.29 - 3.20 - 3.22 3.01"

Matthew Graham : "here are the last 5 bid-to-cover ratios starting with most recent"

Matthew Graham : "5 of last 6 have resulted in lower yields than when-issued trading"

Sam : "AQ or MG, how did the 3 yr auction perform last time?"

Jason York : "just an FYI, my UW jsut called to tell me that GMAC will go with what DU says on a DURP"

Matt Hodges : "over 50%, our bank requires 2 u/w signatures"

Matt Hodges : "as far as I remember from our conf call, ST caps at 45%, but I think WF will take AU"

Jason York : "anyone know if SunTrust or wells Fargo will allow the higher DTI's on DURP/"