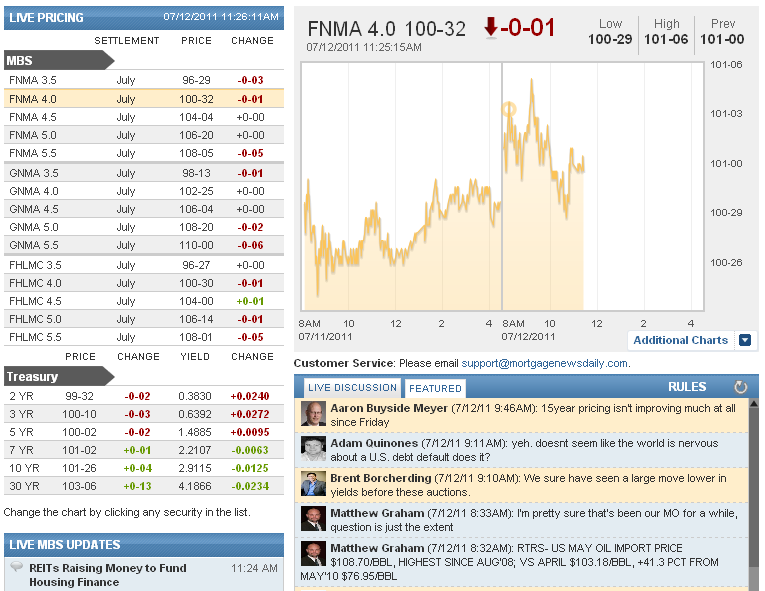

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:02 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:28AM :

ALERT:

MBS at Lows, Negative Reprice Risk Increasing

Not all lenders are out with rates yet, but those who are may be eyeing MBS at their lows of the morning and considering repricing for the worse. The range is still pretty narrow, and we still haven't broken convincingly into yesterday's range (yesterday's ceiling is still today's floor, in other words), but with Fannie 4.0's currently down to 100-31 after hitting 101-05 earlier this morning, the risks are potentially developing. If MBS bounce and stay in today's range, risks would be greatly decreased. Remember, we still have and auction and FOMC minutes today. (1pm and 2pm respectively)

9:25AM :

ALERT:

MBS Lagging TSYs Again. Loan Pricing Still Better

The last few days have provided a perfect example of why it can be dangerous to base your perspective of loan pricing on the movements of the benchmark 10-year Treasury note. If you;ve been pacing loan pricing based on the 10yr note's behavior, you're probably wondering where all your bps are going because they're not being passed along to rate sheets. What's going on? MBS have greatly lagged the interest rate rally that unfolded following a disappointing Employment Situation Report last Friday. Not to worry though, this tends to be the case whenever a "flight to safety" leads rates lower as MBS buyers are known to sit and wait until the market calms down before making any investment decisions (for quantitative reasons related to prepay speeds and the timeline of cash-flows). Case and point, the 10yr Treasury note is currently +12/32 while the Fannie Mae 4.0 MBS coupon is only +4/32. That 8/32 spread (25bps), which works out to a 5 tick lag after adjusting for different payoff assumptions, could lead one to believe loan pricing might improve by almost 40bps today. That won't be the case. At current indications, rate sheets are likely to improve by 10-20bps at best. That assumes all lenders lenders are pricing loans equally, which has not been the case recently. The primary mortgage market has been a roller coaster ride. All this volatility has worn out rate sheets and lender offers are all over the map!

8:53AM :

Rate Mover: Cisco to Cut Jobs to Revive Profit Growth

Although the ongoing EU debt crisis is the bond market's main motivator this morning, this news added some steam as well.... (Reuters) - Networking equipment company Cisco Systems Inc could eliminate as many as 10,000 jobs, or about 14 percent of its workforce, to revive profit growth, Bloomberg said, citing two people familiar with the matter. As many as 7,000 jobs would be eliminated by the end of August, the people told the agency. Cisco is also providing early-retirement packages to about 3,000 workers who took buyouts, according to Bloomberg.

8:48AM :

ECON: Trade Deficit Widest Since Oct 2008

The Trade Deficit in May rose to it's highest level since October 2008. Today's print was -$50.23 bln versus a consensus of $44 bln and a previous reading of $43.63 bln. Exports were down and imports were up with the latter at the highest level since July 2008 at $231.6 bln. Oil is a factor though. At $108.70 / barrel, imported oil prices were at their highest since August of 2008 and up 41.3 pct from one year ago.

8:46AM :

Rate Mover: Euro Leaders Open to Possible Greek Default

This is a big reason why rates are rallying this morning....(Reuters) - The euro zone acknowledged for the first time some form of Greek default may be needed to cut Athens' debts, but markets seized on the lack of a deadline for action and a lukewarm response from the IMF to heap pressure on Italy and Spain. Dutch Finance Minister Jan Kees de Jager said on Tuesday euro zone finance ministers had effectively accepted that if they wanted to have the private sector involved in a second bailout of Greece, a selective debt default was likely, despite the European Central Bank's vehement opposition to such a move. "We have managed to break the knot, a very difficult knot," he told reporters as he arrived for a second day of talks. Asked about whether a selective default was now likely, he replied: "It is not excluded any more. Obviously the European Central Bank has stated in the statement that it did stick to its position, but the 17 (euro zone) ministers did not exclude it any more so we have more options, a broader scope." Participants said both a buy-back of Greek debt on the secondary market and a German proposal for a bond swap for longer maturities were under consideration after a complex French plan to roll over bonds made no headway. Both would likely be regarded by ratings agencies as a default, or at best a selective default, which could have profound repercussions for financial markets. The lack of immediate action and the increased likelihood of some form of default sent European bank stocks and debt markets into a spin and propelled the euro sharply lower against the dollar. The cost of insuring against a default in Spain, Portugal and Greece hit a record high and 10-year bond yields in Italy, the euro zone's third-largest economy, shot above six percent for the first time since 1997, well above the level which bankers say will put heavy pressure on finances.

8:44AM :

Small Business Optimism Stuck in Recession Territory

NFIB’s monthly Small-Business Optimism Index dropped one tenth of a point (0.1) in June, settling at 90.8, an unsurprising reading, basically unchanged from the previous month and solidly in recession territory. While some indicators rose slightly – including expected capital outlays – pessimism about future business conditions and expected real sales gains tugged the Index down, causing a small but disappointing drop in the Index for the fourth consecutive month. Although June marked the second year anniversary of the recovery, it appeared there was little happening to make small business owners optimistic. “Small-business owners are registering a vote of ‘no confidence’ in the federal government,” said NFIB Chief Economist Bill Dunkelberg. “Between the deluge of new regulations and a Washington policy agenda that is largely ignorant of Main Street needs, stubbornly low consumer spending, and grave concern among small firms about the federal budget, there is not much to be optimistic about as a small-business owner. Who can blame the prevalence of pessimism when administration officials are telling Congress that small businesses need to pay more in taxes to support government spending programs?” Earnings trends for small businesses remained distressingly negative in June, particularly given that the recovery is now beginning its third year. The sales outlook for small firms continues to look grim as expectations have declined for 4 months in a row and “poor sales” continues to be the #1 problem for owners in operating their business. Inflation has slowed slightly, due in part to a leveling of gas prices. However, the fact that small firms are raising prices at all provides a glimmer of hope in an otherwise lackluster economic report. Access to credit remains a limited problem as it continues to affect a small percentage of owners.

8:22AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Aaron Buyside Meyer : "15year pricing isn't improving much at all since Friday"

Adam Quinones : "yeh. doesnt seem like the world is nervous about a U.S. debt default does it?"

Brent Borcherding : "We sure have seen a large move lower in yields before these auctions."

Matthew Graham : "I'm pretty sure that's been our MO for a while, question is just the extent"

Matthew Graham : "RTRS- US MAY OIL IMPORT PRICE $108.70/BBL, HIGHEST SINCE AUG'08; VS APRIL $103.18/BBL, +41.3 PCT FROM MAY'10 $76.95/BBL "

Scott Valins : "importing way more than we are exporting?"

Matthew Graham : "RTRS- US MAY TRADE DEFICIT WIDEST SINCE OCT 2008 ($59.5 BLN); IMPORTS HIGHEST SINCE JULY 2008 ($231.6 BLN)"

Matthew Graham : "RTRS - US MAY TRADE DEFICIT $50.23 BLN (CONSENSUS $44.00 BLN) VS APRIL DEFICIT $43.63 BLN (PREV $43.68 BLN) "

Matthew Graham : "widest trade deficit since 2008"

Adam Quinones : "Cisco could eliminate as many as 10,000 jobs: report: http://www.reuters.com/article/2011/07/12/us-cisco-jobs-idUSTRE76B0AV20110712"