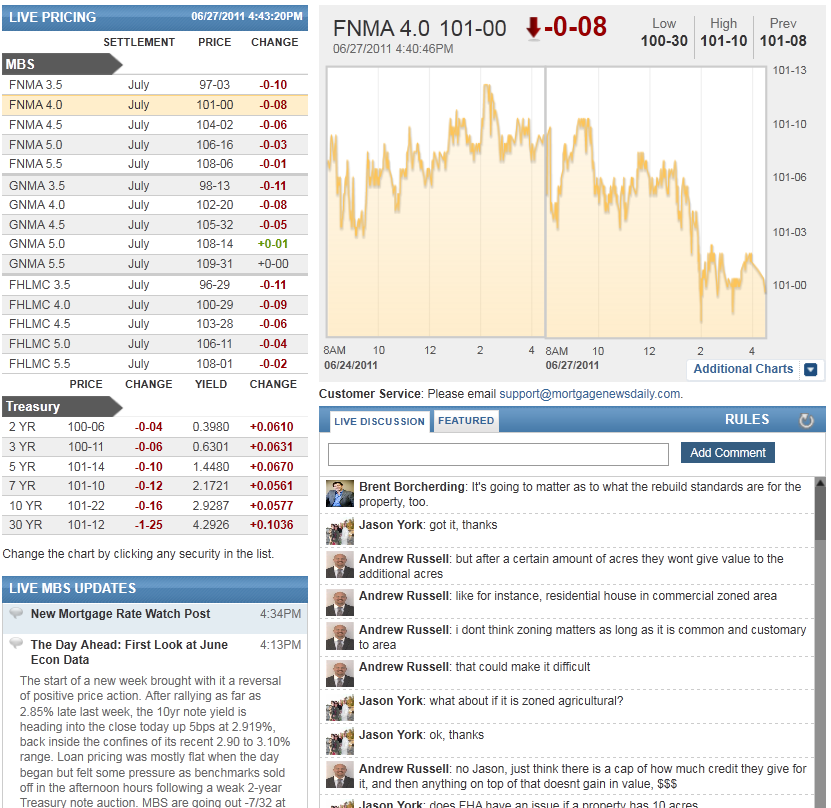

MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:00 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:29PM :

Large Firms Endanger Entire Financial System: Hoenig

(Reuters) - Financial firms that are so large that markets assume the government would prevent them from failing in a crisis are damaging to economic growth and the financial system, a top Federal Reserve official said on Monday. "The problem with SIFIs (systemically important financial institutions) is they are fundamentally inconsistent with capitalism," Kansas City Federal Reserve Bank President Thomas Hoenig said in remarks prepared for delivery to a conference on financial regulation.

Hoenig has persistently criticized firms that are viewed as meriting government protection after government bailouts during the recent financial crisis. Hoenig did not discuss the outlook for U.S. monetary policy in remarks on financial regulation.

3:18PM :

Lack of Conviction Displayed in Rally Reversal

On Friday, after 10s broke 2.90% resistance, our focus turned toward needing to see a confirmation of positive technical developments, hopefully in the following session, or today. Our skepticism was based on the idea that stocks had tanked on low volume and Treasuries were the main benefactor simply by default (no pun intended). A feeling of apprehension set in quickly as we concluded that rates had rallied with little to no push-back. The directional move seemed too easy, too good to be true. You might also recall that mortgages enjoyed none of those "flight to safety" benefits on Friday. Benchmark 10s improved by 0.375 in price, yet rate sheet influential MBS coupons ended the day flat. We felt l this reflected a lack of conviction in the bond market. There was a feeling of summer apathy in the air to say the least. So today we are not surprised to see profit taking and short selling lead benchmark 10s back in to the highly trafficked range we've occupied for all of June, between 2.90 and 3.10%. We're also not surprised to see MBS prices holding up better than their Treasury counterparts, not after the poor performance MBS gave on Friday when Treasuries were "rallying" and MBS buyers were no where to be found. That said, the corrective behavior being displayed by both stocks and bonds today leaves us back in a familiar situation. Stocks are once again treading water above important technical support levels and bonds are holding their breath near key technical resistance levels. Markets continue to await new guidance before exhibiting and confirming a new directional bias. What does this mean for rate sheets? It means lenders are more likely to price loan defensively until the market decides on a direction and sticks to it. Intraday volatility is not a friend to lock desks. The easiest way to deal with it is to simply add some margin to loan pricing. That way there's already a cushion baked into rate sheets when room is needed to absorb volatility.

1:48PM :

ALERT:

Negative Reprice Risk on the Rise After Auction

Although production MBS coupons have generally kept to a tight 6/32 price range all day, "rate sheet influential MBS" are now at their session lows and making a break even lower following the first Treasury auction of the week. While the reprice threat is not yet wide-spread, risks are rising. The Fannie Mae 4.0 is currently -6/32 at 101-02. This is 8/32 below the intraday price high of 101-10 and reprice territory for lenders who passed along modest pricing gains early this morning. If further MBS declines are seen, broader-based recalls for the worse are expected. We would target a breakdown of 101-00 price support in Fannie Mae 4.0s.

1:40PM :

Auction Recap: Dealers Digest Healthy Portion. Indirects MIA

Although production MBS coupons have generally kept to a tight 6/32 price range all day, the Fannie Mae 4.0 is currently at the low side of that range after the first Treasury auction of the week. Demand for $35bn 2s was relatively low on two accounts. First, the bid-to-cover ratio registered 3.08 bids submitted for every 1 accepted by Treasury. While complaining about a bid ratio over 3-to-1 is slightly spoiled, this metric is still well-below average (3.24-to-1). Then again recent averages have been greatly skewed by a few huge turnouts, specifically the 3.46 ratio seen in May, 3.47 in January and 3.70-to-1 last November. The second sign of sloppiness: 50.4% of the auction was sold at the high-yield of 0.395%. This is almost 1 basis point above the "When Issued" yield as bid in the open market, an indication that buyers lacked motivation in this offering and wanted to see cheaper prices. Of those buyers, primary dealers did the heavy lifting by adding $22bn in new 2-year note inventory or an above-average 65% of what they bid on. This implies primary dealers were interested buyers but only at higher yields. And based on the size of this auction's "tail" (high-yield vs. WI), it looks like they got what they wanted and maybe a bit more. Indirects on the other hand added only $7.7bn in new 2s or a way below average 22% of the issue. Directs were pretty average participants at 15% of the competitive award and 28% of what they bid on. The story here seems to be a large tender by dealers who wanted inventory but only at a cheaper price but likely got more than they bargained. AND...indirect bidders who only tendered a measly $11bn (previous 2yr note auction tenders: $17bn, $21bn, $16.5bn, $19bn, $22bn). It's like indirects wanted nothing to do with this debt. Short-term inflation worries? I guess the million dollar questions are: How much more inventory did dealers get than they wanted? Are indirects bidders trying to tell us something?

12:36PM :

New Capital Rules: Good or Bad for Home Lending?

A few comments on this next story from Reuters. Higher capital requirements are good and bad. When added to mortgage industry risk retention regs, these additional capital requirements could slow reform in the secondary mortgage market as larger banks shy away from new lending risks (they would rather lend to the government). That would force the GSEs and FHA to carry on their heavy involvement in the housing finance mechanism and reduce competition in the primary mortgage market. Not a political favorite! But, if home prices have not bottomed and another wave of strategic defaults rolls through the housing market, these extra reserves would be needed. So perhaps regulators are just preparing the biggest banks for the worse case scenario. Either way, without new financial innovations we see these additional reserve requirements as hindering the money creation process. The mortgage industry is now reliant on REITS for housing finance innovation....(Reuters) - Global banking regulators have agreed on a proposal to slap an extra capital charge on the world's biggest banks to make them safer by 2019. The surcharge is part of a series of regulatory reforms launched in response to the financial crisis, which forced countries worldwide into costly bailouts of their banking sectors to prevent systemic collapses. The Group of Governors and Heads of Supervision (GHOS) said after a meeting in Basel on Saturday the proposal would be put out to public consultation next month. "The additional loss absorbency requirements are to be met with progressive common equity tier 1 capital requirement ranging from 1 percent to 2.5 percent, depending on a bank's systemic importance," the group said in a statement. The capital surcharge will come on top of the new 7 percent minimum core capital all banks across the world will have to hold under new Basel III rules being phased in over six years from 2013.

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Jeff Anderson : "Hello from sunny FLA everyone. I totally agree with JR's comment. Just had 3 firms in our area merge. They were probably 15-25 LO's in size per shop. The small firms are having issues with all the reserve/asset requirements."

Adam Quinones : "I would say the busiest times were the overnight session and right before the Fed's QEII open market operation at 11am. Modest jump around auction time too but otherwise slow U.S. session."

Adam Quinones : "not terribly low but below average activity in TSY futures. 1.17mln vs. 1.32 10-session average."

Adam Quinones : "low volume day in MBS "

Rob Clark : "citi price change"

Curt Sandfort : "WF in middle of a reprice"

John Rodgers : "http://www.archives.gov/veterans/military-service-records/"

BVG : "hey Yorkie--- is there a site where I can order a dd214 without the wait?"

Jason York : "Chase USDA just repriced"

Adam Quinones : "now +1.11% at 1278"

Adam Quinones : "S&P futures taking back some of Friday's "summery weakness""

Rob Clark : "pf 1/8 worse"

Tony Cardinal : "they will only do it if it's owned by WF, currently"

Tony Cardinal : "WF, Lion. Freddie to Freddie SL, no appraisal, stated income...question is...Is it WF owned currently?"

Lion : "High Balance, Freddie Refi Relief, Open Access, No Income, No Asset - Any good sources to recommend? "

Adam Quinones : "agreed. very summery today...."

Andrew Horowitz : "a summer auction"

Andrew Horowitz : "yeah pretty sloppy"

Adam Quinones : "Low bid to cover. Very low non-dealer bid. Indirects MIA here."

Adam Quinones : "I give it a D."

Adam Quinones : "RTRS - - PRIMARY DEALERS TAKE $22.47 BLN OF 2-YEAR NOTES SALE, INDIRECT $7.67 BLN "

Adam Quinones : "RTRS - U.S. 2-YEAR NOTES BID-TO-COVER RATIO 3.08, NON-COMP BIDS $148.85 MLN "

Adam Quinones : "RTRS U.S. SELLS $35 BLN 2-YEAR NOTES AT HIGH YIELD 0.395 PCT, AWARDS 50.43 PCT OF BIDS AT HIGH "

Adam Quinones : "RTRS - - KOCHERLAKOTA-MONETARY POLICY SHOULD BE DRIVEN MORE BY CORE INFLATION OUTLOOK THAN BY ESTIMATES OF NATURAL UNEMPLOYMENT RATE "

Adam Quinones : "The same conditions of instability that produced the post-war system of repression are again at work. Banks’ reserve requirements are rising in the wake of the financial crisis. Regulators like Britain’s Financial Services Authority are mandating that banks boost their holdings of safer government bonds for liquidity reasons. The new Basel 3 rules on bank capital still privilege government debt over other assets, nudging holdings toward sovereign debt despite the possibility of below-market retu"

Adam Quinones : "THE MYSTERY = Investors scared to make long-term allocation decisions bc of increased levels of uncertainty. "

Adam Quinones : ""Between 1945 and 1980 negative real interest rates ate away at government debt. Savers deposited money in banks which lent to governments at interest rates below the level of inflation. The government then repaid savers with money that bought less than the amount originally lent. Savers took a real, inflation-adjusted loss, which corresponded to an improvement in the government’s balance-sheet. The mystery is why savers accepted crummy returns over long periods.""

Adam Quinones : "READ MORE ABOUT REPRESSION: http://www.economist.com/node/18834259?story_id=18834259"

Adam Quinones : "it's called repression Brent. A very common way to keep debt levels from skyrocketing. Negative real interest rates eat at debt principal."

Brent Borcherding : ""If you're going to force us to put our money to work in this environment...it's going into the safest thing possible." Got it & let's hope that it works."

Adam Quinones : "....not including the generally risk averse attitude Brent"

Adam Quinones : "GN's more than FN's"

Adam Quinones : "i have said our outlook supports lower rates. in relation to QEII the major reason to buy TSYs has been a factor of bank capital requirement reforms. Cash needs to be put to work in a liquid asset. TSYs and MBS should benefit from that..."

Adam Quinones : "after months of short covering (position squaring), I think we're safe to say stored energy is building and ready to explode."

Brent Borcherding : "AQ--Haven't you written that you expect TBTF banks to be buying TSY as the Fed leaves? "

Adam Quinones : "From that perspective...I dont know how this week's auctions are gonna go. The 2nd quarter is coming to an end and so is QEII. The directional bias is very up in the air and TSYs look overbought. All reasons that could lead to below-average demand metrics. But when it comes down to it ... a general feeling of risk aversion is prevalent. That in and of itself is enough justification to buy TSYs. Fear of the unknown..."

Adam Quinones : "...convexity buying has been mostly mute."

Adam Quinones : "short covering has really played a big role in the rates rally. we still have yet to see a major bullish shift in the market's profile (positional sentiment)"

Adam Quinones : "everyone waiting for someone else to make the first move."

Adam Quinones : "that is basically what's happening in the bond market right now. "

Brent Borcherding : "Love it...very visual"

Jason Wilborn : "and usually the first wildebeest takes it for the squad"

Adam Quinones : "and all the others follow."

Adam Quinones : "there is a moment of stillness then all of sudden out of nowhere one wildebeest makes a run for it."