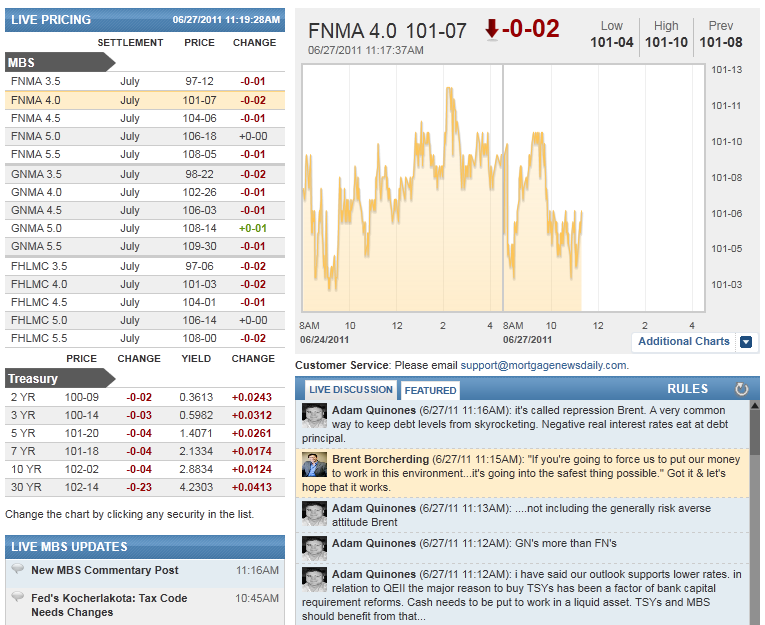

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:00 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:45AM :

Fed's Kocherlakota: Tax Code Needs Changes

(Reuters) - U.S. lawmakers should change the tax code to discourage household and business borrowing that threatens the stability of the financial system, a top Federal Reserve official said on Monday.

The current U.S. tax code allows households to deduct interest payments on home mortgages and corporations to deduct interest payments on debt.

Both policies subsidize leverage, encouraging the kind of excessive borrowing that helped trigger the recent financial crisis, Minneapolis Fed President Narayana Kocherlakota said in remarks prepared for delivery to the Tri-State Bankers Summit in Big Sky, Montana.

High leverage leaves households and businesses vulnerable to shocks, he said. Indeed, the sudden drop in land prices may not have set off the recent financial crisis had households and business not been weighed down with so much debt, he said.

"The mortgage interest tax deduction undercuts financial stability," Kocherlakota said. "The tax code includes what is known as a corporate debt tax shield that encourages higher leverage for financial institutions."

Policymakers should therefore limit the degree to which households and businesses can deduct interest payments from their taxable incomes, he said.

They could still use tax incentives to promote home ownership, but instead of mortgage interest payment deductions, they could use tax credits on downpayments, he said. Such a policy would help out homebuyers without subsidizing their mortgage debt.

Likewise, policymakers could cut the corporate tax rate to encourage business investment, he said.

Last year's Wall Street overhaul legislation gave the Fed new supervisory powers over large banks that are meant to allow it to spot and defuse any build-up of risk in the financial system.

Policymakers should use tax policy to support those efforts, Kocherlakota said.

(Reporting by Ann Saphir; Editing by Padraic Cassidy)

10:32AM :

ALERT:

Directional Alert: MBS Back Down. Stocks Surge.

This is one of those alerts that isn't necessarily a warning about reprices for the worse. Reason being: current MBS levels are, for the most part, priced into any rate sheets that are out already this morning, and will be priced in to sheets that aren't out yet. After getting as high as 101-10, Fannie Mae 4.0 Coupons have fallen fairly quickly to 101-06. Over the same time, the S&P Index, opened in the mid 1268's and just now crested 1278. So while it is an outside possibility that rate sheets from 9:15 to 9:45am might be at a slight risk of repricing for the worse, this is first and foremost simply an alert to let you know about what HAD BEEN a sharp directional move higher turning into a sharp directional move lower. That being said, both Treasury Yields and MBS Prices are still INSIDE the extremes of their trading ranges from Friday. Volatility within a range.

9:06AM :

Fed Seen Purchasing $300bn in Treasuries After QEII

(Bloomberg) -- The Federal Reserve will remain the biggest buyer of Treasuries, even after the second round of quantitative easing ends this week, as the central bank uses its $2.86 trillion balance sheet to keep interest rates low. While the $600 billion purchase program, known as QE2, winds down, the Fed said June 22 that it will continue to buy Treasuries with proceeds from the maturing debt it currently owns. That could mean purchases of as much as $300 billion of government debt over the next 12 months without adding money to the financial system. “I don’t think the Fed wants to remove accommodation in any way, shape or form,” said Matt Toms, the head of U.S. public fixed-income investments at Atlanta-based ING Investment Management, which oversees more than $500 billion. “It’s quite natural for them to reinvest cash,” he said. “That effectively maintains the accommodative stance.” A total of $112.1 billion of the Fed’s government bond holdings will mature in the next 12 months, 7 percent of the $1.59 trillion in Treasuries held in its system open market account, known to traders as SOMA. Replacing those securities will require the Fed to buy an average of $9.4 billion of Treasuries a month through June 2012. The Fed also held $914.4 billion of mortgage-backed debt and $118.4 billion of debentures, the debt of government sponsored enterprises Fannie Mae and Freddie Mac, as of June 22. UBS AG, Citigroup Inc., Bank of America Corp., JPMorgan Chase & Co. and Royal Bank of Canada say $10 billion to $16 billion will mature each month, depending on the pace of prepayments

8:51AM :

MBS Maintain Friday Range Before and After Econ Data

Fannie Mae 4.0 Coupons are down only 1/32nds from Friday's close. Earlier this morning, they'd been as low as 101-03, matching Friday morning's lowest levels. These gains leave prices in the middle of the their trading range over the last two sessions. 10yr Treasuries are improved after the data as well with yields nearly unchanged at 2.87. S&P futures only fell about 2 points on this AM's data. The theme that seems to be pervading all the morning's trading is that markets are still in need of guidance and motivation. This morning's market movements are lacking a certain amount of conviction that might otherwise speak to impending directionality heading into this afternoon's 2yr Note Auction.

8:34AM :

ECON: Consumer Spending Flat in May

(Reuters) - U.S. consumer spending was unchanged in May for the first time in almost a year, likely reflecting a plunge in auto sales, according to a government report on Monday, that also showed a build-up in underlying inflation pressures. The flat reading in consumer spending came after 10 straight months of gains, the Commerce Department said, and followed a downwardly revised 0.3 percent gain in April. Economists polled by Reuters had expected spending, which accounts for about 70 percent of U.S. economic activity, to gain only 0.1 percent last month after a previously reported 0.4 percent rise in April. When adjusted for inflation, spending fell 0.1 percent in May, declining for a second straight month. Spending on durable goods fell 1.5 percent after being flat in April. Spending last month was probably held back by a sharp drop in motor vehicle purchases as disruptions to auto production due to a shortage of parts in the aftermath of Japan's March earthquake and tsunami left some models out of stock. May's weak reading suggests that consumer spending, which has been hampered by high gasoline prices, in the second quarter will be much slower than the 2.2 percent annual rate recorded in the first three months of the year. While the report fits in with other data illustrating the loss of momentum in the economy, falling gasoline prices should lift spending and therefore growth in the third quarter. (Reporting by Lucia Mutikani, Editing by Andrea Ricci)

7:48AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "Interesting read. I tend to agree, but would prefer not to address this in the midst of an already shaky time for purchase demand."

Matthew Graham : "" They could still use tax incentives to promote home ownership, but instead of mortgage interest payment deductions, they could use tax credits on downpayments, he said. Such a policy would help out homebuyers without subsidizing their mortgage debt.""

Adam Quinones : "RTRS - KOCHERLAKOTA-POLICYMAKERS SHOULD USE TAX INCENTIVES FOR HOME OWNERSHIP, BUSINESS INVESTMENT THAT DON'T ENCOURAGE DEBT "

Brent Borcherding : "That's not really an underwriting guideline though, right? I mean, I'm an originator too, but what your idea is I'd like the easiest, refinance...outside of VA Streamline, comeback..."

Christopher Stevens : "mi idea Brent is to let people with an FHA mortgage streamline refinance using their current mi rate as opposed to the new rates. This would help people save money. the new mi rates are keeping people from refinancing because the drop in rate is not enough to cover the increase in MI"

Brent Borcherding : "Just curious, what do you think could/should be loosened up in underwriting?"

Christopher Stevens : "Most people who already refinanced rolled in closing costs at these low rates and are probably close to being maxed on equity availability to roll in closing costs again."

Chris Kopec : "CS....I agree somewhat. The well-qualified will benefit, and the ones that could benefit the most will remain on the sidelines."

Christopher Stevens : "There will be no refi boom if u/w standards are not loosened a bit. "

Adam Quinones : "will be based on MBS prepays Chris. If we see a mini-refi boom it could happen...but $300bn seems a bit excessive."

Christopher Stevens : "interesting article... http://blogs.wsj.com/marketbeat/2011/06/27/treasury-yields-still-tumbling-with-help-from-stealth-qe3/"

Adam Quinones : "the hard asset is much more illiquid."

Adam Quinones : "haha. what about all the real estate they own????"

Matthew Graham : "I'm gonna be really surprised if any of the big 5 are heavy enough into RMBS to prompt a future bailout in the current environment"

Adam Quinones : "the lag in the non-agency market reflects falling home prices and the potential for more strategic defaults."

Adam Quinones : "We've done nothing but tick wider since April AH. Besides servicers, convexity buyers have been very quiet,. MBS have lagged..."

Andrew Horowitz : "the pounding in those markets occured from April until now, my point is that during that time period the FNMA/FHLMC/GNMA complex has rallied think there is some correlation with the collapse of the cmbs and subprime gambles "

Adam Quinones : ""Risk Off": MBS Buyers Missing in Action: http://www.mortgagenewsdaily.com/mortgage_rates/blog/216210.aspx"

Adam Quinones : "we're at YTD wides and buyers have been MIA for the most part since the start of June. TBAs have largely played follow the leader with TSYs"

Adam Quinones : "Andy I dont see the "flight to safety" into MBS"

Andrew Horowitz : "Bonds backed by subprime home loans in states such as California and Florida fell by 23% from April to June, according to pricing data from Amherst Securities. The ABX, an index that tracks the value of bonds backed by subprime home loans, tumbled 21%, to about 46 cents on the dollar, from 59 cents, according to data from Markit."

Andrew Horowitz : "here is the article MG http://online.wsj.com/article/SB10001424052702303627104576410024021474448.html?mod=googlenews_wsj"

Andrew Horowitz : "this may also explain the run into our MBS market, exiting the risk and buying the safety"

Andrew Horowitz : "here you go back on topic from the journal this weekend The rush by banks to dump risky assets and avoid losses now appears to have exacerbated turmoil in the credit markets in May and June. Bonds backed by subprime home loans and commercial real-estate debt plunged 20% to 25% in a span of a few weeks, erasing a whole year's worth of price gains."

Adam Quinones : "the recent decline in oil prices, if sustained, will be helpful though."

Adam Quinones : "different spending choices = few units purchased or less volume spent."

Adam Quinones : "that number seems scary but with no wage growth consumers have no additional purchasing power. that implies consumers will either have to eat at savings (not in May!), rely on credit, or simply make different spending choices..."

Adam Quinones : "RTRS - US MAY CORE PCE PRICE INDEX RISE LARGEST SINCE OCT 2009 (+0.3 PCT) "

Matthew Graham : "RTRS US MAY CORE PCE PRICE INDEX RISE LARGEST SINCE OCT 2009 (+0.3 PCT)"

Matthew Graham : "RTRS US MAY YEAR-OVER-YEAR PCE PRICE INDEX RISE LARGEST SINCE JAN 2010 (+2.5 PCT) "

Matthew Graham : "RTRS US MAY PERSONAL SPENDING WEAKEST SINCE JUNE 2010 "

Matthew Graham : "RTRS US MAY MKT-BASED YEAR-OVER-YEAR PCE PRICE INDEX +2.7 PCT, CORE +1.3 PCT "

Matthew Graham : "RTRS US MAY MKT-BASED PCE PRICE INDEX +0.2 PCT (APRIL +0.4 PCT), CORE +0.3 PCT (APRIL +0.2 PCT) "

Matthew Graham : "vRTRS US MAY PERSONAL SAVING RATE 5.0 PCT VS APRIL 4.9 PCT "

Matthew Graham : "RTRS US MAY REAL CONSUMER SPENDING -0.1 PCT VS APRIL -0.1 PCT (PREV +0.1 PCT) "

Matthew Graham : "RTRS US MAY YEAR-OVER-YEAR PCE PRICE INDEX +2.5 PCT VS APRIL +2.2 PCT (PREV +2.2 PCT); CORE +1.2 PCT VS MARCH +1.1 PCT (PREV +1.0 PCT) "

Matthew Graham : "RTRS US MAY OVERALL PCE PRICE INDEX +0.2 PCT (+0.1709) VS APRIL +0.3 PCT (PREV +0.3 PCT) "

Matthew Graham : "RTRS US MAY CORE PCE PRICE INDEX +0.3 PCT (+0.2571; CONS +0.2 PCT) VS APRIL +0.2 PCT (PREV +0.2 PCT) "

Matthew Graham : "RTRS- US MAY PERSONAL SPENDING 0.0 PCT (CONSENSUS +0.1 PCT) VS APRIL +0.3 PCT (PREV +0.4 PCT) "

Matthew Graham : "here's PCE...."