The week begins at a brisk pace with Personal Income and Spending right off the bat at 8:30AM on Monday morning. Soon after that we'll be preparing for the week's Treasury auction cycle, starting early this time with $35bn 2s at 1pm. 5’s and 7’s arrive in a similarly early fashion on Tuesday and Wednesday. Adding a few layers of complexity to that situation will be a diverse line-up of Fed Speakers not to mention the ongoing potential for tapebomb news headlines.

"Greece remains the focal point for markets, with a three-day debate on the austerity measures beginning today," said economists at BMO Capital Markets. "A vote on the measures is expected on Wednesday, and a vote on an enabling law to ensure the package can be quickly implemented is expected Thursday."

While the Treasury auction cycle and continued developments in Greece will certainly be market moving, there’s an interesting twist to the calendar of events ahead.... Thursday is the last day of the month, the quarter, the half, and of QE2.

After spending seven months buying bonds from the Treasury and selling them to the Fed, many questions remain unanswered as to how market participants will change their views and strategies surrounding the Treasury market once the latest round of Quantitative Easing program is completed. While the Fed told us last week that it intends to reinvest maturing debt back into U.S. Treasuries, which could lead to another $300 billion in asset purchases over the next 12 months, the exit of the market's biggest buyer adds uncertainty to already volatile trading environment. Illustrating that, investors haven't been displaying much directional commitment to bonds lately. So with 10s going out near new YTD yield lows last Friday, traders will looking for a confirmation rally early and often this week.

Treasuries are slightly stronger and equity futures are turned modestly upwards as the week begins. The benchmark 10-year Treasury begins the week yielding 2.87%, while the two-year yield is 0.35% and the 30-year yield is 4.21%. The S&P 500 is poised to open 1 point higher at 1,265and the Dow appears ready to jump 24 points at the open to 11,905. The Fannie Mae 4.0 MBS coupon is unchanged at 101-08.

Overnight news included a word from French finance minister Christine Lagarde; she said the government has drafted a deal to incentivize French banks to roll over their holdings of Greek government debt.

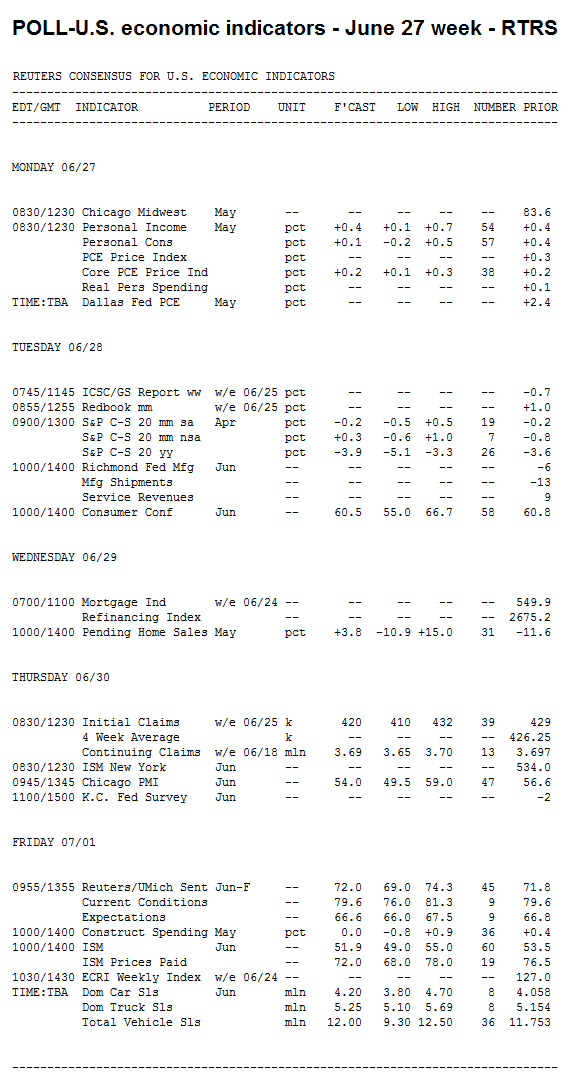

Key Events This Week:

Monday:

8:30 - Be prepared for a weak Personal Income & Outlays report for May. While income is expected to rise 0.4% for the second month, consumer spending is anticipated to be flat after rising 0.4% in April. Some economists even anticipate a 0.2% cutback in spending, given that private employment only grew by 83k in the month - the lowest in 11 months.

"The various stages of the temporary shocks from the disaster in Japan and the rise in energy prices should be on full display in the personal consumption and income report," said economists at Citigroup.

"Consumer spending was hit hard in May by the drop in motor vehicle purchases, due to a severe lack of inventory on dealer lots," they added. "With vehicle assemblies ramping up in June, there is a strong likelihood that sales will rebound later in the summer. Meanwhile, the substantial gains in wage and salary income have been eaten up by the run-up in gasoline prices. Through April, there has been no real disposable income growth at all this year."

Core PCE inflation - the Federal Reserve's preferred measure - is forecast to again rise 0.2% that would increase the year-on-year inflation rate to 1.2%.

"Spiraling inflation is currently not one of our fears, given the considerable slack that exists in the labor market and the sluggish level of wage growth," said economists at IHS Global Insight. They added that inflation expectations in the University of Michigan survey "have begun to decline due to falling gasoline prices."

11:00 - Narayana Kocherlakota, president of the Minneapolis Fed, speaks on leverage subsidies to the Tri-State Bankers Summit in Big Sky, Montana.

1:00 - Thomas Hoenig, president of the Kansas Fed, speaks on systemically-important financial institutions to a conference on the Dodd-Frank reform in Washington.

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

1:00 - 2-Year Notes

Tuesday:

9:00 - Home prices unexpectedly rose 0.8% in April's FHFA home price index last week. That gives a little upside risk for the S&P Case-Shiller Home Price Index, a more closely-watched index of 20 metropolitan areas. The last index, for the first quarter, was far from optimistic: prices fell 4.2% in the quarter, with the national median dropping to its lowest since mid-2002. Year-on-year, the 20-city index was down 3.6%.

According to Nomura Global Economics, prices continued to fall in April. They predict a year-on-year decline of 3.9%.

"Taking into account variations in other home price indices over the February-April period, which have already been reported by private research firms such as Zillow.com and Core Logic, the year-over-year change rate of the index likely decreased further in April," they said.

10:00 - No need to mince words here: Consumer Confidence has no reason to have increased in the past month. Since the index fell 5.2 points to 61 in May, "the consumer mood has become more pessimistic due to poor payroll numbers, a further decline in home prices, increasing non-energy prices, and an unsettling stock market."

That's according to IHS Global Insight. But in fact: it's a minority view. The consensus anticipates a one-point gain to 62. The reasons are ... not clear.

As forecasters at Janney put it: "Consumers got whacked hard by the ugly stick in March, as the concurrence of war in Libya, rising energy costs, and a nuclear disaster delivered bad news troika-style. After an immediate blow to confidence eased somewhat, the trickle of mixed economic data turned into a faucet of negativity, culminating in May's deeply disappointing payrolls report."

Treasury Auctions:

11:30 - 4-Week Bills

11:30 - 52-Week Bills

1:00 - 5-Year Notes

Wednesday:

10:00 - The Pending Home Sales Index declined a whopping 11.6% in April, marking the third fall in five months and leaving the index at its lowest in seven months. The consensus estimate looks for a 1% decline in May, but according to High Frequency Economics, a spokesman at the National Association of Realtors said pending sales were up 15% in May.

"The NAR complies the numbers, so it should know," HFE added. "An increase of that size would more than reverse April's 11.6% drop."

12:00 - Fed Governor Sarah Bloom Raskin speaks on rebuilding road to financial stability at the New American Foundation in Washington.

Treasury Auctions:

1:00 - 7-Year Notes

Thursday:

8:30 - Last week's Initial Jobless Claims report didn't bode well for the June payrolls figure, which is compiled based on data from that period. Weekly claims rose 9,000 to 429,000, with the four-week average at 426,250. In the survey week for May's disappointing payrolls report, the four-week average was 440,250. This week's survey is anticipated at 420,000 - it would mark the 12th week above the 400k level.

"A return to the sub-400k March readings seems unlikely in the near-term," said economists at Nomura. "In fact, early retooling (in June rather than July) in the auto manufacturing sector may temporarily boost claims in the weeks ahead."

9:00 - James Bullard, president of the St. Louis Fed, briefs reporters following a conference on quantitative easing in St. Louis.

9:45 - No rebound is expected in the Chicago Business Barometer for June. The index of manufacturing and services decline 11 points in May to 56.6, a score that indicates healthy expansion, but not a robust pace. With the new orders index sharply lower in that survey, and weakness evident in the regional manufacturing surveys, expectations are for another drop in June. The consensus is calling for a 53.

"The deep dives in the Philly Fed and Empire State business indexes signaled that manufacturing activity is slowing abruptly," said economists at Citigroup. "Chicago area activity had been much stronger than other regions and the nation as a whole, but the slowdown is affecting even that high-flying area. In addition, supply-chain issues stemming from the disaster in Japan probably have hurt motor vehicle and parts production."

Friday:

9:55 - Consumer Sentiment fell 2.5 points in mid-June to 71.8. A weak jobs market coupled with further declines in the stock market were largely to blame, and both continue to weigh on consumers. The consensus looks for no change.

"Since that time, there has been no good news to which households can point that would have lifted confidence," said economists at Nomura. "We don't expect the late-June figure to move much."

Economists at Citigroup, however, predict that falling gasoline prices should buoy sentiment; on the other hand, they mention rising jobless claims and volatile equities.

10:00 - Growth in the ISM Manufacturing Index has been slowing down since peaking in February at a robust 61.4. The May index declined 6.9 points to 53.5, with the new orders component tumbling almost 11 points to 51. Further slowdown is expected in June: the consensus is predicting a score of 52. None of the economists surveyed predict a contraction, but if they are wrong it would break a 22-month trend of growth.

Economists at Janney Capital Markets explain why the index is so closely-watched by financial markets: "Manufacturing industry performance represents the most classic of leading indicators for overall domestic activity. Although factory output accounts for an estimated 15% of total production, it tends to be more volatile and quicker to react to changes in demand than the larger services sector output. As a result, the slowdown in manufacturing, perhaps best exemplified by declines in the ISM, is troubling for second half economic growth."

"A key item to watch," added economists at IHS Global Insight, "will be export orders, as future growth in manufacturing requires a solid export market when domestic demand is anemic. Export readings have bounced between a solid 55 and a robust 62 in the past 18 months and were at the low end of that range in May; they must thrive, or manufacturing shrivels."

10:00 - Construction Spending rose 0.4% in April, yet compared to 12 months prior it was down 9.3%. Pulling the index down recently has been public construction; it fell 1.9% in April, marking the eighth month of decline, whereas private spending climbed 1.7%. The May index is anticipated to fall 0.3% overall, though forecasts range widely from -0.8% to +0.2%.

"We look for a decline in May construction spending, led by a continued fall in public projects and a downswing in residential expenditures," said economists at Citigroup. "The long decline in residential construction seems to have run its course. Based on housing starts and building permits data, new construction has been relatively flat since the recession ended. But the residential construction spending numbers have been extremely volatile, reflecting big swings in additions and alterations."