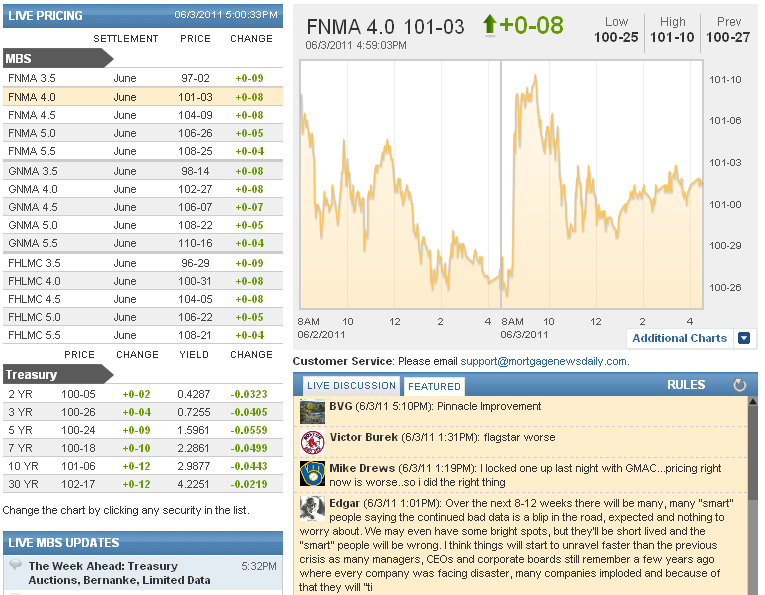

MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:00 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:25PM :

Reprice Risks Subside as Stocks Fall and MBS Rise

After the 3pm official bond market close, 10yr yields are down just over 1bp and MBS have gained 2 ticks. That puts FNCL 4.5's up 7 ticks on the day at 104-08 and 4.0's up 8 ticks on the day at 101-03. Previous losses had prompted several lenders to reprice for the worse, but these late-day gains are mitigating that risk. And while there's not a good chance of reprices for the better yet, this helps solidify some of the ground gained in MBS today. 10yr yields are at 2.988.

1:20PM :

Why Do Banks Hate Elizabeth Warren?

(Reuters) - Elizabeth Warren, it’s not you they hate. It’s what you represent. You want to be an honest cop when so many before you in Washington have looked the other way and pretended that the banking industry could police itself. She knows where the bodies are buried — in countless toxic forms and statements that only bank lawyers fully understand. She’ll make every attempt to end the silent rip-offs and myriad shenanigans that cost consumers billions. As the debate about Warren — and what she stands for — rages on, here’s a look at why the banks despise the idea of her as a strong regulator... Reason #1 Weak consumer regulation was the norm, but banks love the status quo. The CFPB will be the first regulator in American history that didn’t answer to the banks, but to their customers. It will be a true watchdog. Reason #2: Mortgage abuses were rampant. A consumer financial bureau would keep an eye on an industry that’s operated in darkness for too long. Reason# 3: Credit abuses are rampant. Banks have conceived elaborate formulas for charging you more money for credit. A consumer bureau might be able to rein in these practices. Reason #4: Credit Forms are Confusing. Why can’t credit forms spell costs out in plain language? Why can’t they tell you what your payment should be including taxes, insurance and other fees? The CFPB already is working to simplify this morass of incomprehensible forms and even wants your opinion on new proposed versions. So nothing personal Elizabeth Warren. It’s not the way you dress or the fact that you teach at Harvard and have been an advocate for banking customers. Or that you’re “so bloody disagreeable,” as one former Wall Street banker put it. It’s just that you’re so darned honest about banking abuses and are one of the best people in the country to enact change.

1:05PM :

ALERT:

Reprices Reported. More Recalls Possible

Reprices for the worse have been reported today. If your lender has not recalled and repriced for the worse already you are still at risk of that happening. More so now than ever because mortgages and benchmark Treasuries are retesting their worst prices of the day as investors have pushed stocks back to their pre-jobs data levels (1308 in S&P).

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Victor Burek : "flagstar worse"

Mike Drews : "I locked one up last night with GMAC...pricing right now is worse..so i did the right thing"

Edgar : "Over the next 8-12 weeks there will be many, many "smart" people saying the continued bad data is a blip in the road, expected and nothing to worry about. We may even have some bright spots, but they'll be short lived and the "smart" people will be wrong. I think things will start to unravel faster than the previous crisis as many managers, CEOs and corporate boards still remember a few years ago where every company was facing disaster, many companies imploded and because of that they will "ti"

Kent Mikkola #353976 : "http://www.hud.gov/offices/adm/hudclips/letters/mortgagee/files/11-10ml.pdf"

Jason York : "anyone have an FHA MI chart then can send me?"

Dean Gorenflo : "Full list of declared disasters with from and to dates"

Dean Gorenflo : "Lynn...check this link: http://www.fema.gov/news/disasters.fema?year=2011"

Lynn ONeal : "anyone familiar with how to determine an expiration date on a FEMA declared disaster?"

Dirk Postupack : "5/3rd repricing for the worse"

Jeff Anderson : "GMAC reprice for the worse. Settle down boys. Or are they just slowing the pipe on a Friday?"

Chris Kopec : "This week changed the narrative. We've gone from inflation, to soft patch, to questioning a double dip."

Victor Burek : "my bank just repriced worse"

Jill Statz : "ST for the reprice for the worse"

Jason Sheaffer : "I love this site because wells wholesale always reprices about 15 minutes before wells retail reprices so I can always lock up my deals before our reprice hits!"

Matt Hodges : "my concern is the new line of work, JY. How secure will an u/w feel about it?"

Terry Colabrese : "WF and a local regional bank have repriced for the worse already, in my region. That was pretty quick, I think!"

Jason York : "i meant to ask, now with that new nugget of information, can I still use his income?"

Jason York : "i don't know if anyone remembers my line of questioning the other day about my customer that was self-employed, and is now in a new line of work for about a month, but I just got his tax returns, and he didn't have any income the past 2 years, when I called him to ask him to send over his business returns, he said that his business fell off a cliff in Sept 2008, and he didn't make any money in the business in 2009 or 2010, which is why he is now in the new line of work"

Matthew Graham : "Yes, massive spike after data, but still very high relative to other days of the month. bulging and subsiding into this little selling spree"

Jeff Anderson : "How's volume? Spike after the data and cooling down now?"