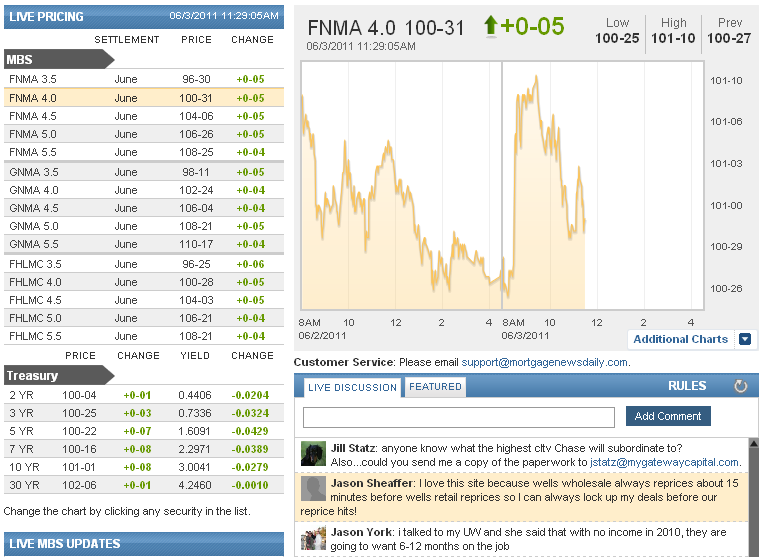

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:02 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:36AM :

ALERT:

Reprices and Delays Possible as MBS Shed Gains

In our last live MBS update we informed dashboard participants that "mortgages are coming off their best levels of the day as stocks attempt to rally from their lows" and "we will alert if stocks continue to rally and MBS shed more price gains." Well, stocks have extended their recovery effort (on short covering) and production MBS coupons are now 10/32 off morning price highs. This will lead some lock desks to recall rate sheets and reissue for the worse while others will simply delay their initial release until the market finds stable ground. Either way loan pricing appreciations will not be as robust as originally expected today. MBS are however still in positive territory so rebate should not be worse than yesterday's indications.

10:25AM :

ECON: U.S. service sector growth picks up in May-ISM

(Reuters) - The pace of growth in the U.S. services sector picked up modestly in May after a sharp drop in the previous month, according to an industry report released on Friday.

The Institute for Supply Management said its services sector index rose to 54.6 last month from 52.8 in April. The reading came in just above economists' forecasts for 54.0, according to a Reuters survey. The bounce came after April's reading fell to the lowest level since August 2010.

A reading above 50 indicates expansion in the sector. (Reporting by Leah Schnurr, Editing by Chizu Nomiyama)

10:23AM :

MBS Off Best Levels as Stocks Scratch for Life

Mortgages are coming off their best levels of the day as stocks attempt to rally from their lows. The Fannie Mae 4.0 is still deep in the green, up 10/32 at 101-05, but is 5/32 off the intraday high of 101-10. The timing of this retracement is poor as lock desks are in the process of creating rate sheets. This move will likely trim day over day rebate appreciations a bit but loan pricing should still improve by 15 to 25bps, that is unless MBS prices continue to fall. While the stock lever is exerting negative pressure on bonds we're not seeing much push-back from traders, which isn't surprising when one considers that Treasury will auction $66bn in debt supply next week. The broader trend in bonds is still bullish, but this price action should serve as another reminder of the risks associated with floating loans that must be locked on a short timeline. Even in a broader bullish trend, back-ups and reversals are always a threat. We will alert if stocks continue to rally and MBS shed more price gains.

9:02AM :

New MBS Commentary Post

8:53AM :

ALERT:

Rate Sheets to Benefit from Poor Payrolls Data

Rate sheets will improve today after bond markets reacted favorably to weak labor market data this morning. Nonfarm payrolls increased 54,000 last month when economists polled by Reuters had expected payrolls to rise 150,000. "Rate sheet influential" MBS coupons are +14/32 at 101-08, recovering almost all of the price declines experienced yesterday. The move in mortgages is being led by benchmark TSYs which have broken back into the 2.00% handle. 10s are currently +21/32 at 101-15 yielding 2.955% (-7.5bps). Based on this reaction loan pricing could improve by as much as 50bps.

8:41AM :

ECON: Job Growth Much Weaker than Expected

(Reuters) - Employment rose far less than expected in May to record its weakest reading since September, while the jobless rate rose to 9.1 percent as high energy prices and the effects of Japan's earthquake bogged down the economy. Nonfarm payrolls increased 54,000 last month, the Labor Department said on Friday, with private employment rising 83,000, the least amount since June. Government payrolls dropped 29,000. Economists polled by Reuters had expected payrolls to rise 150,000 and private hiring to increase 175,000 in May. The government revised employment figures for March and April to show 39,000 fewer jobs created than previously estimated. The job creation slowdown confirmed the economic weakness already flagged by other data from consumer spending to manufacturing. It could stoke fears about the depth and duration of a slowdown that started early in the year. The Labor Department said severe weather last month, including tornadoes and flooding, in the Midwest and the South did not materially affect data collection. It also said that while some workers in those regions may have been temporarily displaced from their jobs, it found "no clear impact of the disasters on the national employment and unemployment data for May." Economists still believe the lull in activity will be temporary. They cite high gasoline prices, bad weather and disruptions to motor vehicle production because of a shortage of parts from Japan as factors weighing on growth.

8:21AM :

Market Expecting Weak Employment Numbers

Rising jobless claims and Wednesday's much weaker ADP private jobs report have severely diminished forecasts for the all-important Nonfarm Payrolls employment report coming out at 8:30 ET. Predictions were already low at the start of the week - averaging 190k versus 244k the month before - and now it's more common to hear prayers for anything above 100k. "Last week, we had penciled in a below-consensus 170,000 gain in nonfarm payrolls, but following this week's cast of dismal economic characters, we'll be happy to take any six-figure number," said BMO Capital Markets an hour before the report. RDQ Economics commented Thursday: "We look for private payrolls to have risen 150,000 in May, which compares to an average monthly gain of 253,000 over the last three months (and we see total nonfarm payrolls up 140,000)."

Nomura Global Economics added: "We expect tomorrow's nonfarm payrolls to show employment expansion, but not at the levels required for a robust jobs recovery. Our forecast is for a 85k increase in nonfarm payrolls; 110k rise in private payrolls; 10k decline in manufacturing employment; and, an unchanged unemployment rate (9.0%)." The Unemployment Rate is still widely expected to inch down to 8.9%. Thirty minutes before the report, the benchmark 10-year Treasury yield is at 3.02%, versus 3.03% at Thursday's close. The two-year note remains at 0.46%, and the 30-year yield is down one basis point at 4.24%. Like Treasuries, mortgages are mostly flat. The FNCL 4.0 coupon is +3/32 at 96-28 and the 30 year FN4.5 is +1/32 at 100-27. Equity trading is equally cautious: S&P 500 futures are 5 points lower at 1,307.50 and Dow futures are 32 points down at 12,207. Commodity prices are lower. Light crude oil fell 0.79% overnight to $99.61 per barrel, and gold prices dropped 0.29% to $1,528.20 per ounce.

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Victor Burek : "then yesterdays reprice worse"

Victor Burek : "flagstar only .2 better"

Chris Kopec : "Just spoke with a friend of mine in the engineering business regarding the jobs report.....he said that engineering layoffs are accelerating due to the decision to mothball future nuke projects, as a result of the Japan earthquake/tsunami. So, American jobs are being held hostage thanks to Japanese tech/safety failures. Sounds like a typical government reaction."

Matthew Graham : "ISM NON-MANUFACTURING PRICES PAID INDEX 69.6 IN MAY VS 70.1 IN APRIL "

Matthew Graham : "ISM NON-MANUFACTURING EMPLOYMENT INDEX 54.0 IN MAY VS 51.9 IN APRIL "

Matthew Graham : "ISM NON-MANUFACTURING NEW ORDERS INDEX 56.8 IN MAY VS 52.7 IN APRIL "

Matthew Graham : " ISM NON-MANUFACTURING BUSINESS ACTIVITY INDEX 53.6 IN MAY (CONSENSUS 54.0) VS 53.7 IN APRIL "

Matthew Graham : "ISM REPORT ON U.S. NON-MANUFACTURING SECTOR SHOWS PMI AT 54.6 IN MAY (CONSENSUS 54.0) VS 52.8 IN APRIL "

Adam Quinones : "Plain and Simple: Payroll growth in May was way-weaker than expected at +54,000 jobs. April was revised worse by 12,000 jobs and March was reduced by 27,000 positions. The unemployment rate rose to 9.1% as the labor participation rate was unchanged and the number of people who said they were "employed" was less than the number of people who said they were "unemployed" in the household survey (BETTER EXPLANATION). Here is the ugliest stat of all: The number of people who've been jobless for longe"

Andrew Horowitz : "enough of "them" trying to tell the world that we can recover without the housing sector"

Adam Quinones : "resolution authority!"

Andrew Horowitz : "what the market needs is QE3 to target the Housing sector"

Adam Quinones : "...and the evolution of economic theory "

Matthew Graham : "back to CK, if you don't feel this way already, I think many of us will look back at these times in our lives and realize what a unique position we've been in to understand the evolution of the financial crisis"

Chris Kopec : "gm all....funny that the CNBC folks were all brainstorming ways to help the housing market..... hmmm, let's see: FHA MI, LLPAs, appraisal policy, QRM."

Matthew Graham : "Indeed. This is very much in line with a discussion yesterday on the value of the dashboard post-comp-change"

Jack Shotbolt : "Our clients WANT our expertise. I actually show the dashboard to my Realtors and Borrowers. I tell them "I monitor the bond market as your Investment experts monitor the Stock Market""

Adam Quinones : "get those referrals!"

Jack Shotbolt : "Christopher-You're correct, but we need to dig deep and find "ours", let the others starve. It's time work hard boys."

Christopher Stevens : "this may be great for rates but the big picture is our economy is in some serious trouble. the rates could drop to 4% but if people arent working and can't qualify for a mortgage it does not matter."

Adam Quinones : "prob will this AM after seeing lock desks finally hedge yesterday"

Adam Quinones : "Jack..we're about ready to award 4.0s with the title belt"

Adam Quinones : "B/D is not seasonally adjusted while the headline NFP print is."

Adam Quinones : "you cannot relate the B/D adjustment to the headline payrolls number"

Jack Shotbolt : "At what point do we move to the FNMA 4.0?"

Scott Valins : "from ZH: Take away the Birth/Death adjustment of 206,000 and the Real NFP is: -150,000. This is the biggest monthly B/D adjustment in over a year. And if as all the pundit claimed last month, demanding the McDonalds addition of 62,000 janitorial, part-time jobs be added to the May number, the economy really lost over 200,000 in May. Time to price in QE 666."

Adam Quinones : "weakness baked in."

Adam Quinones : "bonds acting exhausted here folks."

Adam Quinones : "MORE BREAKING NEWS: Yemeni President Saleh killed"

Adam Quinones : "S&P just broke 1300 support"

Matthew Graham : " WHILE SOME WORKERS LIKELY DISPLACED DUE TO STORMS, NO CLEAR IMPACT ON JOBS PICTURE SEEN IN MAY--LABOR DEPT. "

Matthew Graham : "SEVERE WEATHER IN MIDWEST, SOUTH DID NOT MATERIALLY AFFECT DATA COLLECTION FOR MAY EMPLOYMENT REPORT--LABOR DEPT. "

Matthew Graham : "NONFARM PAYROLLS WEAKEST SINCE SEPT 2010 (-29,000); JOBLESS RATE HIGHEST SINCE DEC 2010 "

Matthew Graham : "AGGREGATE WEEKLY HOURS INDEX FOR ALL PRIVATE WORKERS +0.1 PCT VS APRIL +0.5 PCT "

Matthew Graham : "GOODS-PRODUCING JOBS +3,000, CONSTRUCTION +2,000, PRIVATE SERVICE-PROVIDING JOBS +80,000, RETAIL -8,500 "

Matthew Graham : "FACTORY JOBS -5,000 (CONS. +14,000) VS APRIL +24,000 (PREV +29,000) "

Matthew Graham : "AVERAGE WORKWK ALL PRIVATE WORKERS 34.4 HRS (CONS 34.3 PCT) VS APRIL 34.4 HRS (PREV 34.3); FACTORY 40.6 VS 40.4, OVERTIME 3.2 VS 3.2 "

Matthew Graham : "AVERAGE HOURLY EARNINGS ALL PRIVATE WORKERS +0.3 PCT (CONS +0.2 PCT) VS APRIL +0.1 PCT (PREV +0.1 PCT), TO $22.98 VS APRIL $22.92; MAY YEAR-ON-YEAR EARNINGS +1.8 PCT "

Matthew Graham : " JOBLESS RATE 9.1 PCT (CONSENSUS 8.9 PCT) VS APRIL 9.0 PCT (PREV 9.0 PCT) "

Matthew Graham : "GOVERNMENT JOBS -29,000 VS APRIL -19,000 (PREV -24,000) "

Matthew Graham : "PRIVATE SECTOR JOBS +83,000 (CONS +175,000), APRIL +251,000 (PREV +268,000) "

Matthew Graham : "U.S. MAY NONFARM PAYROLLS +54,000 (CONSENSUS +150,000) VS APRIL +232,000 (PREV +244,000), MARCH +194,000 (PREV +221,000) "