MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:02 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

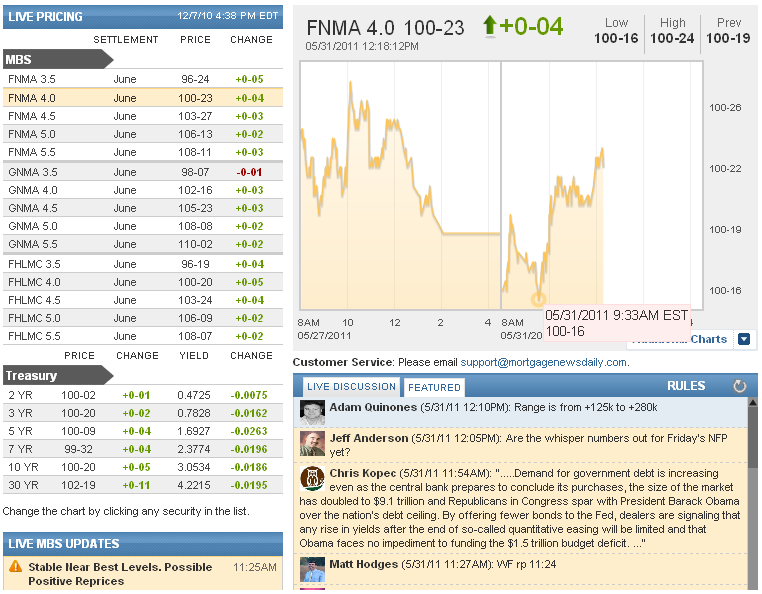

UPDATED! 11:25 : Stable Near Best Levels. Possible Positive Reprices

MBS are only up 3 ticks on the day, yet reprices for the better are becoming a possibility the longer we hold current levels. This isn't likely to be a widespread phenomenon, but for lenders pricing conservatively, and near this morning's low MBS marks, it's only a matter of time spent holding the highs of the day before a token or two is coaxed out of the worst rate sheets. Looking at 10yr notes by way of a benchmark for the general ocean of sentiment in which MBS swim, we get the overwhelming sense of "range reinforcement." What does that mean? 10yr yields carved out a new, lower notch in their range on Thursday and Friday with support bounces (ceiling) seen around 3.095 and resistance bounces (floor) seen around 3.055. Simply put, so far this morning, yields have see resistance and support bounces at the same levels, thus reinforcing this recent range. Although MBS hasn't made it back to their Friday highs in the same way 10yr yields made it back to Friday lows, FNCL 4.5's are still 3 ticks up on the day at 103-26. 10yr yields are at 3.0607 currently, and like MBS, haven't moved far from their best levels of the day. In the intermediate term, this 4 bp range in benchmark 10's is too narrow to be maintained for long. If it doesn't see a significant break before NFP, it's all but guaranteed after the report hits at 830am this Friday morning.

MBS are only up 3 ticks on the day, yet reprices for the better are becoming a possibility the longer we hold current levels. This isn't likely to be a widespread phenomenon, but for lenders pricing conservatively, and near this morning's low MBS marks, it's only a matter of time spent holding the highs of the day before a token or two is coaxed out of the worst rate sheets. Looking at 10yr notes by way of a benchmark for the general ocean of sentiment in which MBS swim, we get the overwhelming sense of "range reinforcement." What does that mean? 10yr yields carved out a new, lower notch in their range on Thursday and Friday with support bounces (ceiling) seen around 3.095 and resistance bounces (floor) seen around 3.055. Simply put, so far this morning, yields have see resistance and support bounces at the same levels, thus reinforcing this recent range. Although MBS hasn't made it back to their Friday highs in the same way 10yr yields made it back to Friday lows, FNCL 4.5's are still 3 ticks up on the day at 103-26. 10yr yields are at 3.0607 currently, and like MBS, haven't moved far from their best levels of the day. In the intermediate term, this 4 bp range in benchmark 10's is too narrow to be maintained for long. If it doesn't see a significant break before NFP, it's all but guaranteed after the report hits at 830am this Friday morning.

10:25AM :

March home prices suffer double-dip setback

(Reuters) - U.S. single-family home prices dropped in March, dipping below their 2009 low, as the housing market remained bogged down by inventory and weak demand, a closely watched survey said on Tuesday.

The S&P/Case Shiller composite index of 20 metropolitan areas declined 0.2 percent in March from February on a seasonally adjusted basis, in line with economists' expectations.

The price index was below the low seen in April 2009 during the financial crisis. The glut of houses for sale, foreclosures, tight credit and weak demand have kept the housing market on the ropes even as other areas of the economy start to recover.

The 20-city composite index was at 138.16, falling below the 2009 low of 139.26.

"This month's report is marked by the confirmation of a double-dip in home prices across much of the nation," David Blitzer, chairman of the index committee at S&P Indices, said in a statement. "Home prices continue on their downward spiral with no relief in sight."

Eight cities fell 1 percent or more in March, while Washington was the only city where prices increased on both a monthly and yearly basis. Prices in the 20 cities fell 3.6 percent year over year, topping expectations for a decline of 3.3 percent.

"The declines sustained in the last 12 months have almost erased the gains of the previous 12 months. The housing market is treading backward, but not drowning," said Cary Leahey, economist and managing director at Decision Economics in New York.

In the first quarter, the national index fell 1.9 percent on a seasonally adjusted basis, compared to a decline of 1.8 percent in the previous quarter. On a non-adjusted basis, they fell by 4.2 percent in the quarter. Nationally, home prices are back to their mid-2002 levels, the report said.

(Reporting by Leah Schnurr, additional reporting by Ellen Freilich, editing by W Simon )

10:16AM :

MBS Improve Following Weak Economic Data

With the last significant pieces of scheduled economic data of the morning, bond markets feel like they have all the information they need to turn losses into gains. MBS move from 2 ticks down to 2 ticks up as FNCL 4.5's rose to 103-25. 10yr notes had been threatening to break their 3.095 level in the midst of this morning's data, but have bounced quickly lower after the last report, moving past their Friday closing levels (3.075), to 3.068 currently. There's nothing else pressing on the economic calendar today, so we'd watch 3.095 for support in benchmark 10's and 103-23 in FNCL 4.5's. That doesn't mean reprices for the worse would come at those levels though. Just an indication that the presently bullish trend on the day could be shifting. In fact, lenders are pricing weaker this morning as many of them did not reprice with Friday afternoon's weakness. So with prices confirming those lower levels earlier this morning, we've seen that weakness creep onto rate sheets in some cases. At current levels, MBS are already close to justifying reprices for the better from the weakest-priced lenders this morning, although some have not even released rates yet. We'd expect a few lenders to reprice for the better if current prices merely hold steady, and naturally, more widespread reprices for the better if they were able to gain from there. For lenders already out with rates, we'd need to be near or below 103-20 to be concerned about reprices for the worse.

10:02AM :

Econ: US consumer confidence drops in May

NEW YORK, May 31 (Reuters) - U.S. consumer confidence slid in May as consumers turned more pessimistic on the outlook for the labor market and inflation worries rose, according to a private sector report released on Tuesday. The Conference Board, an industry group, said its index of consumer attitudes fell to 60.8 from a revised 66.0 in April. The reading was below economists' forecasts for 66.5. April was originally reported as 65.4. The expectations index tumbled to 75.2 from 83.2, while the present situation index edged down to 39.3 from 40.2. Consumers' labor market assessment was less favorable. The proportion of those who said jobs were hard to get rose to 43.9 percent from 42.4 percent the month before, although the "jobs plentiful" category also rose to 5.6 percent from 5.1 percent. Consumers were also more negative on their view of the labor market for the next six months. Those expecting more jobs in the coming months decreased to 15.9 percent from 17.8 percent, and those expecting fewer jobs rose to 20.8 percent from 18.7 percent. Consumers' expectations for inflation in the coming 12 months rose to 6.6 from 6.3 percent. (Reporting by Leah Schnurr; Editing by Padraic Cassidy)

10:00AM :

ECON: Chicago PMI Lowest Since Nov 2009

The Institute of Supply Management today released it's Purchasing Managers Index for May (aka "Chicago PMI"). The Index fell to 56.6 versus 67.6 in April. Economists had forecast a reading of 62.6. Readings above 50 indicate expansion. All the internal components of the report were weaker, with "new orders" down to 53.4 from 66.3, prices paid at 78.6 vs 81.8, employment to 60.8 vs 63.7 in April, and the production index at 56.0 vs 70 in April. Keep in mind that a weaker "prices paid" component is bond friendly in terms of a counter-inflationary implication. Several survey panelists mentioned higher fuel and commodity prices as impacting business conditions.

9:19AM :

Week Begins Slowly. Volume Low. Prices Sideways.

While Chicago PMI and Consumer Confidence are yet to come this morning, the few reports out so far have seen the morning off to a fairly slow start with MBS 1 tick lower than Friday's last marks. However, keep in mind that prices had risen through Friday morning and fell back to their lows of the day by 2pm. So even though we're virtually unchanged in terms of day-over-day MBS prices, it's not a guarantee that lender rate sheets will be. Benchmark 10yr TSYs are also near their Friday lows, but within the limits of the 3-day range beginning on Thursday with a high yield boundary centered on 3.095, a pivot point that saw at least 4 distinct resistance bounces earlier in the month before being broken on the 26th. With the data on tap later this morning, not to mention Friday's NFP, there's no guarantee that breakout will hold for long, but at least so far this morning, it still seems to be technically significant. 10yr notes are currently at 3.09.

9:02AM :

US home price index falls to double-dip in March-S&P

The S&P/Case Shiller composite index of 20 metropolitan areas declined 0.2 percent in March from February on a seasonally adjusted basis, in line with economists' expectations. The price index was below the low seen in April 2009 during the financial crisis. The glut of houses for sale, foreclosures, tight credit and weak demand have kept the housing market on the ropes even as other areas of the economy start to recover. The 20-city composite index was at 138.16, falling below the 2009 low of 139.26. "This month's report is marked by the confirmation of a double-dip in home prices across much of the nation," David Blitzer, chairman of the index committee at S&P Indices, said in a statement. "Home prices continue on their downward spiral with no relief in sight." Prices in the 20 cities fell 3.6 percent year over year, topping expectations for a decline of 3.3 percent. In the first quarter, the national index fell 1.9 percent on a seasonally adjusted basis, compared to a decline of 1.8 percent in the previous quarter. On a non-adjusted basis, they fell by 4.2 percent in the quarter. (Reporting by Leah Schnurr, Editing by Chizu Nomiyama)

7:59AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "...doesn't match the volume we saw last week in TSYs but it's still indicative of attentive activity. "

Adam Quinones : "A decent amount of volume out there already. 704k contracts traded in 10s. Mortgage volume above average. "

Adam Quinones : "This should be viewed as a reason to remain defensive in the short-term. Technical backups are always possible, especially when a "duration ledge" is met in the midst of a bull run in TSYs. (*Read "duration ledge" as a need for real money portfolio managers to adjust hedging strategies to better align cash-inflows to cash-outflows)"

Adam Quinones : "Did you know that stocks have a seasonal history of rallying after Memorial Day? Merrill Lynch traders this morning alerted us to the fact that, besides mid-July, the next 3 days have the highest probability of rallying for the entire year. "

Matthew Graham : "yeah, remember Friday that things weakened into the afternoon, on low volume, and with the sense that it didn't much matter on the short day ahead of the long weekend? So when prices began the morning in the same territory as that which was brushed off as inconsequential on Friday, it was all but guaranteed we'd be seeing weaker rates this morning. Now the curveball thrown by weak econ creates the betting pool as to how long it will take and at what levels to see reprices for the better. I mi"

Ken Crute : "some coupons .125% worse, some .125%-.25% better "

Chris Kopec : "If we can hold higher, I'd think so too, MD"

Mike Drews : "that should change by the end of day i'd think"

Chris Kopec : "GMAC about 18bp worse on the 30 year / 30 day"

Chris Kopec : "5/3 rates out....about 11bp worse on the 30 year 30 day"

Matthew Graham : "* US MAY CONSUMER CONFIDENCE INDEX 60.8 VS APRIL REVISED 66.0 (PREVIOUS 65.4) - CONFERENCE BOARD * US CONSUMER CONFIDENCE INDEX MEDIAN FORECAST FROM REUTERS FOR MAY WAS 66.5 * US CONSUMER PRESENT SITUATION INDEX IN MAY 39.3 VS APRIL REVISED 40.2 (PREVIOUS 39.6) * US CONSUMER EXPECTATIONS INDEX 75.2 IN MAY VS APRIL REVISED 83.2 (PREVIOUS 82.6) - CONFERENCE BOARD * US JOBS HARD-TO-GET INDEX 43.9 IN MAY VS APRIL REVISED 42.4 (PREVIOUS 41.8)--CONFERENCE BOARD * US 1-YEAR CONSUMER INFLATION RATE EXPE"

Victor Burek : "lets see if the markets care"

Victor Burek : "consumer confidence much lower"

Matthew Graham : "confidence 60.8"

Andrew Horowitz : "BB the consensus is 180k"

Brent Borcherding : "It's looking like a forgone conclusion that NFP will be weak, but can it be worse than what's already baked in?"

Matthew Graham : "Reinforcing the technical bounce. "

Matthew Graham : "* CHICAGO PURCHASING MANAGEMENT INDEX 56.6 IN MAY (CONSENSUS 62.6) VS 67.6 IN APRIL * CHICAGO PURCHASING MGMT NEW ORDERS INDEX 53.5 IN MAY VS 66.3 IN APRIL * CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX 78.6 IN MAY VS 81.8 IN APRIL * CHICAGO PMI EMPLOYMENT INDEX 60.8 IN MAY VS 63.7 IN APRIL * CHICAGO PURCHASING MANAGEMENT PRODUCTION INDEX 56.0 IN MAY VS 70.0 IN APRIL * CHICAGO PURCHASING MANAGEMENT INDEX AT LOWEST SINCE NOVEMBER 2009"

Matthew Graham : "chi PMI, lowest since 2009"

Victor Burek : "56.6"

Victor Burek : "chicago pmi much lower"

Matthew Graham : "3.095 flexing it's technical muscle in absence of data. pretty interesting."

Matthew Graham : "Stock lever pushing yields higher in general. 10's getting dragged around that 3.095 technical. Chicago PMI at 9:45 and Consumer Confidence at 10 may help inform that debate"

Matthew Graham : "S&P open about 10 higher"