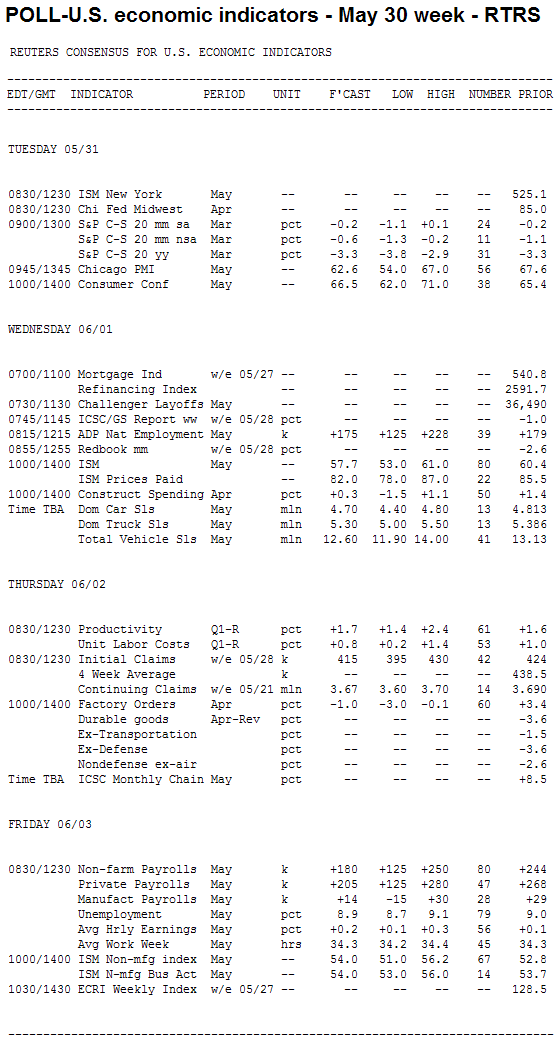

The week ahead holds key jobs data that will likely dictate market directionality as the 2nd Quarter comes to a close. The monthly Employment Situation Report will be released on Friday morning; investors expect it to confirm an economic slowdown is indeed in progress. Economists polled by Reuters see just 190k jobs were added to Nonfarm Payrolls in May versus 244k in April and 221k in March.

"Higher

readings of initial claims for unemployment insurance in recent weeks

have led to concerns about a softening labor market," said economists at

Nomura, who forecast a 175k print.

"We expect that private

job gains tailed off in May from the torrid pace of the previous three

months (averaging 253K)," said analysts at Citigroup. "The economy

simply is not growing fast enough to sustain that many new jobs.

Nevertheless, we think payroll employment expanded at a solid pace

again, with gains across a wide array of sectors."

Still, Treasuries are in profit taking mode after venturing even deeper into overbought territory as the risk trade has returned following a long Memorial Day weekend. Stocks are rallying around the globe...

U.S. equity futures are higher, following four consecutive weeks of decline. S&P 500 futures are +0.85% at 1341.25 while Dow futures are up 0.82% at 12,530.

Shares in China finished 1.38% higher, while those in Japan and Hong Kong closed 1.99% and 2.16% higher. The ongoing European session is seeing similar gains, with France's CAC-40 currently up 1.44%.

BMO noted the euro is among the top performing currencies with a 1% gain pushing it to above $1.44 for the first time in three weeks.

The spark?

Reports that finance officials from the European Union are considering the idea of providing more aid to Greece, plus a batch of new data from Asia including a strong manufacturing data out of Japan.

"Sentiment has turn positive after news rolled out that the EU ruled out restructuring Greece's debt," said economists at BMO Capital Markets. "Expect more money to flow to Greece, but with more tough conditions imposed."

The benchmark 10-year Treasury yield is currently yielding 3.09%, two basis points higher than Friday's close. The two-year note is yielding 0.496% and the 30-year yield is 4.25%. Mortgages are outperforming benchmarks though. The FNCL 4.0 is -0-01 at 100-18 while FNCL 4.5s are UNCH at 103-24.

Meantime, light crude oil opens the week +1.69% at $102.28 per barrel and gold pries are 0.07% lower at $1,535.20 per ounce.

Key Events This Week

Tuesday

9:00 - The S&P Case-Shiller Home Price Index last reported that prices across the 20 metropolitan areas it covers were 3.3% down from year-ago levels and a whopping 32.6% below peak levels. In February, the index fell just 0.2% - its smallest decline since July 2010. Economists anticipate the year-t0-year comparison to look a little worse in March, with the consensus prediction at -3.4%.

"Prices are affected by the large amount of distressed properties that are currently in the market," remind economists at BBVA, noting they accounted for one every three houses sold in the first quarter. "The financial institutions are processing distressed properties through short-sales or public auctions with a significant price discount. Looking forward, as prices get more attractive and labor market conditions improve, demand will slightly increase, leading average housing prices to stabilize once the distressed properties are cleared."

9:45 - The Chicago Business Barometer, a manufacturing and services index with an impressive track record of predicting the nationwide ISM index, is likely to produce another month of robust growth in May, albeit at a softer pace than earlier in the year. Economists forecast a score of 59 - nine points above the break-even point - but marking a downtrend from the 67.6 last month and the 70.6 two months ago.

"The Chicago purchasing managers' index has been in the stratosphere since December, registering the highest readings since the mid-1980s," wrote economists Citigroup.

"The extremely high readings no doubt reflected the substantial rebound in the motor vehicle sector as well as the general outperformance of the manufacturing sector," they added. "However, like other business diffusion indexes measuring breadth of change in activity, those elevated levels cannot continue indefinitely. In addition, the sudden pullback in motor vehicle production related to the Japanese tragedy probably hit Chicago-area parts suppliers. So we expect a pullback in the May Chicago index to a less frothy, but still strong reading."

10:00 - Most economists predict modest improvement in May's Consumer Confidence report from the Conference Board. There's a fair degree of uncertainty with jobless claims marching higher recently, the stock market sinking for four consecutive weeks, and oil prices displaying volatility, but the index is low enough to already account for these factors. The median estimate is 66.5, about one point higher than in April and nearly three points up from March.

"Consumer confidence has been edging higher since nose-diving in March," said economists at IHS Global Insight. "Recent news has been a mixed bag for the consumer. April payrolls and average hourly earnings improved, but the unemployment rate increased to 9.0%. Food and energy prices have moderated recently; weekly gasoline prices actually started falling in the latter part of the month. Stock market volatility and falling housing prices continue to hurt household net worth."

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

Wednesday

8:15 - The pace of private job growth is expected to remain flat in this month's ADP Private Employment Report. Analysts predict the index will show 178,000 new jobs created in May, versus 179,000 in April and 207,000 in March. The pace isn't too pleasing, as April's report marked the smallest gain since November.

Not much commentary was available for the report, but economists at Nomura pointed out their forecast for a 200k increase would be consistent with a forecast of 175k for Friday's nonfarm payrolls report.

"The ADP report captures those who cannot work temporarily due to bad weather, while nonfarm payrolls exclude these workers," they noted. "Moreover, the employment report (of which nonfarm payrolls is a part) covers public sector employment, which has been in steady decline."

10:00 - The ISM Manufacturing Index slowed for a second month in April to 60.4, its lowest since December. But overall the reading was quite robust, marking the 21st month of expansion in the sector with 17 of the 18 industries surveyed posting gains. The May report is forecast to be considerably less optimistic - the median estimate is 57 - but many point out any score above 55 is no indication of weakness.

"The ISM manufacturing index should falter in May as the manufacturing sector loses momentum," wrote analysts at IHS Global Insight. "The expected May reading of 55.3 is still healthy, just less ebullient than the boom-like readings of over 60 recorded for the first four months of 2011."

"It is difficult to estimate the direct and knock-on impacts of the earthquake in Japan and its drag on motor vehicle output, but that is at least a part of the story," they added. "Vehicles and parts are about 6% of the manufacturing sector (not even including the steel, glass, and plastics used in their manufacture) so they can never be ignored."

Citigroup had a similar outlook.

"We figure that the May ISM measure of manufacturing activity slipped somewhat from readings that were among the highest in the past quarter century," they wrote. "We figure the national index cannot sustain such elevated levels. However, even with the expected retreat in May, the ISM index probably remained at a buoyant level consistent with solid growth of factory output."

10:00 - Predictions for Construction Spending could hardly be more diffuse. While the so-called consensus expects a 0.4% increase in April, estimates range from a 1.5% drop-off to a healthy 1% gain. Some of the uncertainty relates to the previous report, where a higher-than-expected 1.4% jump may have been "payback from weather-related dips in prior months," as IHS Global Insight put it. The public sector/private sector dynamic offers further uncertainty.

"Construction spending will drop in April, mostly on a decline in residential construction," said economists at IHS Global Insight, predicting a 0.5% decrease overall. "Nonresidential construction, up two straight months, may show a further small increase. With infrastructure spending declining, a small decline in public construction is likely.

10:20 - John Williams, president of the San Francisco Fed, speaks on economics instruction to a conference on teaching economics and research.

12:25 - Sandra Pianalto, president of the Cleveland Fed, speaks on labor markets and monetary policy to the Columbus Metropolitan Club Forum.

12:30 - Fed Governor Daniel Tarullo speaks on U.S. and international financial regulatory reform to the Peterson Institute in Washington.

Treasury Auctions:

11:30 - 4-Week Bills

11:30 - 52-Week Bills

Thursday

8:30 - Initial Jobless Claims have surprised analysts by keeping above the 400k mark for the past seven consecutive weeks, and the most recent trends haven't been encouraging. Last week's report showed 424k new claims for unemployment insurance from 414k the week before; this week the estimate is 420k, with forecasts ranging from 410k to 440k.

"Nonstop extreme weather will likely keep claims elevated for yet another week," said economists at Nomura. "We continue to have confidence in a gradual labor market recovery, but doubt that claims will drop below 400k in the coming weeks."

8:30 - Not much is expected from the revised Productivity & Costs report for the first-quarter. As GDP was left unchanged in recent revisions, there's little to look out for. Productivity should remain at +1.6% or perhaps tick up to +1.7%, while unit labor costs should keep near its +0.8% gain.

"Because the first quarter GDP revision was so small and compensation was not altered, we do not look for much change in productivity and costs," said economists at Citigroup. "Nonfarm productivity likely will be revised up slightly and unit labor costs will move in the opposing direction. Markets are unlikely to take note of these small changes."

11:00 - Treasury will announce the terms of 3-year, 10-year, and 30-year debt supply to be auctioned in the following week.

Friday

8:30 - The month's most important economic report looks poised to disappoint. The Street believes just 190k Nonfarm Payrolls were added to the jobs list in May, versus 244k a month before and 221k in March.

"Higher readings of initial claims for unemployment insurance in recent weeks have led to concerns about a softening labor market," said economists at Nomura, who forecast a

175k print.

"We expect that private job gains tailed off in May from the torrid pace of the previous three months (averaging 253K)," said analysts at Citigroup. "The economy simply is not growing fast enough to sustain that many new jobs. Nevertheless, we think payroll employment expanded at a solid pace again, with gains across a wide array of sectors."

The Unemployment Rate is widely expected to inch down to 8.9%.

10:00 - Unlike its manufacturing cousin, the ISM Non-Manufacturing Index is actually supposed to do better in May compared to April, when a sharp drop-off pulled the index down 4.5 points to its lowest level since August. The median estimate puts the index at 54, up from 52.8 in April but below the 57.3 recorded two months before.

"The ISM non-manufacturing index likely gave up a bit more ground in May on some sogginess in the economy," said analysts at IHS Global Insight. "The services side of the economy and distribution are still growing, but the economy has lost momentum."

Economists at Citigroup pointed out that markets normally focus on the employment component of this report, but with the nonfarm payroll report coming out ninety minutes earlier, it probably won't command much attention.

3:30 - Eric Rosengren, president of the Boston Fed, speaks to the Stanford Finance Forum in Stanford, California.

MND'S CURRENT MORTGAGE RATE GUIDANCE: A big step was taken in the right direction for mortgage rates last week. We're now sitting at new 2011 lows heading into Non-Farm Payrolls in the week ahead. And while "The Wall" is still standing, there is now clear justification for borrowers looking to float their loan on an intermediate to long-term timeline. Further positive progress will however be slow and short-term back-ups are to be expected. From that point of view, borrowers working on a shorter lock/float timeline should remain defensive of new, lower "Best Execution" Mortgage Rate quotes. Your main goal is to keep new, lower note rate offers.