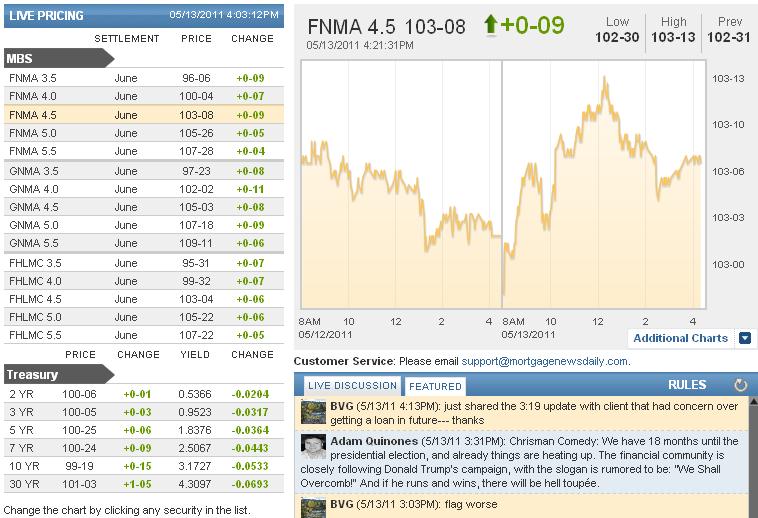

MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:01 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:19PM :

Mortgage Reform: New Secondary Market Legislation

Rep Gary Peters and Rep John Campbell (R-CA) have introduced a bipartisan plan to reform the mortgage market - putting an end to taxpayer-funded bailouts while preserving access to affordable mortgages for middle class families. The Campbell-Peters plan would overhaul the federal mortgage finance system and wind down the embattled mortgage giants, Fannie Mae and Freddie Mac, while establishing a new system of private associations - funded by private capital - to continue ensuring liquidity in the secondary mortgage market. While mortgage investments would still be backed by a government guarantee, the plan mandates strict standards, safeguards and capital requirements to protect taxpayers. Michael D. Berman, CMB, Chairman of the Mortgage Bankers Association, issued the following statement in reaction "The bipartisan legislation introduced by Congressmen Campbell and Peters to reform our secondary markets closely mirrors the proposal of MBA's Council on Ensuring Mortgage Liquidity, which was the first to put forward a comprehensive blueprint for the future of our housing finance system. "As Congress moves forward on this issue, which is so vital to our housing recovery, I want to thank the sponsors for putting forward this thoughtful legislation. MBA looks forward to working with the leadership of the House Financial Services Committee and Senate Banking Committee on comprehensive legislation that reforms our housing finance system in a way that encourages the return of private capital while also providing for a limited but explicit government role in backing the availability of affordable mortgage products through all market conditions."

3:13PM :

ALERT:

Reprices For The Worse Reported

We've seen our first lender reprice for the worse following the recent move back to the center of the day's range in MBS and TSYs. Neither have seen any further losses since the last update.

3:12PM :

MBA White Paper: Future of Residential Mortgage Servicing

The Mortgage Bankers Association (MBA) today released a new white paper which provides background information and an environmental scan of the events leading up to the current foreclosure crisis and examines some of the myths surrounding servicer incentives in the loss mitigation process. The white paper provides information on what a servicer does; how a servicer is compensated; and the perspectives of consumers, regulators, and the legal community with regard to servicer performance in the current crisis. It also identifies issues that need further examination and examines trends in servicer compensation and expenses.

"The housing crisis has caused us to question the way we do things. Acknowledging our mistakes is the first step in rebuilding trust in our industry and our actions," said Stevens. "MBA, and its members, are committed to being leaders in affecting the necessary changes to the residential loan servicing paradigm. We have invited, and will continue to welcome, all interested stakeholders to join us in this effort."

http://www.mortgagebankers.org/IndustryResources/ResourceCenters/Servicing21.htm

3:09PM :

Appraisal Institute Warns on Working with Some AMCs

The Appraisal Institute today cautioned real estate appraisers about signing agreements imposed by some appraisal management companies that seek to hold residential appraisers responsible for AMCs’ actions. Its president warned that consumers could be the ultimate losers. “Appraisers should be very careful about signing any agreement, especially one that makes them responsible for another party’s actions,” said Appraisal Institute President Joseph C. Magdziarz, MAI, SRA. “While there are some fine AMCs doing business today, many AMCs shift liability onto appraisers. For many professional appraisers, it’s simply not worth the risk.” Magdziarz, as president of the nation’s largest professional organization of real estate appraisers, noted that the most qualified, most competent appraisers often refuse to sign such indemnification agreements. “That means that consumers ultimately suffer, because the valuation of their property isn’t likely to be conducted by an appraiser with the most training, education and experience,” he said. “And without a reliable, credible opinion of value, everyone involved in a home sale suffers.” While lenders can manage appraisal operations with internal staff, some choose to outsource these functions to third-party management companies called AMCs. These firms act as “middlemen” between lenders and appraisers. “To get an idea of how potentially dangerous this situation is for appraisers, one need only look to the FDIC’s recent action,” Magdziarz said in reference to the Federal Deposit Insurance Corp. complaint filed May 9 against Lender Processing Services and CoreLogic that seeks to recover roughly $283 million in losses allegedly tied to appraisals. “Regardless of the merit of the FDIC’s charges, it’s clear that appraisers who sign indemnification agreements expose themselves to unnecessary liability that can ruin their careers and destroy their businesses.”

2:48PM :

MBS and TSYs Back to Mid-Range

Stocks saw their most successful rally attempt of the day beginning around 2pm. This kept some pressure on the bond market which had already been moderating off the aggressive 12:15pm levels, eventually bringing both 10's and MBS back to more central parts of their respective ranges on the day. For FNCL 4.5 MBS, that's at 103-05 and 3.186 in 10yr notes. Is it enough for reprices for the worse? It might be depending on the lender. Any reprices or rate sheets received close to that 12:15pm time frame are at a slight risk.

1:56PM :

Settling Into a Range as Volume Slows

The lowest yields seen today in 10yr notes exactly match the lowest yields seen on 5/6. The highest yields exactly match the lowest yields seen on 5/3 and the morning of 5/4. Conclusion: It's a range. This range is not the same sort of long term, indecisive period as that seen between December and February, but rather, it's more likely to be a pivot point on the longest charts. On a weekly chart, for instance, closing out today at current levels would make for a small bounce of last week's slightly lower Friday PM yields. From there, we either break 3.24 or 3.14 and continue on in that direction. In the grand scheme of things, this is a shorter period of consolidation in the context of a much larger trend. What's unknown is whether or not the recent trend is the one that continues or if 3.14 will prove to be a resistance level that we do not get through at this time. The lovely thing about narrow ranges like this is that the support levels serve as excellent lock indicators if they're broken and the resistance levels as excellent longer term float indicators and short term lock indicators if they're broken (think "profit-taking").

12:50PM :

ALERT:

Reprices for the Better Reported as Bonds Surge

Earlier we mentioned the trendline resistance at 3.16+ and that if it broke, the next suggested technical level was 3.14. After 3.16+ gave way, 3.14 followed shortly thereafter, but has shown that it's much more of a resistance level than a pivot point. Yields bounced convincingly and are currently back up to 3.158, but this is still a better yield range than the earlier parts of the day (obviously). So although MBS haven't been able to keep up with the pace set by their benchmark guidance givers, they are much improved, a few ticks off their 103-13 highs of the day at 103-11. That's about 9 ticks up on the day and the directional rally has been enough for several lenders to reprice for the better in what's likely to be a day that sees a majority of lenders release improved rates at least once. There's volume behind the moves as well, but just as that volume confirms the current range, so too does it confirm the technical bounce at 3.14. This lower limit level remains firm resistance for now.

11:18AM :

ALERT:

Best MBS Levels of The Day. Possible Positive Reprices.

With economic data done for the week and emergent inflation concerns generally soothed by today's data, bonds are willing to rally and willing to take guidance from the stock lever. With S&P's having fallen from the 1347's to 1343's in the last 20 minutes, 10yr notes and MBS have moved to their best levels of the day. 10's are currently at 3.171 after bouncing on the consolidating trendline resistance mentioned earlier. It could still break, and if it does, then 3.14 would be the next suggested test. FNCL 4.5's are up 7 ticks on the day to 103-09 making reprices for the better a possibility or simply improved rates from lenders who aren't out with sheets yet.

11:17AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "Chrisman Comedy: We have 18 months until the presidential election, and already things are heating up. The financial community is closely following Donald Trump's campaign, with the slogan is rumored to be: "We Shall Overcomb!" And if he runs and wins, there will be hell toupée."

BVG : "flag worse"

Steven Bote : "AFR reprice for the better"

Victor Burek : "nexbank better"

Brent Borcherding : "Wells Reprice"

Adam Quinones : "MBS cant keep up."

Adam Quinones : "pretty big volume in 10s."

Jill Statz : "Flagstar better"

Chris Kopec : "Since when was housing important?"

Chris Kopec : "“As we look back at the week and forward to the next, one begins to get the feeling that the U.S. economy is not about to run away from anyone,” Kevin Giddis, president of fixed-income capital markets at the brokerage firm Morgan Keegan Inc. in Memphis, Tennessee, wrote in a note to clients. “Some of the major issues like housing and jobs are slow to get better.” http://noir.bloomberg.com/apps/news?pid=20602007&sid=aXDO6q.qpi7o"

Brett Boyke : "Wells RP"

Oliver S. Orlicki : "pfg +.125"

Ira Selwin : "famc price change"

Adam Quinones : "http://www.mortgagenewsdaily.com/consumer_rates/208606.aspx"

Adam Quinones : "http://www.mortgagenewsdaily.com/mortgage_rates/blog/159874.aspx"

Adam Quinones : "there's more..."

Michael Stark : "HAHA! I had just found it. Thanks AQ."

Adam Quinones : "Michael Stark: http://www.mortgagenewsdaily.com/mortgage_rates/blog/210063.aspx"

Michael Stark : "Thanks I get that, but was hoping to share some of the eloquently worded write ups about this subject with some new potential members to demonstrate the content of what we get here."

Andrew Horowitz : "BS need to see the spread between the 4 and the 4.5 tighten up to about 2.625 instead of 3.125"

Bert Swyers : "4.75 is best ex right now and will be until the 4.0 hits at least 101"

Bert Swyers : "we need to shift to the 4.0 coupon to see that big gap go away, we are closer than we have been in a long tim to that happening"

Michael Stark : "AQ - can I have a link to the article about why rates have such a huge step in pricing from say 4.75 to 4.5 and why we hit resistance when trying to move down...?"

Andrew Horowitz : "i would rather see 3.16 today and then retest 3.14 early next week"

Andrew Horowitz : "think we hit 3.14 today, not sure if that is a good thing though, "

Steven Bote : "I agree. Not too much else on the platter for the day."

Matthew Graham : "but doubtful we could muster meaningful volume for that"

Matthew Graham : "if we break 3.16, then 3.14 is the next suggested test"

Matthew Graham : "we're right on the edge of the more narrow consolidating range that lies within the broader 3.14 to 3.24 tange"

Steven Bote : "That and low volume Fridays, I'd imagine."

Shane : "stock lever"

Shane : "3.14 today AH?"