MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:01 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:32AM :

ECON: ECRI Index Rises to 129.7 versus 128.7

NEW YORK, May 13 (Reuters) - A measure of future U.S. economic growth rose in the latest week, but the growth rate weakened on an annualized basis, a research group said on Friday.

The Economic Cycle Research Institute, a New York-based independent forecasting group, said its Weekly Leading Index rose to 129.7 in the week ended May 6 from 128.7 the previous week.

The index's annualized growth rate, however, slowed to 6.4 percent from a revised 6.6 percent a week earlier. It was originally reported at 6.7 percent. ((Reporting by U.S. Markets and Economics Desk)

10:28AM :

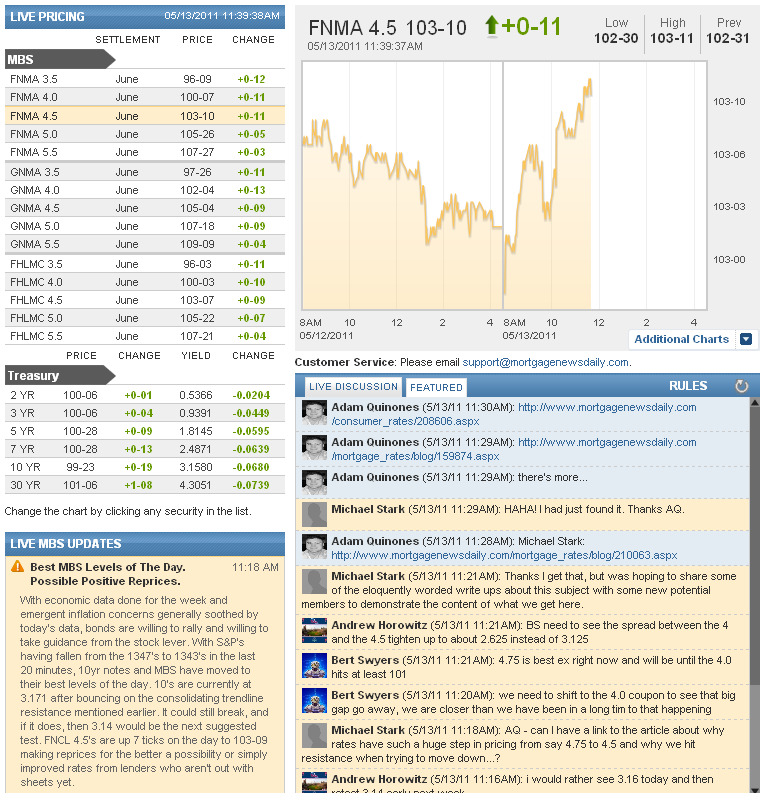

TSY's Rally Within Recent Ranges, MBS Improve

Since May 4th, yields in 10yr notes have seen a series of progressively lower highs and higher lows. The widest level of the range was seen on May 6th, establishing high yield support at 3.24 and low yield resistance at 3.14. The range had narrowed to 3.23 / 3.165 today and indeed the actual yields seen today are very close to hitting those marks. After coming in the door at 3.23 and seeing an initial rally on CPI data, 10's rallied further following Consumer Sentiment data, reaching the higher 3.16's and then bouncing up to the high 3.17's currently. MBS had been severely underperforming earlier, but now stand 10 ticks improved on the day at 103-09, closing the performance gap somewhat and once again making reprices for the better possible from perhaps a few odd lenders that might have priced before 830am this morning. Other lenders who had not released rates should now be able to come out with improved offerings.

10:13AM :

ECON: Philly Fed Survey Sees Inflation Risks in Q2

Growth in the U.S. economy looks a little slower now than it did three months ago, according to 44 forecasters surveyed by the Federal Reserve Bank of Philadelphia. Our panelists expect real GDP to grow at an annual rate of 3.2 percent this quarter, down from the previous estimate of 3.5 percent. On an annual-average over annual-average basis, the forecasters also predict slower real GDP growth over the next four years. The forecasters see real GDP growing 2.7 percent in 2011, down from their prediction of 3.2 percent in the last survey. The forecasters predict real GDP will grow 3.0 percent in 2012, 2.8 percent in 2013, and 3.3 percent in 2014, each somewhat lower than their respective predictions in the last survey.

The forecasters predict higher inflation, both in the short run and over the long run, for the survey's four measures of inflation. The forecasters expect current-quarter headline CPI inflation to average 3.5 percent, up from the last survey's estimate of 1.3 percent. The forecasters predict a higher current-quarter headline PCE inflation of 2.7 percent, up from the last survey's estimate of 1.3 percent.

Measured on a fourth-quarter over fourth-quarter basis, headline CPI inflation is expected to average 3.1 percent in 2011, 2.2 percent in 2012, and 2.3 percent in 2013, higher than the forecasts of 1.7 percent, 2.0 percent, and 2.1 percent, respectively, in the last survey.

Over the next 10 years, 2011 to 2020, the forecasters expect headline CPI inflation to average 2.4 percent at an annual rate. This estimate is up slightly from 2.3 percent in the last survey.

10:01AM :

ECON: Consumer Sentiment Rises to 72.4 from 69.8

May's preliminary reading of Consumer Sentiment Rose to 72.4 from an April Final reading of 69.8 Leading the gains were the expectations component which rose to 67.4 from 61.6 last month and the 12-Month Economic Outlook which rose from 74 last month to 83 in the current report. Current Conditions, however, dropped from 82.5 to 80.2. The 1 year inflation outlook dropped from 4.6 to 4.4, while the 5 year outlook was marginally higher, from 2.9 to 3.0. Of note, the survey shows that the killing of Bin Laden had no impact on consumer's expectations for the economy.

9:47AM :

TSYs Correct Steep AM Rally. MBS Overcorrect

Shortly after dipping into the high 3.18's, 10yr TSYs made a minor corrective bounce up to the high 3.19's. During the same time, MBS fell 103-07 to 103-03, leaving them basically unchanged from yesterday's latest levels. Consumer Sentiment data is on the way in about 10 minutes.

9:03AM :

Following CPI, MBS, TSY's Rally

In the half hour since April CPI was reported in line with expectations, both MBS and TSYs have rallied decisively. 10yr yields are down almost 4 bps to 3.193 and FNCL 4.5's are up 8 ticks on the day now at 103-07. This is all happening early enough that it should have a net positive impact on most lenders rate offerings this morning. If a particular lender is already out with pricing this morning, we'd likely be waiting a bit longer for gains to hold in order to expect any reprice for the better.

8:39AM :

ECON: April Core CPI +0.2. Meets Consensus

Ongoing indications of the margin squeeze as the increases in producer-level prices noted in yesterday's data are indeed not translating to similar increases in consumer level prices. The April Consumer Price Index rose 0.4%, which was exactly in line with expectations as was the core CPI reading of +.2%. Year over year measurements were also right on the screws at +1.3% for the core. The index itself stands at 224.906 vs 224.85 consensus and a 223.467 reading in March. Seasonally adjusted, however, the index for April is 223.745 vs 223.331 in March. Also of note in the report, Real Earnings in the private sector continue to decelerate their negative trend moving to -0.3% from -0.4% last month and -0.5% in Feb. Bond markets are rallying on the data which, although in-line with estimates, was feared to have shown a similar bearish discrepancy due to PPI coming in slightly worse than expected yesterday.

8:15AM :

New MBS Commentary Post

UPDATED AT 11:43AM.