MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:01 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:38AM :

ALERT:

Seeing HALF the Expected Amount of Volatility. Don't Panic

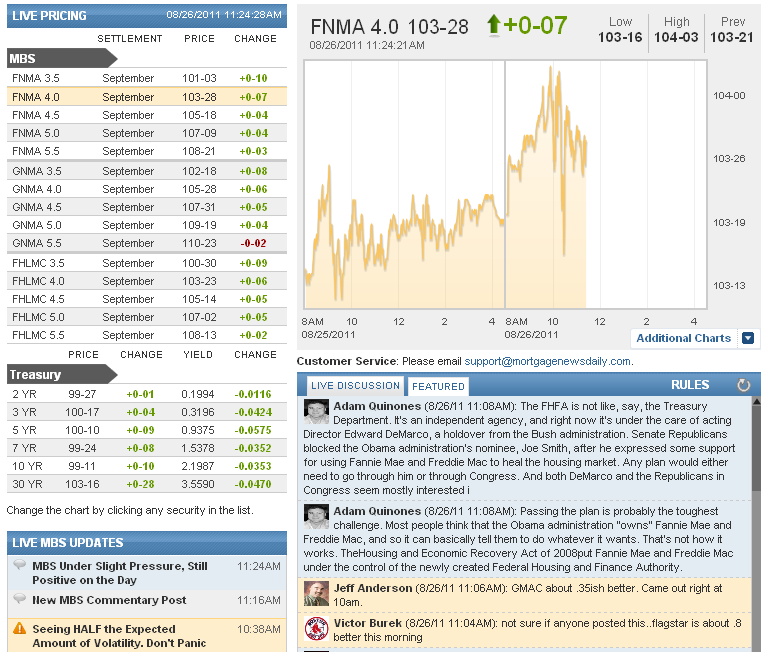

MBS dipped from 104 ish to 103-16 in the blink of an eye. 10yr yields rose from 2.13 to 2.21 in the same blink. But those are tame swings! Here's why: Over the last 3 Jackson Hole days 10yr yields have swung an average of 16bps. We've swung about 8bps today. Believe us, we KNOW how ridiculous the swings seem right now, but this is VERY normal and VERY tame compared to expectations. The fact that recent swings in 10yr yields took them exactly to a technical level and that we saw a supportive bounce only reinforces the notion that we have no reason to panic. Caveat: we're not intimately familiar with how up to speed every lender is with their economic research and the extent to which that impacts (or moderates) their repricing decisions. It's always possible a large swing down in MBS like the one we just saw could cause reprices, but Fannie 4.0's are back to 103-30 now. 10yr yields are at 2.188.

10:28AM :

Highlights From Jackson Hole

(Reuters) - On economic growth, inflation outlook:

"The recent data have indicated that economic growth during

the first half of this year was considerably slower than the

Federal Open Market Committee had been expecting, and that

temporary factors can account for only a portion of the

economic weakness that we have observed. Consequently, although

we expect a moderate recovery to continue and indeed to

strengthen over time, the Committee has marked down its outlook

for the likely pace of growth over coming quarters. On what the Fed's recent policy decision means:

"We indicated that economic conditions -- including low

rates of resource utilization and a subdued outlook for

inflation over the medium run -- are likely to warrant

exceptionally low levels for the federal funds rate at least

through mid-2013. That is, in what the Committee judges to be

the most likely scenarios for resource utilization and

inflation in the medium term, the target for the federal funds

rate would be held at its current low levels for at least two

more years." On what other tools the Fed has:

"In addition to refining our forward guidance, the Federal

Reserve has a range of tools that could be used to provide

additional monetary stimulus. We discussed the relative merits

and costs of such tools at our August meeting. We will continue

to consider those and other pertinent issues, including of

course economic and financial developments, at our meeting in

September, which has been scheduled for two days (the 20th and

the 21st) instead of one to allow a fuller discussion. The

Committee will continue to assess the economic outlook in light

of incoming information and is prepared to employ its tools as

appropriate to promote a stronger economic recovery in a

context of price stability."

10:04AM :

Fed Prepared to "Use Tools," But No QE3 Hints

(Reuters) - Federal Reserve Chairman Ben Bernanke on Friday stopped short of signaling further action to boost growth, but said it was critical for the economy's health to reduce long-term joblessness.

"It is clear the recovery from the crisis has been much less robust than we had hoped," he said in remarks prepared for delivery to an annual Fed retreat.

Bernanke said the Fed will meet for two days in September instead of the planned one to mull its options to provide additional monetary stimulus, among other topics.

The Fed chairman said reducing the record high level of workers who have been unemployed for six months or more would help achieve stronger U.S. economic growth.

"Under these unusual circumstances, policies that promote a stronger recovery in the near term may serve longer-term objectives as well," he said.

(Reporting by Mark Felsenthal; Editing by Neil Stempleman)

9:59AM :

ECON: Consumer Sentiment Sinks in August

(Reuters) The Thomson Reuters/University of Michigan's consumer sentiment index edged up from its mid-August level but was still consistent with recession-era lows. The index has only been lower in three other surveys, which were taken in April and May 1980 and November 2008. The final August reading on the overall index of consumer sentiment was at 55.7, down from 63.7 the month before. It was slightly better than August's preliminary reading of 54.9, which had been the lowest level since May 1980. Economists polled by Reuters had forecast a reading of 56.0. "Consumers have shifted from being optimistic about the potential impact of monetary and fiscal policies to a sense of despair and pessimism about the role of the government," survey director Richard Curtin said in a statement.

The survey's barometer of current economic conditions was 68.7, down from 75.8 in July and below a forecast of 69.3. The component is at its lowest level since August 2009, just after the official end of the recession.

The outlook also worsened, with the gauge of consumer expectations falling to 47.4 from July's final reading of 56.0, but above an expected 45.7.

The survey's one-year inflation expectation rose to 3.5 percent from 3.4 percent, while the five-to-10-year inflation outlook held steady at 2.9 percent. (Reporting by Leah Schnurr; Editing by Padraic Cassidy)

9:27AM :

The Obama Administration Can't Refi Your Mortgage on Its Own

Most people think that the Obama administration 'owns' Fannie Mae and Freddie Mac, and so it can basically tell them to do whatever it wants. That’s not how it works. The Housing and Economic Recovery Act of 2008 put Fannie Mae and Freddie Mac under the control of the newly created Federal Housing and Finance Authority. The FHFA is not like, say, the Treasury Department. It’s an independent agency, and right now it’s under the care of acting Director Edward DeMarco, a holdover from the Bush administration. Senate Republicans blocked the Obama administration’s nominee, Joe Smith, after he expressed some support for using Fannie Mae and Freddie Mac to heal the housing market. Any plan would either need to go through him or through Congress. And both DeMarco and the Republicans in Congress seem mostly interested in limiting Fannie and Freddie’s short-term losses so they can be spun off from the government.

9:08AM :

ALERT:

Bond Markets Shift in Favor of More Bullish "Middle Ground" After GDP

After a fairly lackluster GDP this AM, MBS and Treasuries traded sideways for a bit, but have rallied in the past few minutes. That comes on the heels of what were already slightly stronger opening levels. As S&P futures approached the 1150 technical level, MBS and 10yr yields did the same, 103-28 for Fannie 4.0's and 2.17+ for 10's. Treasuries went out the door just over 2.23 yesterday, the exact mid-point between important technical boundaries at 2.06 and 2.40 (hat tip to the Dashboard's Brent B on being the first to comment on this yesterday). The AM data and trading shifts yield to the next notch lower in yield on the technical ladder: 2.17-2.18. Additionally, 103-28 is a well traveled pivot of late having supported prices almost all day on the 23rd and then acting as resistance ever since that day's Treasury auction. The next major data comes in just under an hour with Consumer Sentiment at 9:55am, but most importantly, Bernanke at Jackson Hole at 10am. Lenders should be able to pass on some gains this morning depending on how sensitive they are to the J-Hole-Related uncertainty. Implied volatility in the options market (like fixed income's very own .VIX in a way) is in line with recent highs, which, for lack of a better term, are very high. That's likely a factor in Treasuries outpeforming MBS somewhat this AM and also raises the possibility of more hesitant pricing or even delayed rate sheets until the first shockwaves are felt from Jackson Hole.

8:54AM :

ECON: Corporate Profits Rose 4.1 Percent in Second Quarter

The Commerce Department today reported that Corporate Profits rose by a seasonally adjusted 4.1 pct in the 2nd quarter vs 0.1 pct in Q1. Corporate profits after tax include inventory valuation and capital consumption adjustments. Profits from current production do not reflect tax law changes that would affect profits as reported to tax authorities. The 4.1 pct figure is an After Tax profit and benefited from a fall in corporate income taxes by 0.7 pct. It had risen by 4.3 pct in the previous quarter.

8:38AM :

ECON: GDP Revised Down to 1 Percent in 2nd Quarter

(Reuters) - GDP growth rose at annual rate of 1.0 percent the Commerce Department said, a downward revision of its prior estimate of 1.3 percent. It also said after-tax corporate profits rose at the fastest pace in a year.

Economists had expected output growth to be revised down to 1.1 percent. In the first quarter, the economy advanced just 0.4 percent.

Output was curbed by exports, which grew at a 3.1 percent pace instead of 6.0 percent. Imports increased at a 1.9 percent rate rather than 1.3 percent. That left a slightly wider trade deficit and trade barely contributed to GDP growth. Trade had previously been estimated to have added 0.58 percentage point to overall output.

The drag from business inventories was offset by consumer spending, which was revised up to a 0.4 percent rate from 0.1 percent. The increase in spending, which accounts for more than two-thirds of U.S. economic activity, was still the smallest since the fourth quarter of 2009.

Business spending was revised to a 9.9 percent rate of increase from 6.3 percent as investment in nonresidential structures and equipment and software was stronger than previously estimated. But there are fears that the recent stock market rout could make businesses a bit hesitant to spend on capital and hiring.

The report also showed that after-tax corporate profits increased 4.1 percent in the second quarter after edging up 0.1 percent in the first three months of the year. It also showed inflation pressures abating, with the personal consumption expenditures price index rising at a 3.2 percent rate. That compared to 3.9 percent in the first quarter.

The core PCE index closely watched by the Fed advanced at a 2.2 percent rate, the largest increase since the fourth quarter of 2009. It was revised up from 2.1 percent. (by Lucia Mutikani; Editing by Neil Stempleman)

7:12AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "I like Volz's techs there"

Matthew Graham : "RTRS - ROGER VOLZ, DIRECTOR OF CASH EQUITIES AT BGC FINANCIAL IN NEW

YORK: "The initial reaction was to sell the non-event, now we're getting some short-covering. There's still a negative lean on the day, if we hold below 1,141 at the close I'm looking for us to retest recent lows around 1,127. At this stage, there's no help from Mr. Bernanke. The early read was nothing of any import or anything dramatic. The market is taking it as a negative; the next question is how we flush through this to"

MMNJ : "digest and rally"

Matthew Graham : ""have tools" not "expect qe3"

Oliver S. Orlicki : "s & p down over 1.5"

Victor Burek : "outlook for growth is lower...inflation under control"

Matthew Graham : "stocks tanking"

Victor Burek : "sure seems bond friendsly so far"

Matthew Graham : "RTRS - BERNANKE - ECONOMIC HEALING WILL TAKE A WHILE, WILL NEED TO REMAIN ALERT TO RISKS TO RECOVERY, INCLUDING FINANCIAL RISKS "

Matthew Graham : "RTRS - BERNANKE - FINANCIAL STRESS CONTINUES TO BE SIGNIFICANT DRAG ON ECONOMY AT HOME AND ABROAD "

Matthew Graham : "RTRS - BERNANKE - EXPECT INFLATION TO SETTLE AT LEVELS AT OR BELOW 2 PCT, OVER COMING QUARTERS "

Matthew Graham : "RTRS - BERNANKE - DATA SUGGEST MORE PERSISTENT DRAGS, NOT JUST TEMPORARY FACTORS, RESTRAINING GROWTH "

Matthew Graham : "RTRS - BERNANKE - FED HAS MARKED DOWN ITS OUTLOOK FOR GROWTH OVER COMING QUARTERS "

Matthew Graham : "RTRS - BERNANKE REPEATS FED HAS RANGE OF TOOLS TO PROVIDE MORE ECONOMIC STIMULUS, DISCUSSED THOSE TOOLS AT AUGUST MEETING "

Matthew Graham : "RTRS - BERNANKE - FED TO MEET FOR TWO DAYS INSTEAD OF ONE IN SEPTEMBER TO CONSIDER TOOLS TO PROVIDE ADDITIONAL MONETARY STIMULUS, OTHER ISSUES "

Matthew Graham : "RTRS - FED'S BERNANKE - RECOVERY FROM CRISIS MUCH LESS ROBUST THAN HOPED "

Matthew Graham : "Also out at GDP time: RTRS - US Q2 CORPORATE PROFITS AFTER TAX +4.1 PCT VS Q1 +0.1 PCT (PREV +0.1 PCT) "

Matthew Graham : "RTRS- US Q2 BUSINESS INVENTORY CHANGE CUTS 0.23 PERCENTAGE POINT FROM GDP CHANGE"

Matthew Graham : "RTRS- US Q2 BUSINESS INVENTORY CHANGE +$40.6 BLN (PREV +$49.6 BLN) "

Matthew Graham : "RTRS- US Q2 YEAR-ON-YEAR PCE PRICE INDEX +2.5 PCT (PREV +2.5 PCT), CORE PCE +1.3 PCT (PREV +1.3 PCT) "

Matthew Graham : "RTRS- US Q2 GDP EX MOTOR VEHICLES +1.2 PCT (PREV +1.4 PCT) "

Matthew Graham : "RTRS- US Q2 EXPORTS +3.1 PCT (PREV +6.0 PCT), IMPORTS +1.9 PCT (PREV +1.3 PCT) "

Matthew Graham : "RTRS - US Q2 HOME INVESTMENT +3.4 PCT (PREV +3.8 PCT), BUS. INVESTMENT IN STRUCTURES +15.7 PCT (PREV +8.1 PCT) "

Matthew Graham : "RTRS - US Q2 BUSINESS INVESTMENT +9.9 PCT (PREV +6.3 PCT), EQUIPMENT/SOFTWARE +7.9 PCT (PREV +5.7 PCT) "

Matthew Graham : "RTRS - US Q2 CONSUMER SPENDING +0.4 PCT (PREV +0.1 PCT); DURABLES -5.1 PCT, BIGGEST DECLINE SINCE Q4'08, (PREV -4.4 PCT) "

Matthew Graham : "RTRS - US Q2 PCE PRICE INDEX +3.2 PCT (CONS +3.1 PCT), PREV +3.1 PCT; CORE PCE +2.2 PCT (CONS +2.1 PCT), PREV +2.1 PCT "

Matthew Graham : "RTRS - US PRELIM Q2 GDP DEFLATOR +2.5 PCT (CONS +2.3 PCT), PREV +2.4 PCT "

Matthew Graham : "RTRS- US PRELIM Q2 GDP +1.0 PCT (CONSENSUS +1.1 PCT), PREV +1.3 PCT; FINAL SALES +1.2 PCT (CONS +1.0 PCT), PREV +1.1 PCT "