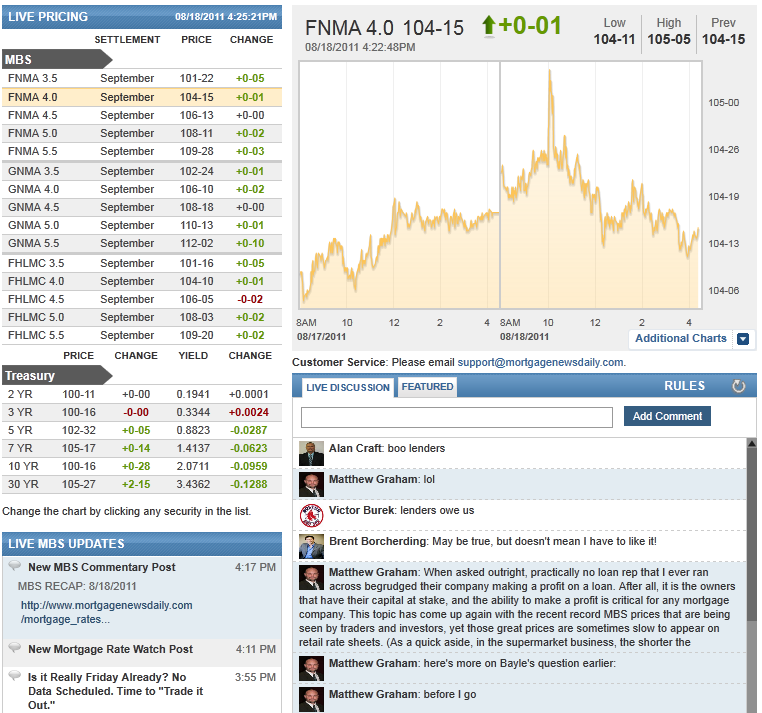

MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:02 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:55PM :

Is it Really Friday Already? No Data Scheduled. Time to "Trade it Out."

As is sometimes the case on Fridays, tomorrow's calendar of scheduled economic data is completely empty, although there are two Fed speakers, Dudley at 830am and Pianalto at 1:45pm. We're fairly fond of anything that we can glean from the Fed these days both because of the nearness in history of the FOMC announcement that rocked the market, it's unprecedented number of dissenting voters, as well as next Friday's Jackson Hole Bernanke speech. But even if the Fed speakers tomorrow do little to move markets, the absence of economic data combined with the epic nature of today's moves in Treasuries, not to mention to potential technical breakdown in stocks, could make for a great day of what we've recently dubbed "trading it out," where we observe the interplay of one market against the other, each relying on a framework of technical trends and stopping points as they gradually come to a consensus with one another. Ha! Who needs octagons or ringside seats?! This is the best brawl we've seen in a long time! For a bit of context, and a closer look at how the technical developments in Stocks and Treasuries have been affecting MBS (and ultimately, what makes its way onto rate sheets), take a look at the following link):

2:56PM :

Update on Treasury’s MBS Wind Down – Taxpayers Recoveries Reach 70 Percent Milestone

Treasury has now recovered more than 70 percent ($159.5 billion) of its original $225 billion investment in MBS, which it made during 2008 and 2009 through authority provided to it by Congress under the Housing and Economic Recovery Act of 2008. These MBS purchases helped stabilize the financial markets and preserve access to mortgage credit during a period of unprecedented market stress.

The MBS market has improved considerably since Treasury purchased these securities. Based on current market conditions, Treasury expects to make a profit for taxpayers on this investment.

On March 21, 2011, Treasury announced that it would begin the orderly wind down of its MBS portfolio. Treasury plans to sell up to $10 billion MBS (principal) per month, subject to market conditions. The sale is part of Treasury’s continued efforts to wind down emergency financial crisis response programs that were put in place in 2008 and 2009.

For additional details on Treasury’s remaining MBS portfolio, please visit

2:21PM :

New MBS Commentary Post

1:47PM :

ALERT:

MBS Mostly Able to Hang on to Yesterday's Closing Marks. Rebounding

After poking and prodding at a break up into the 2.10's, 10yr yields are back down to 2.073. Stocks are trending downward and S&P's are currently at 1138.87 still about 4 points higher than lows this morning. MBS are mostly along for the ride, but whereas Treasuries enjoy the roller-coaster, MBS are a bit nauseous. In other words, Treasuries are a direct beneficiary of the stock sell-off and volatility--a true "safe haven" for flight-to-safety bidding. MBS never gain as well as TSYs when the "risk-off" sentiment pervades markets. But MBS have been able to claw their way at least back above yesterday's closing marks in 4.0's and actually bounce at yesterday's closing marks in 3.5's. Combined with the 10yr note holding under 2.10, these are promising technical developments. They speak to an entrenchment against rapid losses into the afternoon, whereas that might have been a fear if you simply saw MBS prices move from record highs at 10am sharply to the lows of the day by noon. For now, that particular dip in the roller-coaster ride appears to have leveled off. Watching how stocks respond to the approach to their lows of the day for further bond-market guidance. Some of the reprices for the worse that came across now look out of line with the day's market movements. Maybe other factors at work there... Could make sense given strong rate offerings under 4.25% may have spurred a lot of lock demand yesterday and this morning. The rapidly correcting market provided a good opportunity for a big reprice (or two) from lenders who not only needed to adjust for market conditions but also control the pipeline a bit. There's an implication here, and that is that sideways or even improving prices don't mean immunity from reprices for the worse. Know your lender though. Some are more predisposed than others to pipeline motivated price changes.

12:33PM :

ALERT:

MBS Falling. Reprices for Worse Possible

Production MBS coupons have given back early morning gains thanks to widespread profit taking in the bond market. The Fannie Mae 4.0 is currently bid +2/32 at 104-16 after trading as high as 105-05 following a weak regional manufacturing read at 10am. This fall from new record highs is enough to warrant reprices for the worse. Beware. The pain will be most felt at rates below 4.25%.

11:17AM :

New MBS Commentary Post

11:03AM :

ALERT:

MBS and Treasuries Bounce Weaker as Stocks Stop Sliding

S&P's hit 1135 at their worst this morning and are now back up to 1145. Bond markets followed suit and have risen from 1.97 to 2.06. Fannie 4.0's are down to 104-21 and 3.5's are at 101-28. That brings the price spread between the two MBS coupons EXACTLY back to 2-26, a level we've been discussing for a few days as a tipping point for 3.5 coupons gaining more prominence. We're not sure if lenders are already considering repricing for the worse, but it's a tragic possibility among those who got overly aggressive in response to the rally. But we'd urge you to consider the timing of the initial rate sheet in relation to MBS price movements today and then of course, whether or not you've seen any reprices for the better before any "panic lock."

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "scary little move bouncing now. interesting technical developments on that downtrend mentioned earlier in S&P"

Matthew Graham : "and a little bit down + need for pipeline control = more bad than is justified merely by changes in MBS prices."

Matthew Graham : "Plaza for the worse as well"

Matt Hodges : "i haven't seen it yet, but I'll be sure to tell you"

Jason Wilborn : "did GMAC reprice for the worse"

Matthew Graham : "this morning and yesterday we've seen some of the best rates recently. Lenders had to have been getting crushed with locks yesterday and this AM. so a sharp little correction is a good place to hide while repricing for pipeline control as well"

Matthew Graham : "Plaza: "Heavy Document Upload Volume May Cause Delays

Due to heavy volume, you may experience delays in processing document uploads through PULSE. Please avoid duplicate uploads as this will further delay processing.""

Adam Quinones : "ive been watching S&Ps on longer intervals...it has bounced back and forth between 50% and 62% retrace since Aug 11. ...today it dipped below 1150 for first time since then."

Victor Burek : "now flagstar has taken 1.0 away at 4.25 and below"

Matthew Graham : "AQ. what do you think about downtrend from this AM's pre-tank levels in S&P and the last high?"

Jason York : "plaza for the worse"

Adam Quinones : "im watching 1150 in S&P futures. It is 62% retrace of all-time highs. It is giving us some directional guidance."

Adam Quinones : "BoA worse."

Victor Burek : "flagstar worse again!!!!"

Matthew Graham : "nexbank worse"

Matthew Graham : "lots of little supportive bouncing at 2.10"

Victor Burek : ".3 at higher rates"

Victor Burek : "they took .6 away at 4.1 and beow"

Victor Burek : "flagstar worse"

Adam Quinones : "lack of liquidity Andy."

Andy Pada : "Why would mbs be in the red?"

Andrew Horowitz : "my guess is banks went in and sold positions or some would have been selling their own positions that they recently took out"

Matthew Graham : "RTRS - FITCH: WITHOUT DEBT REDUCTION PLAN US WILL TEST THE BOUNDARIES OF ITS 'AAA' RATING "

Matthew Graham : "RTRS - FITCH: ALTHOUGH US CAN SUSTAIN MORE DEBT THAN OTHER 'AAA' SOVEREIGNS, IT HAS TO DEVELOP A CREDIBLE DEBT REDUCTION PLAN "

Matthew Graham : "RTRS - FITCH: PRE-EMINENCE OF US DOLLAR AS GLOBAL RESERVE CURRENCY MEANS US GOV'T EFFECTIVELY HAS FIRST CALL ON EXCESS GLOBAL SAVINGS, SUPPORTS LOW REAL INTEREST RATES "

Matthew Graham : "RTRS - FITCH: THE DEPTH AND BREADTH OF THE US TREASURY MARKET MEANS THERE IS NO SERIOUS EXPOSURE TO LIQUIDITY RISK "

Matthew Graham : "RTRS - FITCH: US CAN TOLERATE MORE DEBT THAN OTHER 'AAA' SOVEREIGNS "

Matthew Graham : "Auction amounts as-expected"

Matthew Graham : "RTRS- U.S. TREASURY SAYS ESTIMATES $57.367 BLN OF COUPON SECURITIES HELD BY PUBLIC MATURING ON AUG 31 "

Matthew Graham : "RTRS - US TO SELL $35 BLN 2-YR NOTES AUG 23, $35 BLN 5-YR AUG 24, $29 BLN 7-YR AUG 25, TO SETTLE AUG 31 "