MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:01 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:41PM :

NY Minute: Bond Market Correction, but Tame in Context

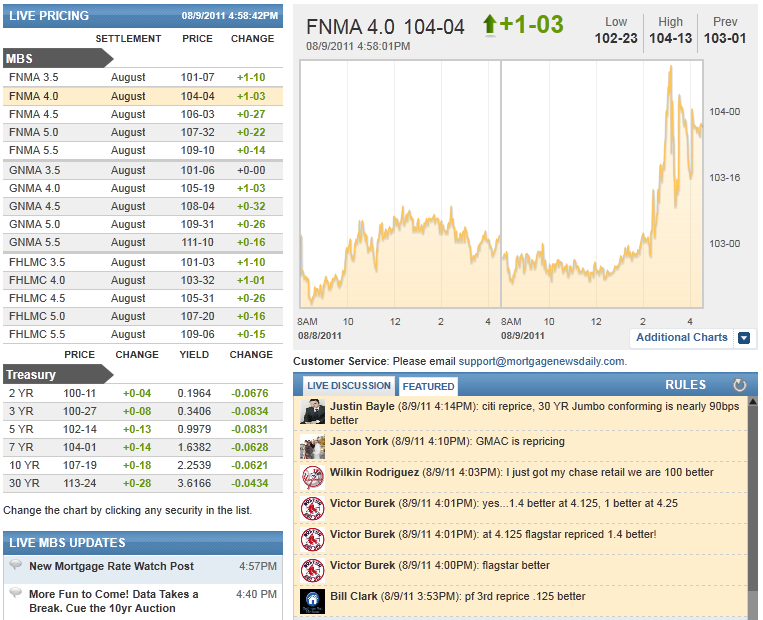

So the 10yr note and the Fannie 4.0 MBS go to the amusement park together. MBS say they're ready to go on an exciting ride. 10yr warns "are you sure you can handle it?" MBS says "no worries, bring it." And so it was that the longer end of the yield curve, hand in hand with the lower end of the MBS stack embarked on the second phase of the post FOMC rally. In fact, earlier in the day, MBS had been outperforming Treasuries. Or to use our amusement park analogy, they'd been more eager to get on the ride and get their thrills. But shortly after "the bounce" came as 10yr notes approached their all time lows, the abruptness of the swing was too much for MBS to handle. MBS like the rally, but not the volatility. Their previous outperformance has eroded as a result, but things are far from bad. While a 10bp losing streak in 10yr notes might be scary on another day, currently, that leaves 10's at 2.1786. Fannie 4.0's are now "only" 1 full point better on the day at 104-01. Reprices for the better have been seen, but please keep in mind not to expect lenders to be able to pass along a proportionate amount of gains until things settle way down.

3:05PM :

ALERT:

Post FOMC Rally Continues, Production MBS Coupons Improve

10yr notes and MBS 4.0 coupons alike were probably a bit awestruck after the FOMC Announcement. Where was the love for them!? Well, the "love" appears to be on the uptick now, except that it's being delivered by trading action in the markets instead of Fed Policy. After all, the FOMC rate decision is very much a concern of the shortest maturity rates. In terms of the 2s/10s curve, that means 2's are the most sensitive to the FOMC. That was abundantly clear as 2's plummeted while 10's expressed a bit of indecision. 4.0's were standing right there with 10's, not really sure what to do. But now, the shape of the yield curve is shifting in the favor of longer duration securities. Reason? The initial reaction (which favored 2's) was to the 2013 date given. But now, the market is reacting to the rest of the statement. To oversimplify: "oh! there's other info in that thing besides the 2013 date? I'll be darned! I guess things are pretty bad..." So now we're seeing 10's catch up with shorter duration parts of the curve. It's an honest to God facemelter.... 10's are 17 bps lower on the day at 2.13, but who the heck knows where they'll be by the time you read this... Fannie 4.0's are up over a point at 104-03. 3.5's are in "soon-to-be-new-production-coupon" territory (would have to STAY at these levels) currently at 100-24. What had been "up in coupon" is now "Down in coupon." Short term opportunism on the 2013 date is now long term panic. Buckle up folks...

2:53PM :

ALERT:

FOMC to World: "Save The Date!" Low Rate Time Frame Now Explicit.

It's pandemonium folks. The Fed knew darn well what they were doing. Not since 1992 have there been 3 dissenters on a vote to approve the text of an FOMC announcement, but that's how controversial today's decision was to lay out a firm timeline on what had previously been "low rates for an extended period." Markets have now been given a date: "mid 2013," making 2yr notes more "cash-like" than they've ever been. From the high 0.2's earlier, 2yr notes plummeted to 0.18. The middle of the curve, especially 5's, dropped even more. The long end of the curve is lagging. That makes sense considering the Fed just guaranteed the short end and said nothing about the long end. Earlier in the reaction phase, the yield curve was noticeably steeper. Higher MBS coupons were outperforming the lower (because higher coupons have shorter durations, so it's like the MBS mimicking the yield curve). There's much more to discuss on the aftermath from this FOMC statement, but for now, just be aware there's a possibility of reprices for the better.

1:26PM :

ALERT:

MBS Rally Following Healthy 3yr Note Auction

If we didn't have an FOMC announcement on the docket the current MBS chart is starting to get that "potential reprices for the better" look about it. We're up about 4 ticks (eighth of a point) to 102-30 since the results of the 3yr note auction came in. The high yield was slightly lower than expected. Demand was just slightly higher than the average of the last 4 auctions and demand from indirect bidders was stellar. 10yr notes are a almost 2bps lower since auction and stocks are fairly flat. Looks like markets are indeed waiting for FOMC, but perhaps with the slightest of bond-market-friendly lead-offs. Some plucky young lender might reprice for the better here, but no guarantees. Additionally, anything can change in a NY minute.

11:24AM :

Investors Increase Treasury Holdings in Latest Survey

(Reuters) - Investors increased their U.S. Treasuries holdings as fear about the European debt crisis and a steep selloff on Wall Street unleashed a stampede for safe haven, a survey showed on Tuesday.

The rush into U.S. government bonds has occurred despite Standard & Poor's stripping of the United States' long-term AAA-rating on concerns over its high indebtedness last Friday.

The share of investors who said on Monday they were long, or holding more Treasuries than their portfolio benchmarks, rose to 11 percent from 6 percent last week, J.P. Morgan Securities said on Tuesday.

In early July, no respondents were long Treasuries, something that had not happened since February 2005.

The surge in Treasuries purchases knocked short-dated U.S. yields to record lows on Monday. For more, see US/

Growing positions in Treasuries bode favorably for this week's August quarterly refunding when the U.S. Treasury Department is scheduled to sell $72 billion coupon-bearing securities.

According to the latest J.P. Morgan survey, the share of investors who were neutral, or owning Treasuries equal to their portfolio benchmarks, was steady at 74 percent.

The share of investors who said they are short on U.S. government debt, or holding fewer Treasuries than their benchmarks, fell to 15 percent, the lowest since April 25.

The net shorts -- the difference between shorts and longs

fell to 4 percent its lowest level since late February. In early Treasuries trading, prices on benchmark 10-year Treasury noteswere down 17/32 for a yield of 2.38 percent, up 6 basis points from late on Monday but down 23 basis points from a week ago.

(Reporting by Richard Leong; Editing by Kenneth Barry)

11:22AM :

ECON: Small Business Optimism Dips Again in July

(Reuters) - Small businesses in the United States grew less optimistic about recovery prospects for a fifth straight month in July, according to the National Federation of Independent Business.

The NFIB's Small Business Optimism Index fell 0.9 point in July to 89.9, largely because of weaker expectations for real sales gains and reduced hope for an improvement in business conditions in the next six months.

William Dunkelberg, chief economist for the small business group, said that aside from concern about future sales, the 1,817 respondents to the survey seemed troubled by other, less easily defined worries.

"The debt ceiling madness" may be acting as a damper on businesses' willingness to hire and invest, Dunkelberg said.

"Twelve percent (seasonally adjusted) reported unfilled job openings, down 3 points, suggesting that the unemployment rate will rise," the survey summary said. Some 50 percent of respondents said their firms had made capital outlays in recent months, unchanged from June and still an historically weak reading, it said.

(Reporting by Glenn Somerville, editing by Neil Stempleman)

11:16AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Bill Clark : "pf 3rd reprice .125 better"

Matthew Graham : "MBS are at prices that have historically coincided with lower rates, but due to the abrupt nature by which we achieved these levels, hedging in the secondary market is currently too costly to come anywhere close to that until things settle down"

Jeff Anderson : "Anyone have any spare dramamein?"

Matthew Graham : "how bout this...."

Thomas Quann : "No, Im sorry, the borrowers are owed more"

Matthew Graham : "now.... if markets think that 2.05 was the bounce, we're about to feel some g-forces"

Ira Selwin : "TQ - all jokes aside you arent "owed" more"

Timothy Baron : "none MG, but borrowers think rates are dropping"

Steve Chizmadia : "No one MG"

Matthew Graham : ""there go locked loans?" who has repriced enough to warrant that?"

Timothy Baron : "true dat"

Ira Selwin : "they are losing a lot right now"

Ira Selwin : "Timothy lenders arent stingy. they are freaking out"

Timothy Baron : "Lenders still stingy for the most part."

Matthew Graham : "2.03+ = all time intraday low for 10's"

John McClellan : "what the heck! have you guys seen the 10 year????!"

Matthew Graham : "all time highs for 4.0's"

Andy Pada : "sure is better"

Scott Valins : "is 104-08 better than last thursday?"

Steve Chizmadia : "wow. we broke 104"

Ken Crute : "like it for the new stuff, hate if for the loans in process "

Tony Cardinal : "Nice"

Ken Crute : "just got a 50bp improvment "

Matthew Graham : "eyes first saw 2013 = rally short end. eyes then read the rest of it = rally long end."

Oliver S. Orlicki : "here come the reprices...FAMC, FPF, SunTrust"

Steve Chizmadia : "Plaza and Stearns better"

Matthew Graham : "there's some more clarity on shift between steepener and flattener"

Justin Bayle : "this is crazy"

Thomas Quann : "DOWN IN COUPON TIME?"

Andrew Horowitz : "can we say 2.00"

Bert Swyers : "we need to find a range and stay there for a minute"

BVG : "yes it's because of that and the explicit wording from Fed that our economy is in the Tank and remaining there."

Jason Sheaffer : "the 30 year is now lower than the 10 year was a few months ago"

Matthew Graham : "reversal of fortune for yield curve"

Jason Sheaffer : "whoa, 2.18 on the 10 year"

Jeff Anderson : "It could be tempered until the Fed, I'm thinking."

Andrew Horowitz : "nah, lets stagnate right here would be better Bert"

Bert Swyers : "let the rally begin"

Matthew Graham : "RTRS - US TREASURY - PRIMARY DEALERS TAKE $13.11 BLN OF 3-YEAR NOTES SALE, INDIRECT $15.33 BLN "

Matthew Graham : "RTRS - U.S. 3-YEAR NOTES BID-TO-COVER RATIO 3.29, NON-COMP BIDS $15.22 MLN "

Matthew Graham : "RTRS - U.S. SELLS $32 BLN 3-YEAR NOTES AT HIGH YIELD 0.500 PCT, AWARDS 29.50 PCT OF BIDS AT HIGH"

Matthew Graham : "and th other teensie weensie little tidbit: this will be the lowest yielding 3yr auction, ever. (11/8/10 at a high yield of .575 and it's all but impossible we'd get that high today)."

Matthew Graham : "Indirect bidders average 34.1% over the last 4"

Matthew Graham : "Last 5 in a row have come in with high yields UNDER the 1pm when-issued yield"

Matthew Graham : "Last 4 auction BTC average = 3.25"

Steve Chizmadia : "T Minus 17 minutes until the auction"

Matthew Graham : "S&P at 1149.62 right now... several big bumps around the 1150 pivot"

Jason Wilborn : "stocks going to go red before end of day"

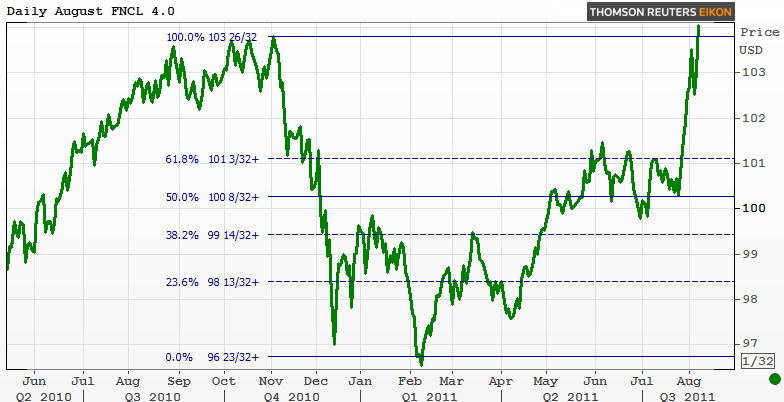

Check out a new record price high in Fannie Mae 4.0 MBS...