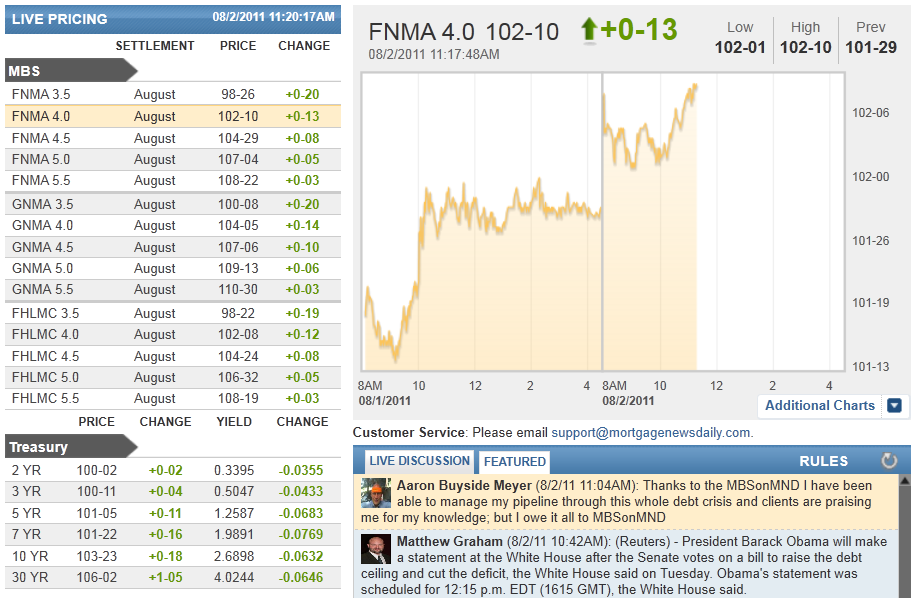

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:02 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:16AM :

SNAPSHOT: Senate to Vote on Debt Deal

(Reuters) - Here is a rundown of the final actions in Congress on Tuesday as lawmakers try to rush a deficit reduction deal to the White House that also will raise the $14.3 trillion limit on U.S. government borrowing, just hours before the deadline to avert an unprecedented default.

* The Democratic-led Senate set to vote on the deal at noon EDT (1600 GMT).

* Senate begins debate on the measure. It is expected to pass.

* Senate action comes after the Republican-led House of Representatives approved it on Monday night on a bipartisan vote of 269-161.

* U.S. Treasury Secretary Timothy Geithner tells ABC News that the contentious battle over the debt limit and the threat of default had damaged confidence in the economy and that credit rating agencies would "take a careful look" at whether U.S. lawmakers have the will to reduce deficits.

* Despite the deal that will increase government borrowing authority through the 2012 presidential election year, Wall Street still worries about a possible downgrade of U.S. credit rating. U.S. stock indices open lower on Tuesday. (Reporting by Donna Smith; editing by Vicki Allen)

9:59AM :

ALERT:

MBS Stronger as EU's Own Debt Crisis Remains a Factor

It's been an uncommon stretch of time in terms of where the markets focus their attention. After having dominated (clearly) for months, EU-related headlines have been surprisingly hard to find during the rise to prominence of our own domestic debt problems. That's fairly logical, but now that the debt ceiling vote moves closer and closer to its ostensible resolution, it's been easier for markets to pay attention to what's going on abroad (again). So as Italy calls emergency talks to deal with political turmoil and a debt/GDP ratio that is outdone only by Greece itself, the flight-to-safety bid returns, plain and simple. 10yr Yields were as low as the 2.67's this morning but have since corrected slowly back up to 2.71+. It will be interesting to see if we get any support from yesterday's low yields (potential "pivot"). Similar story in MBS where Fannie 4.0's made it as 102-05+ this morning and are currently back down to 102-02+, perhaps testing their own pivot (yesterday's highs were 102-00, so we could lose a few more ticks and still use yesterday's ceiling as today's floor). If that happens, there's no major significance other than to say the market was defaulting to rally mode rather than "wait and see" mode. There''s too much uncertainty surrounding the ongoing resolution of the debt vote as well as Friday's NFP to read too much into the technical movements we might see between now and Friday. Whatever the case, things are good for now. Best rates of the year, best MBS prices of the year.

9:14AM :

Fed Confronts Limited Tools to Stir Economy

Federal Reserve officials face two constraints as they prepare for a policy meeting next week amid a dismal economic outlook.

First, inflation is already elevated by many measures and could become more so if the Fed takes new steps to revive the economy. And, second, even if they were convinced they should act, officials don't have tools ideally suited to fix the economy's problems.

The constraints mean the central bank is unlikely for now to embark on a big new program of securities purchases at the Aug. 9 meeting or launch other major initiatives.

"We have to be careful," Charles Plosser, president of the Federal Reserve Bank of Philadelphia, said in an interview. "The notion that we can have a substantial impact on output and employment over the near term is a difficult case to make."

"The possibility remains that the recent economic weakness may prove more persistent than expected and that deflationary risks might re-emerge, implying a need for additional policy support," Fed Chairman Ben Bernanke said last month.

"The FOMC, in my view, may have to define a supportive policy stance that will be held in place for quite a long period while letting what are essentially nonmonetary policy fixes do their work," Dennis Lockhart, president of the Federal Reserve Bank of Atlanta, said in a speech last week. These nonmonetary policies—like balancing the government's budget—could take "a number of years" to work, he noted.

The Fed also could be more explicit about plans for its $2.6 trillion of Treasury and mortgage-backed securities holdings. At some point it will let these holdings dwindle, first by allowing them to mature without reinvesting the proceeds and then by selling them. The Fed could offer clearer assurances that it won't start shrinking the portfolio for a very long time; that could help hold down long-term interest rates.

8:56AM :

Ally Financial Profit Down on Mortgage Loss

(Reuters) - Ally Financial Inc's second-quarter profit declined by 80 percent as the lender's mortgage operations lost money, versus a year-earlier profit.

Ally Financial -- which specializes in car and home loans -- reported on Tuesday net income of $113 million, down from $565 million a year ago.

Ally's mortgage operations reported a $127 million quarterly loss compared with a $230 million profit a year before. (Reporting by Joe Rauch, editing by Gerald E. McCormick)

8:34AM :

ECON: Consumer Spending Declines, First Time in Nearly 2 Years

(Reuters) - U.S. consumer spending unexpectedly fell in June to post the first decline in nearly two years as incomes barely rose, a government report showed, suggesting economic growth could remain subdued in the third quarter.

The Commerce Department said on Tuesday consumer spending slipped 0.2 percent, the first drop since September 2009, after edging up 0.1 percent in May.

Economists polled by Reuters had expected spending, which accounts for about 70 percent of U.S. economic activity, to rise 0.2 percent.

When adjusted for inflation, spending was flat in June after easing 0.1 percent the prior month. The decline came even as gasoline prices retreated from their peak just above $4 a gallon in early May and suggested the much-anticipated bounce back growth in the third quarter would lack vigor.

Consumer spending barely grew in the second quarter, inching up at an annual rate of only 0.1 percent -- the weakest pace since the end of the 2007-09 recession. Spending increased at a 2.1 percent rate in the first quarter.

That contributed to hold the economy to an anemic growth pace of 1.3 percent in the second quarter.

The weak spending in June also reflected tepid income growth after employment growth ground to a near halt in June, with nonfarm payrolls rising only 18,000. Income ticked up 0.1 percent, the smallest increase since November, after rising 0.2 percent in May.

Disposable income ticked up 0.1 percent, also the smallest increase since November. But when adjusted for inflation, disposable income rose 0.3 percent. With real disposable income outpacing spending, savings rose to $620.6 billion from $581.7 billion in May. (Reporting by Lucia Mutikani, Editing by Andrea Ricci)

7:48AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "(Reuters) - President Barack Obama will make a statement at the White House after the Senate votes on a bill to raise the debt ceiling and cut the deficit, the White House said on Tuesday.

Obama's statement was scheduled for 12:15 p.m. EDT (1615 GMT), the White House said. "

Adam Quinones : "fyi: Flagstar let its broker clients know that, "FHA statutory loan limits are expected to decrease on October 1, to pre- Housing and Economic Recovery Act (HERA) limits. Though FHA has not yet published the implementation process, we expect FHA to allow loans to close at today's higher loan limits provided credit approval is issued on or before September 30, 2011. Loan limit changes to our system will be ready to implement when the changes take effect. At this time, we have not determined a cut"

Adam Quinones : "now lock desks are just hoping to see some loans come in the door to balance out their hedge ratios."

Adam Quinones : "cause a lot of desks prob have too much coverage on their pipeline and now need to "peel it off" at higher prices (yikes!)"

Adam Quinones : "eventually you need to buy that back...unfortunately at higher prices. that is why youre seeing extra margin in rate sheets."

Adam Quinones : "when rates fall as fast as they have, hedging models assume that more loan will fall out. that means, if you dont buy back your hedges as prices rise, that you will have too much coverage on your pipeline"

Adam Quinones : "the percentage of MBS hedges they have vs. the desk's expectation for pull-through"

Adam Quinones : "saw about 1bn on screens yesterday...hearing of lock selling this AM as well."

Adam Quinones : "if they didnt get caught with too much coverage...yes."

Steven Bote : "I'd imagine it's a great morning to hedge from the desk side of things, would you deskers agree?"

Matthew Graham : "Take out those volatile, brief spikes higher in yield, and we're right where we were going."

Matthew Graham : "THE BIG LIGHT BULB: It's not "being this low in yield" that is making things seem volatile or overly aggressive... Rather, it's the two brief spikes higher in yield seen recently that ruin the narrow and stable shape of the previously existing rally."

Matthew Graham : "Where we are today is a perfect continuation of that trend, perhaps parabolically "leveling off" as rallies of this pace usually do as they approach likely candidates for resistance."

Matthew Graham : "aka, totally fit with "history repeating""

Matthew Graham : "Same exact trendline that contained the entire 2nd half of 2009 (which, like 2011, also followed a steep rally and abrupt correctional sell-off in bonds)"

Matthew Graham : "so to me, the line on the chart is a logical reaction to all that... medium paced, narrow trading range rally to technical trendline."

Matthew Graham : "Early April, we'd just fought off a move higher in yield, Econ data stopped looking like it was gaining steam, QE2 ending was getting closer, economic detractors were stubbornly present."

Matthew Graham : "This way of thinking doesn't jive for everyone, but when I look at charts, 10yr yields particularly, I see "psychology in motion." It's like an ekg of what the market knows and what it thinks about where it's going"

Matthew Graham : "looking at the beginning of the rally around 4/11 when 10's were near 3.6, things were very linear and very stable."

Matthew Graham : "well there's another way to look at that BB"

Brent Borcherding : "It gets a little scary, seeing this much gain, this quickly. Seems like whatever it is it can't be as bad as what's being baked in the cake."

Chip Harris : "Saw the update about Ally. Not a surprise. They have been a nightmare to deal with ever since the new LO Comp Rules toof effect. I have pretty much stopped sending them business."

Adam Quinones : "gm all. TSYs higher, curve flatter, Euro weaker, stocks down, gold at new record high (again) and MBS lagging. RISK OFF!"

Matthew Graham : "RTRS - PERSONAL SPENDING DECLINE FIRST SINCE SEPT 2009"

Matthew Graham : "RTRS - MKT-BASED YEAR-OVER-YEAR PCE PRICE INDEX +2.7 PCT, CORE +1.4 PCT "

Matthew Graham : "RTRS - PERSONAL SAVING RATE 5.4 PCT VS MAY 5.0 PCT RTRS - MKT-BASED PCE PRICE INDEX -0.1 PCT (MAY +0.2 PCT), CORE +0.2 PCT (MAY +0.3 PCT) "

Matthew Graham : "RTRS - REAL CONSUMER SPENDING 0.0 PCT VS MAY -0.1 PCT (PREV -0.1 PCT) "

Matthew Graham : "RTRS - YEAR-OVER-YEAR PCE PRICE INDEX +2.6 PCT VS MAY +2.6 PCT (PREV +2.5 PCT); CORE +1.3 PCT VS MAY +1.3 PCT (PREV +1.2 PCT) "

Matthew Graham : "RTRS - OVERALL PCE PRICE INDEX -0.2 PCT (-0.1714) VS MAY +0.2 PCT (PREV +0.2 PCT) "

Matthew Graham : "RTRS - CORE PCE PRICE INDEX +0.1 PCT (+0.1129; CONS +0.2 PCT) VS MAY +0.2 PCT (PREV +0.3 PCT) "

Matthew Graham : "RTRS - PERSONAL INCOME +0.1 PCT (CONS +0.2 PCT) VS MAY +0.2 PCT (PREV +0.3 PCT) "

Matthew Graham : "RTRS - US JUNE PERSONAL SPENDING -0.2 PCT (CONSENSUS +0.2 PCT) VS MAY +0.1 PCT (PREV 0.0 PCT) "