MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:00 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

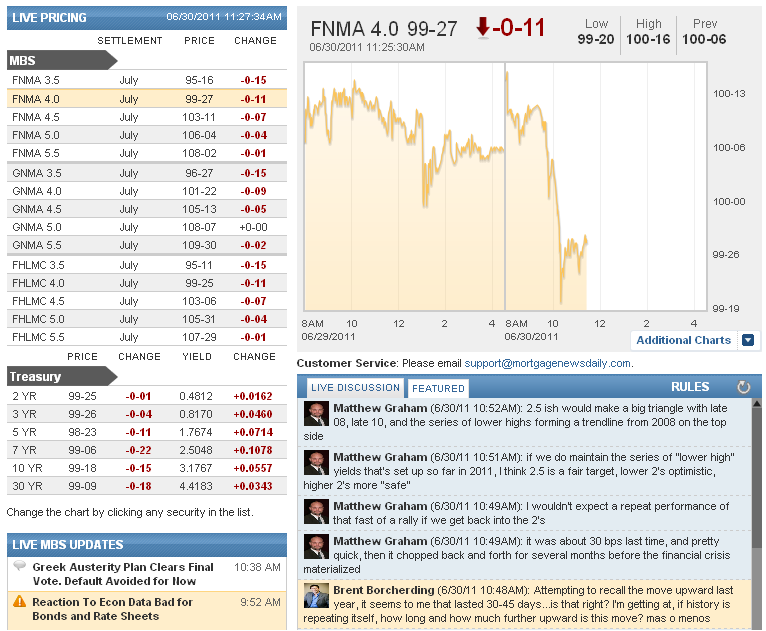

11:28AM : Technical Breakdown Prompts Rapid Sell-Off

If you're watching charts, this is old news to you. We're just talking

about the technical breakdown in 10yr Treasuries right now, not because

they dictate mortgage rates, but because the overall "bond market" has

been volatile and operating near longer term inflection points that

speak to potential "shifts." In times like these, the value of

analyzing MBS charts greatly decreases and underlying benchmarks become

much more important. What we're seeing happen this morning is a bond

market that came into the day as close to "on the edge" of the recent

range as it could be. That was marked by 3.10 in 10yr notes, which was

actually broken yesterday, but would need trading action today to

actually confirm or reject the breakout. Long story short, the breakout

has now been confirmed after looking indecisive leading up to 9:45am

Chicago PMI data. After that, the snowball began. Volume ramped up,

and yields moved sharply 10bps higher to 3.20. That was the next major

technical level for 10yr yields, and in terms of "history repeating

itself" is an analogous level to how things happened in 2010. If

history continues repeating, more volatility is in store--BIG swings.

But even before assessing that possibility, we can at least observe

today that 3.20 has held as a supportive ceiling for 10yr yields,

effectively stopping the bleeding. It could break again in coming hours

or days, but for now, insane volume and a healthy bounce back down to

3.17 suggest that the bond market has pulled into the "pit lane" between

sub-3.10 trading and greater-than-3.20% trading. Tomorrow's economic

data may help inform a break away from this middle ground, either

helping bonds get "back in the race," or retire and head to higher

yields. The translation to MBS hasn't been unusually awful so far with

4.0's down just under three eighths (11/32nds) to 99-27. If you had

rates well before 9:45am Eastern, reprices remain a risk. If you don't

have them yet, expect a big cut to rebate.

10:38AM :

Greek Austerity Plan Clears Final Vote. Default Avoided for Now

(Reuters) - The Greek parliament approved detailed austerity and privatization bills on Thursday in a crucial vote to secure emergency funds and avert imminent bankruptcy, but longer-term dangers still lurk. Prime Minister George Papandreou secured a majority for the legislation after lawmakers backed a 28 billion five-year euro austerity plan on Wednesday, clearing the last obstacle to the next slice of aid from the European Union and the International Monetary Fund. Belgian Finance Minister Didier Reynders said euro zone finance ministers were likely to agree as a result to release a next tranche of loans to Greece at a meeting on Sunday. The IMF is set to follow suit on July 5. That 12 billion euro loan will prevent Greece defaulting in mid-July or at the latest on August 20, when it must honor a big bond redemption, and shift the focus to a second assistance package likely to be about the same size as last year's 110 billion euro bailout. But credit insurance markets are still pricing in an 80 percent chance of Greece defaulting on its 340 billion euro debt mountain -- 150 percent of annual economic output -- within five years, and a likely 40 percent write-down for bondholders on three-year debt. Prime Minister George Papandreou's socialist government may find it hard to enforce tax increases and state asset sales against massive public resistance, while a violent fringe always present in Greek politics has burst to the fore. Vasso Papandreou, a former European Commissioner and rebel member of the prime minister's PASOK party who is not related to him, told parliament she would vote for the laws as a patriotic duty even though she believed the economy would deteriorate as a result.

9:52AM :

ALERT:

Reaction To Econ Data Bad for Bonds and Rate Sheets

Following the better-than-expected results on the Chicago Purchasing Manager's Index, 10yr benchmarks have risen to their highest yields in over a month, and Fannie Mae 4.0 MBS have fallen an immediate 6/32nds, bringing them into negative territory for the day. If you already had rate sheets this morning, this may mean a reprice for the worse is on the way shortly. Otherwise, it changes the likelihood of slightly improved initial rate sheets to slightly worse.

9:48AM :

ECON: Chicago PMI Beats Consensus

(Reuters) - Business activity in the U.S. Midwest grew more than expected this month, helped by a jump new orders, a report showed on Thursday.

The Institute for Supply Management-Chicago business barometer rose to 61.1 in June, The reading was 56.6 in May and economists had forecast a June reading of 54.

The employment component of the index slipped to 58.7, from 60.8 in May, but new orders surged, to 61.2, from 53.5. A reading above 50 indicates expansion in the regional economy. (Reporting by Ann Saphir; Editing by James Dalgleish)

9:28AM :

JPMorgan Strikes Deal on Mortgage CDO Case

(Reuters) - A federal judge on Wednesday approved a $153.6 million settlement between JPMorgan Chase & Co and the top U.S. market regulator over allegations a mortgage CDO product defrauded the bank's investors at the time of the housing market collapse. The U.S. Securities and Exchange Commission and the second-largest U.S. bank announced the settlement on June 21 of civil charges over JPMorgan's collateralized debt obligation (CDO) marketed as Squared CDO 2007-1. The settlement was approved at a hearing in New York by U.S. District Judge Richard Berman, who described it as "another important step for the financial industry and the SEC in righting the wrongs of the recent financial crisis." The settlement echoes on a smaller scale the $550 million accord that Goldman Sachs Group Inc reached last July over its Abacus collateralized debt obligation. Both cases involved charges that banks let hedge fund clients structure complex securities -- and then bet against them -- without disclosing their involvement to investors. John Savarese, a lawyer for JPMorgan Chase & Co said the matter had been "thoroughly investigated" and the parties had reached "a fair and reasonable agreement." JPMorgan sold $150 million of Squared CDO notes to pension funds and investors worldwide that lost most of their value in just 10 months, the SEC said.

8:57AM :

MBS Fall After Jobless Claims, Now Holding Ground

Fannie Mae 4.0 MBS are up 4/32nds at 100-10. They briefly traded as high as 100-15+ this morning, but that proved fleeting. 10yr notes are also improved on the day. Yields are down .0259 to 3.095. This is an important level as it lies within the boundaries of their recent range, and holding here would effectively be a rejection of the breakout suggested with yesterday's sell-off. But even if 10's are able to hold under 3.10 today, that would do little to change the near-term likelihood of volatility. Based on the morning's MBS improvements, lenders should generally be coming out with improved rate sheet offerings, but expect more defensiveness than generosity in the volatile environment.

8:44AM :

Fannie's Monthly Summary Shows Falling Delinquencies

In the latest monthly summary released by Fannie Mae, the single-family serious delinquency rate fell 5bps to 4.14 pct, after having fallen 8bps in the April report. The report, covering May, showed a similar 5bps fall in multi-family delinquencies to 0.52 pct. Fannie also reported the completion of 16,419 loan modifications in May bringing the 2011 total to 84,133.

8:35AM :

ECON: Jobless Claims Barely Move. Higher than Forecast

(Reuters) - New U.S. claims for unemployment benefits fell less than expected last week, a government report showed on Thursday, suggesting the labor market was struggling to regain momentum.

Initial claims for state unemployment benefits edged down 1,000 to a seasonally adjusted 428,000, the Labor Department said.

Economists polled by Reuters had forecast claims dropping to 420,000. The prior week's figure was unrevised at 429,000.

It was the 12th straight week that claims have been above 400,000, a level that is usually associated with a stable labor market. Employment stumbled badly in May, with employers adding just 54,000 jobs -- the fewest in eight months.

Nonfarm payrolls are expected to have increased 90,000 this month, according to a Reuters survey, with the unemployment rate edging down to 9.0 percent. The employment report for June will be released on July 8.

(Reporting by Lucia Mutikani; Editing by Neil Stempleman)

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "yeah, rate sheets are another story... "

Adam Quinones : "(id be concerned if convexity sellers surface)"

Matthew Graham : "10's could easily get there without altering the bigger picture"

Matthew Graham : "Might seem overly bearish or scary, but I'd only be really concerned with a break above 3.20"

Adam Quinones : "rates are overbought, path of least resistance = higher."

Adam Quinones : "right now I think we need to focus on techs."

Matthew Graham : "however, if they don't, the choppiness is in line with historical precedent."

Andrew Horowitz : "it appears they are just looking at the headline and not digging into the report"

Matthew Graham : "yeah...."

Adam Quinones : "hopefully others see those comments soon..."

Matthew Graham : "Joseph, specifically, note AQ's highlight of one of the report's respondents below: "Producing ahead to avoid know future contract price increases. Chemicals market still shows volatility with no end in sight.""

Matthew Graham : "AQ, so far, the stuff you pointed out is the best "find" in the internals, and the best example of an analyst looking past the headline. I was kinda dismayed reading bandwagony comments on Breakingviews just now..."

Joseph Watts : "Why make it if no one is buying it?"

Andrew Horowitz : "Make it now and store it on shelves"

Matthew Graham : "RTRS- BULLARD - EFFECTS OF FED ASSET PURCHASES ON REAL ECONOMY HARDER TO ASSESS BECAUSE OF SHOCKS TO ECONOMY IN EARLY 2011 "

Matthew Graham : "RTRS- BULLARD - FINANCIAL MARKET EFFECTS OF FED'S QE2 WERE SAME AS IF FED HAD REDUCED POLICY RATE SUBSTANTIALLY "

Matthew Graham : "RTRS- BULLARD - FED ASSET BUYING AT LONGER MATURITIES CAN SUBSTITUTE FOR ORDINARY MONETARY POLICY WHEN INTEREST RATES ARE NEAR ZERO "

Andrew Horowitz : "from the quotes you just posted they are MFG goods in hopes that the orders will come in"

Matthew Graham : "RTRS - FED'S BULLARD - EFFECTS OF QUANTITATIVE EASING ON ECONOMY WILL LAG BY SIX TO 12 MONTHS "

Scott Valins : "based on the rip up in yields its clear that the path of least resistance is higher"

Adam Quinones : ""Suppliers continue to have trouble finding skilled workers. The recession, the "recovery," and the disappearance of industrial arts in our schools seem to have diminished a formerly strong labor pool""

Matthew Graham : "to quantify the volume comment, we've seen the strongest 10-minute chunks of time with between 90k and 100k contracts in the past 2 weeks. the 10 minutes following PMI was just over 90k, basically on par with other fast-paced post-econ-data 10 min blocks"

Adam Quinones : ""There may be a little softening coming but its too early to tell.""

Adam Quinones : ""Producing ahead to avoid know future contract price increases. Chemicals market still shows volatility with no end in sight.""

Adam Quinones : ""Incoming orders have definitely slowed down. Several orders we expected to see are currently on hold. Hopefully something will break or the 4th quarter is going to look sad.""

Adam Quinones : ""Material inflation, Steel and Aluminum, still impacting cost. Weak housing and commercial construction hurting overall business""

Adam Quinones : "General Comments from Members of the Survey Panel..."

Andrew Horowitz : "the "hope" is that it implies a second half pickup"

Andrew Horowitz : "SV it stopped the downward trend in all of the MFG numbers"

Scott Valins : "ok so just clarifying that this beat estimates but why would this imply a 2nd half pickup? it's still worse than most first half #s"

Adam Quinones : "rates traders wont like this report. It bucks the trend on manufacturing weakness and implies the Fed was right when they said to expect a 2nd half pickup."

Matthew Graham : "RTRS- CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX AT LOWEST SINCE NOVEMBER 2010 "

Matthew Graham : "RTRS - CHICAGO PURCHASING MANAGEMENT PRODUCTION INDEX 66.9 IN JUNE VS 56.0 IN MAY "

Matthew Graham : "RTRS - CHICAGO PMI EMPLOYMENT INDEX 58.7 IN JUNE VS 60.8 IN MAY "

John Rodgers : "that is a hot number"

Matthew Graham : "RTRS- CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX 70.5 IN JUNE VS 78.6 IN MAY "

Matthew Graham : "RTRS- CHICAGO PURCHASING MGMT NEW ORDERS INDEX 61.2 IN JUNE VS 53.5 IN MAY "

Matthew Graham : "RTRS - CHICAGO PURCHASING MANAGEMENT INDEX 61.1 IN JUNE (CONSENSUS 54.0) VS 56.6 IN MAY "

Adam Quinones : "Chicago PMI reports on June data...this is a chance for econ developments to move the market..."

Matthew Graham : "waiting to see how domestic stock open goes"

Matthew Graham : "4th time at 3.088 so far this am. seems like they want to try to break lower"

Adam Quinones : "10s are crossing back and forth over 3.10% since Japan opened at 8pm last night."

John Rodgers : "from GMAC (Ally) I will send another email with several general correspondent updates under separate cover; however, please find the pricing changes effective yesterday 6/29 for your information.

• Conv 30Y – 5-10 bps (no change to 20Y)

• Conv 15Y – 15-30 bps (no change to 10Y)

• Govt 30Y – 5-55 bps (there will also be a price improvement on FICO >=700 of 25 bps implemented 6/30)

"

Matthew Graham : "I'm not sure they could express any more indecision"

Matthew Graham : "but at least supported by yesterday's closing levels."

Matthew Graham : "10's blocked by opening levels so far'"

Adam Quinones : "Open interest has fallen in both the 10yr futures contract and S&P futures this week.Lower open interest in TY tells us there's been liquidative position squaring of longs, but limited new position adding. A similar story can be told in stocks. Falling open interest into higher prices implies short covering has led the rally, not new position adding. This makes sense as stocks have trended lower since April and bonds have rallied for 2 of 3 months in the quarter. This week's price action stinks "

Matthew Graham : "RTRS- US INSURED UNEMPLOYMENT RATE FELL TO 2.9 PCT JUNE 18 WEEK FROM 3.0 PCT PRIOR WEEK (PREV 2.9 PCT) "

Matthew Graham : "RTRS- US CONTINUED CLAIMS FELL TO 3.702 MLN (CON. 3.690 MLN) JUNE 18 WEEK FROM 3.714 MLN PRIOR WEEK (PREV 3.697 MLN) "

Matthew Graham : "RTRS- US JOBLESS CLAIMS 4-WK AVG ROSE TO 426,750 JUNE 25 WEEK FROM 426,250 PRIOR WEEK (PREVIOUS 426,250) "