Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the

MBSonMND Dashboard

.

EXTRA PERSPECTIVE: We've been here before. Quite

recently. Remember? Something similar to this "event" played out two-weeks ago (June 14th). A few days after setting YTD rate lows,

loan pricing

decided to throw up on itself because mortgage rates failed to commit to

a sustained rally (we called it pouting). This happened on a day

when stocks managed to put together a healthy recovery rally, despite

weak economic data (bond friendly data). Sounds a lot like today doesn't

it? If you're

not sure, the answer to that question is yes. What happened today was

very similar to what happened two-weeks ago. And the market corrected

shortly there-after. That provides some warmth after the beating we

took place today but it doesn't mean the market will surely behave the

same way it did two-weeks ago. Short-term floaters have much to

lose too (gain in monthly payment), especially for higher loan amounts.

We just

set new YTD rate lows and now we're teetering on a shift higher in

Best Execution Mortgage Rate quotes. Don't lose your current rate

quote here. For long-term floaters, we're

not ready to ring the alarm bell just yet.

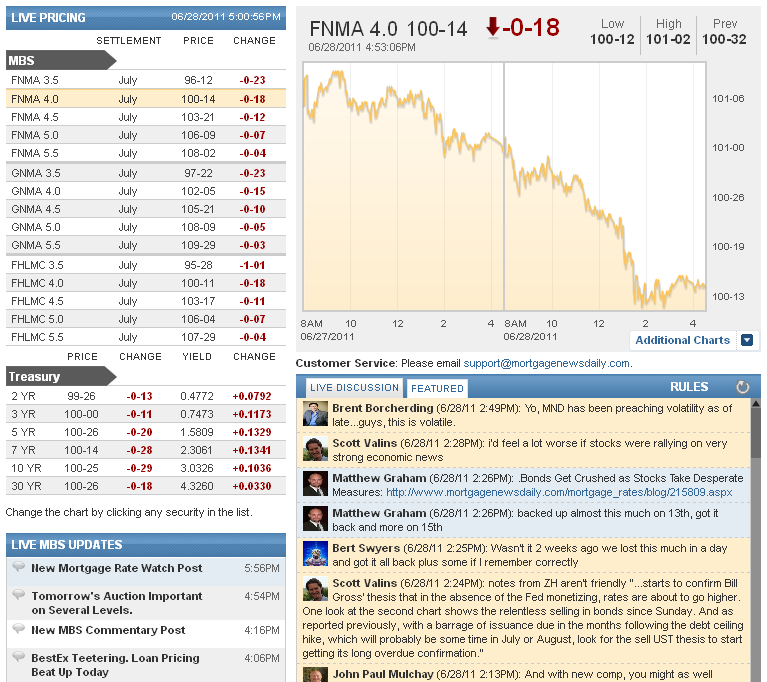

4:06PM : BestEx Teetering. Loan Pricing Beat Up Today

Although MBS coupons outperformed their benchmark guidance givers, it was a bad day in the bond market. The Fannie Mae 4.0 MBS coupon is heading into the close 17/32 lower at 100-15.... 19/32 below the morning price high of 101-02. These steep intraday price declines forced most lenders to reprice for the worse. Taking a closer look at rate sheets, among the five major lenders, rebate is now 49.6bps worse than it was yesterday afternoon. These deteriorations are large enough to say C30 Best Execution has moved from 4.50% to 4.625%, but we'll refrain from confirming that until tomorrow when investors have a chance to digest what went down today.

3:33PM :

Small Lenders Seek to Balance Reform Anxieties

(Reuters) - U.S. lenders and community bankers sounded the alarm to lawmakers on Tuesday over proposed federal rules aimed at reducing risk-taking on mortgage lending, saying the guidelines could hurt small banks and impair credit markets. The rules -- mandated by the passage of the Dodd-Frank Wall Street overhaul bill -- are under consideration by regulators to establish guidelines for originators of securitized loans, the types of instruments that are blamed for fueling the 2007-2009 financial crisis. Regulators intend to reduce risk-taking by forcing lenders to hold a 5 percent stake in any debt instrument pooled in the secondary market. "Should this proposal be adopted, it will surely drive many banks from mortgage lending and shut many borrowers out of the credit market entirely," Christopher Dunn, chief operating officer of South Shore Savings Bank in South Weymouth, Massachusetts, told a Senate Banking Committee hearing on behalf of the American Bankers Association.

The current guidelines "fly in the face of workable and clear standards," he said. This type of "regulatory burden is significant" to smaller institutions, and will impair access to credit for consumers.

The law created an exemption for mortgages deemed to be safe enough and gave regulators the task to define such suitable loans. Regulators proposed an exemption for the so-called qualified residential mortgages when borrowers make 20 percent down payments. A comment period on the proposed rule expires on August 1. "We have to come up with an appropriate balance," said Senator Jack Reed, a Rhode Island Democrat, during the hearing. "If you don't have any of these rules of the road, you get exactly what we had -- which was gaming and no money down."

3:18PM :

Builders: Lower Loan Limits to Slow Housing Recovery

A drop in some mortgage loan limits for the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac and the Federal Housing Administration scheduled to occur on Oct. 1 will reduce housing demand and place downward pressure on home prices in major housing markets, according to a new study from the Economics and Housing Policy Group at the National Association of Home Builders (NAHB). The size of "conforming" mortgages for the GSEs is currently limited to $417,000 in general, but that ceiling can rise to as high as $729,750 using a statutory formula based on local median home prices. Unless Congress acts to extend these levels, they will revert to the lower permanent criteria for high-cost areas under the Housing and Economic Recovery Act of 2008. The base limit will remain at $417,000, but the formula for establishing limits for high-cost areas will change from 125 percent to 115 percent of the area median home price, and the national ceiling will drop from $729,750 to $625,500. Looking at limits published by the FHFA, 204 counties — or 6.5% of the 3,143 counties in the U.S. — will see a decrease in their high-cost conforming loan limit. These counties represent relatively dense concentrations of population and housing and contain 20.7 million owner-occupied units out of the 75.3 million nationwide, or 27%.The downward pressure on prices could extend beyond the homes directly affected by the lower limits, the study warns, because first-time and trade-up home sales are interrelated. Purchasing homes that go above the GSE ceiling will require non-conforming loans that currently have been about 60 basis points (0.6 percentage points) higher than conforming loans, the study finds, and based on a report by the Federal Housing Finance Agency (FHFA) the non-conforming mortgages are expected to be 50 to 75 basis points higher.

3:09PM :

Mortgage Fraud Up 31% in First Quarter 2011; FCEN Says

(WSJ) - Banks are scouring their files for shady loans made during the housing boom, and that’s caused the number of mortgage fraud reports filed with the government to rise 31% in the first three months of this year, according to a report released Tuesday. The Financial Crimes Enforcement Network, a Treasury Department agency, reported 25,485 “suspicious activity reports” related to suspected mortgage fraud in the January-March period. That was up from 19,420 in the same quarter a year earlier. The increase was attributed to large mortgage servicers performing thorough reviews of loan files after receiving demands from mortgage investors to repurchase mortgages that have fallen into default. In January, Bank of America agreed to pay Fannie Mae and Freddie Mac $2.8 billion to cover bad mortgages the government-controlled companies agencies purchased from the bank’s Countrywide Financial mortgage unit. Repurchase requests covered in the fraud report mostly involve activity that occurred in 2006 and 2007, James H. Freis Jr., FinCEN’s director, said in a statement. In the January-March period, 86% of mortgage-fraud reports involved activities that occurred more than two years ago. “The industry is slowly making its way through the most problematic mortgages,” Freis said. Fannie and Freddie and other mortgage investors have been trying to recoup losses by forcing banks to buy back loans in which borrowers or lenders made fraudulent statements when the loans were made. The report also noted that fraud is occurring among newer loans. For example, the report identified instances in which foreclosed properties are sold at an artificially low price to a straw buyer, who turns around to sell the property for a quick profit, the report said.

2:06PM :

Auction Recap: Apathy Obvious in Low Number of Bids

Treasury just completed its second coupon auction of the week with a sale of $35 billion 5yr notes. Just like yesterday's 2-year note offering, this fundraiser was sloppy. The bid-to-cover ratio came in at 2.59 bids submitted for every 1 accepted by Treasury. Not only is that well below the 2.88-to-1 auction average, it's the lowest bid-to-cover ratio since last June. Apathetic buyer demand also reared its ugly head in the low price/high-yield produced by bidders, which came in 2.3bps above the 1pm "When Issued" yield. When combined with weak bid-to-cover numbers, these two metrics imply investors allowed a price concession to build, but never got aggressive once costs fell (lack of demand). That sentiment can be seen in the buyer breakdown too. The street (dealers) added $18.2bn in new 5yr note inventory or 52% of the competitive bid. Putting over 50% of the issue on dealer books is never a good thing. Making matters worse, dealers only tendered $64bn in bids. That is the smallest bid the street has supplied 5s since December 2010. So dealers picked up more debt than they bargained for...which could put pressure on the market if rates don't rally in the near future. Indirect bidders were in the same boat. They bid on a below average amount of 5s ($14.7bn) and were awarded more than they wanted ($13.1). That explains why the high-yield tailed the 1pm "When Issued" yield by 2.3bps. Directs were pretty close to average on the whole, just like yesterday. No shockers there. That makes two poorly attended auctions in a row now. While this is a nerve racking development, our view is weak auction demand reflects the fact that benchmarks were at their lowest yields of the year beforehand and the 2nd quarter is about to come to an end, as is the Fed's 2nd Quantitative Easing program. Without a confirmed sell-off in stocks, there is little motivation to "make a move" here. Investors would rather remain nimble as they await new tapebombs in the ongoing EU debt drama.

1:12PM :

ALERT:

Reprices for Worse Likely After Poor Treasury Auction

Reprices for the worse appear imminent after a poorly bid 5-year note auction at 1pm. The Fannie Mae 4.0 MBS coupon is currently -15/32 at 100-17. This is 3/32 below our 100-20 reprice target and 17/32 off the intraday high. While some lenders may wait for price action to stabilize in the bond market, others will not be willing to take a chance. We would be recalling and repricing for the worse if it were our desk.

12:00PM :

ALERT:

Negative Reprice Threat: Some Lenders Prepared. Others Didn't

Time for more good news/bad news. The bad news is "rate sheet influential" MBS coupons have fallen to new intraday price lows. The Fannie Mae 4.0 coupon is currently -9/32 at 100-23. The good news is major lenders seem to have already accounted for extra price weakness in their first release of rate sheets by adding a cushion. Based on our data, loan pricing is 28.8bps worse on average today with the largest rebate reductions seen in note rates below 4.75% (loans used to fill 4.0 MBS trades). With rate sheets already reflecting a 9/32 MBS price decline, broad-based reprices for the worse won't be likely without further MBS price declines, at least from the five major lenders (Wells, BoA, JPM, Citi, GMAC). If it were up to us, we wouldn't recall and reissue for the worse until the Fannie Mae 4.0 coupon dips under 100-20 support. That doesn't mean some of the trigger happy lock desks won't reprice for the worse sooner though, especially if their rate sheets were relatively flat this morning. If you think your pricing falls into that category, beware, we're in negative reprice territory already.

11:16AM :

New MBS Commentary Post

11:11AM :

Auction Concession and Stock Lever Hurt Bonds

We've had some developments since Consumer Confidence data flashed just before 10AM (it came out early). At 1287, S&P futures are at their best level since last Wednesday while the 10-year Treasury note is at its weakest level since last Thursday. 10s are currently -7/32 at 101-14 yielding 2.954% (+2.5bps). There is one positive tidbit to share though, mortgages are still outperforming benchmarks. The Fannie Mae 4.0 MBS coupon is -3/32 at 100-29 after falling as far as 100-26 following the release of Consumer Confidence data. The stock lever is clearly putting pressure on the bond market, but rates aren't really fighting back as they have more recently, not with two more auctions to go today and tomorrow. Indeed the concentration of weakness in the bond market is indicative of an auction concession. Soon to be sold 5 and 7-year notes are the worst performers, backing up 4.4 and 3.9bps respectively. Plus the yield curve is steeper as auction supply is focused on the front-end. And mortgages are generally holding steady as short-sellers attack the belly of benchmarks. This tells us price action is likely short-term in nature (tactical auction concession), but also reminds us of the pending potential for price volatility where news headlines dictate directionality and determine a new bias in the broader marketplace. Our next major support level in 10s is 3.00%. There are several less influential inflections in between, but 3.00% is a level we don't want to break.

Featured Market Discussion

Matthew Graham : "plaza Reprice"

Brent Borcherding : "Yo, MND has been preaching volatility as of late...guys, this is volatile."

Matthew Graham : "nexbank reprice"

Scott Valins : "i'd feel a lot worse if stocks were rallying on very strong economic news"

Matthew Graham : ".Bonds Get Crushed as Stocks Take Desperate Measures: http://www.mortgagenewsdaily.com/mortgage_rates/blog/215809.aspx"

Matthew Graham : "backed up almost this much on 13th, got it back and more on 15th"

Bert Swyers : "Wasn't it 2 weeks ago we lost this much in a day and got it all back plus some if I remember correctly "

Scott Valins : "notes from ZH aren't friendly "...starts to confirm Bill Gross' thesis that in the absence of the Fed monetizing, rates are about to go higher. One look at the second chart shows the relentless selling in bonds since Sunday. And as reported previously, with a barrage of issuance due in the months following the debt ceiling hike, which will probably be some time in July or August, look for the sell UST thesis to start getting its long overdue confirmation.""

John Paul Mulchay : "And with new comp, you might as well consider it some solid philanthropy. "

John Paul Mulchay : "SPS, SLS. Citi actually agreed to one as well but couldn't qualify the client. "

John Paul Mulchay : "The process is more like a short sale to oneself. Existin servicer agrees to current value with no deficiency or further obligation. Then originate a new FHA loan with a new lender. Existing takes that as payment in full. Small servicers are most likely to do it. Challenge is the negotiation with the current servicer to get the agreement. "

Scott Valins : "meaning the lender who agreed to reduce the principal"

Scott Valins : "JPM what lender who held the loan being refi'd have you seen participate?"

John Paul Mulchay : "It's a long haul"

John Paul Mulchay : "Jim, I have done them. Freedom was who I used but not sure if they still will do it. Flagstar would be 2nd choice. If your rep sounds confused have him go to UW because they will do it. "

Michael Stark : "Hey Matt - regarding the ? about short refi's Wasn't there a report out that said less than a dozen had ever been completed nationwide? Kind of a ghost program... I can tell you technically - Wells retail does them - it is in our guides but haven't done one yet."

Matthew Graham : "FYI, Fed's Fisher is speaking currently, and soundbytes are trickling in. So far, he's focused generally on broad economic outlook, saying the economy should be much stronger in the second half of the year versus the first half and that growth of 4 pct would not be unimaginable."

Matthew Graham : "getting into some shorter term supportive territory in 10yr yields right now, just overhead 3.4-3.6, could be some noise or even a supportive event that prevents or delays a back up to the actual limits of the range"

Adam Dahill : "MND saved me a lot of $$$ today. You guys rock"

Matthew Graham : "2.9 to 2.85 on the low end, cases for both depending on whether you want to looks at it horizontally or as a moving target"

Matthew Graham : "call it 3.10 to make it easy"

Matthew Graham : "indeed"

Andy Pada : "so were home on the range? "

Matthew Graham : "100-13 on 6/21 for MBS"

Matthew Graham : "3.097 on 6/14 Andy"

Andy Pada : "Weren't we here last week?"

Adam Quinones : "RTRS - IMF BOARD SELECTS FRANCE'S CHRISTINE LAGARDE AS NEW IMF MANAGING DIRECTOR "

Victor Burek : "flagstar worse"

Bert Swyers : "Boa worse"

Michael Tadros : "PF worse .125"

Michael Tadros : "Direct Mortgage worse"

Michael Tadros : "Interbank worse. 375"

Bert Swyers : "Wells worse "

Jason York : "plaza for the worse"

Adam Quinones : "indirect tenders fell HARD in yesterday's 2-yr note offering."

Matthew Graham : "another problem here is that indirect participation had been steadily increasing in recent 5yr auctions, then took a big enough step back today to mean something"

Adam Quinones : "first thing I noticed was weak tenders from dealers and indirects...the same thing happened yesterday "

Matthew Graham : "last auction 3.20, this one 2.59. yuck."

Matthew Graham : "bad news, but thanks"

Victor Burek : "rut roh"

Matthew Graham : "2.59 BTC"

Matthew Graham : "1.615 high yield"

Matthew Graham : "it's been about a minute late on average this year"

Matthew Graham : "i'll post it in chat as soon as it hits"

Victor Burek : "5yr"

Scott Valins : "what auction is today?"

Adam Quinones : "which makes sense...why not let the concession build up. stocks are going along with it too..."

Adam Quinones : "right now it's a drift higher in slow trading activity. liquidity is lacking. there has been limited push-back against the meandering move ahead of the auctions."

Christopher Stevens : "is this serious profit taking or a legit move up"

Adam Quinones : "a feeling of apathy is still in the air. seeing no push-back against recent sell-off in TSYs."