MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:03 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:57PM :

The Week Ahead: Fed Meeting and EU Summit

Indecisive attitudes carry over into next week where two major events are seen shaping investor outlooks. In the U.S., the Federal Reserve will conclude a two-day policy meeting on Wednesday with the release of the FOMC Statement. We expect the Fed to confirm an end to QEII and indicate that further quantitative easing measures are totally dependent on new economic data developments. The Fed's current stance is that economic growth will pick-up in the 2nd half of the year. Also on our radar is the outside chance that Fed officials will mention an inflationary target, but we really don't anticipate much shift in their overall rhetoric. The other market moving event on the horizon is the European Union Summit, where among other things EU leadership will debate another Greek bailout package or the idea of modifying the current rescue plan. Germany is seen as the primary resistance in finally putting an end to this year long drama. The main mission of the ECB is to avoid a "credit event" where Greece would be considered in default. Other than that the economic calendar is pretty thin with no events on Monday and only Existing Home Sales on Tuesday. The schedule goes quiet again on Wednesday with only the Fed at 2:15. Then on Thursday we get a regional business activity index (we got two bad updates this week) plus Jobless Claims and New Home Sales. The week wraps up on Friday with Final Q1 GDP and Durable Goods Orders. The bond market is stuck in "wait and see" mode as stocks teeter on a major technical collapse. Trading strategies are very short-term in nature as investors are waiting for new directional guidance. Next week certainly offers the potential for headline drive price volatility....

2:36PM :

Greece to Pass Austerity Plan, With Changes

(Reuters) - Greece will seek approval from euro zone finance ministers on Sunday to agree to some changes in a mid-term austerity plan that parliament is expected to pass, the country's new finance minister said on Friday.

"The midterm plan is the passport for reliability not only for the fifth tranche but for the problem of the viability of the public debt," Evangelos Venizelos told Mega TV channel after he was appointed in a cabinet reshuffle.

"The mid-term plan will have to be voted with improvements that have already been made in committee. And those that have already passed (in committee) must be agreed officially with our partners." (Reporting by Harry Papachristou and Angeliki Koutantou)

2:15PM :

Payrolls Down in Many States, but so is Jobless Rate

(Reuters) - The number of people on companies' payrolls shrank in more than half the U.S. states in May, even though the jobless rates in many places continued to improve, Labor Department data released on Friday showed.

The number of employees working for businesses outside of farming decreased in 27 states and Washington, D.C., while it increased in 22 states.

The largest drop in payrolls was in California, which shed 29,200 jobs, followed by New York with 24,700 jobs, and Pennsylvania with 14,200.

In contrast, the largest increase was in Florida, which gained 28,000 jobs, followed by Ohio with 12,000, and Arizona and Louisiana with 10,100 jobs each.

According to the report, the jobless rates in 43 states and the District of Columbia dropped from May 2010, and rose in only four.

In May, the unemployment rates in 24 states fell from the previous month, while those in 13 states and the District rose.

National employment numbers released earlier this month cast a shadow on the country's economic recovery. U.S. nonfarm payrolls increased a slight 54,000 in May and the country's unemployment rate rose to 9.1 percent from April's 9 percent.

Data at the state level is collected by slightly different methods from the numbers drawn for the national report.

2:05PM :

MBS Retreat to Equivocal Range as Volume Dies Down

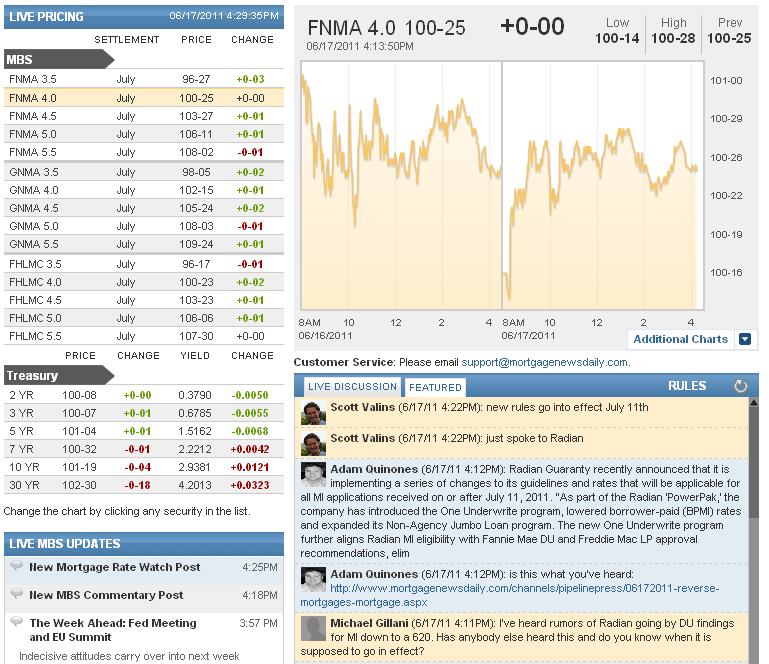

Volume is average today, but low in the context of the last 3 sessions (1.5 mil, 1.9 mil, 1.8 mil, and then today with just over 900k so far), and it's getting lower now, in that characteristic post-lunch-time-on-a-Friday sort of way. MBS and Treasuries both gestured toward range breakouts earlier today, but have since retreated to the safety and monotony of their previous ranges. So much for the epic volatility associated with quadruple witching days, eh?! Fannie Mae 4.0 coupons are unchanged on the day at 100-25 and 10yr notes are about 2bps higher at 2.9454. MBS never really got high enough to justify reprices for the better. Indeed, today's trading range, with the exception of some early morning drama, has been exceedingly boring, equivocal, and without significant implication for the future. 2 hours left for stocks to trade though, so there's still a chance of something interesting happening into the after-hours bond-market session. MBS would need to fall 3 more 32nds before we'd be much concerned about potential reprices for the worse.

12:30PM :

ALERT:

MBS Near Highs. Possible Reprices For The Better

After running into a ceiling at 100-27 on numerous occasions this morning, Fannie Mae 4.0 MBS moved briefly to 100-28 but have since returned to 100-27. At the same time, benchmark 10yr Treasuries broke a similarly pesky floor at 2.94, which is also part of a long term trend of resistance, only to bounce back to previous levels. While this isn't indicative of impending reprices for the better, the break from the morning's earlier range is a sign to be alert for that potential. Lenders who released initial rate sheets before 9am are the most likely crowd to take part in reprices, should this hint of bullishness develop into something slightly more.

11:18AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "yep. market gonna be in pre-FOMC mode."

Scott Valins : "somewhat quiet"

Adam Quinones : "Nothing on Monday. Existing Home Sales on Tues. FOMC on Wed. New Home Sales on Thurs. "

Scott Valins : "whats going on early next week?"

Adam Quinones : "trader AIMs all set to "away" status"

Adam Quinones : "market is sleeping."

Gus Floropoulos : "Nasdaq turned negative...SnP almost there."

Matthew Graham : "sure, why not! Maybe some shock value baked in there, but that's completely possible"

Rob Clark : "The Citi bond analyst just said on CNBC she expects the 10 year to hit 2.35%"

Jill Statz : "6%"

Jason York : "ok another USDA question, anyone know the max amount of seller paid closing costs?"

Matthew Graham : "S&P at that good old 1270 level again, lows of the day. TSYs and MBS at best levels of the day, trading rather technically, with a bit of an uptick in volume as technical levels are being tested more seriously"

John McClellan : "highest i have seen front is 42 back is 55"

John McClellan : "USDA will go to 55% with GUS approval"

Michael Rourke : "29/41 on Wells Fargo's AllRegs for USDA. Can go higher with compensating factors."

Jason York : "what are the DTI limits for USDA?"

Victor Burek : "flagstar is about .1 worse then yesterday"