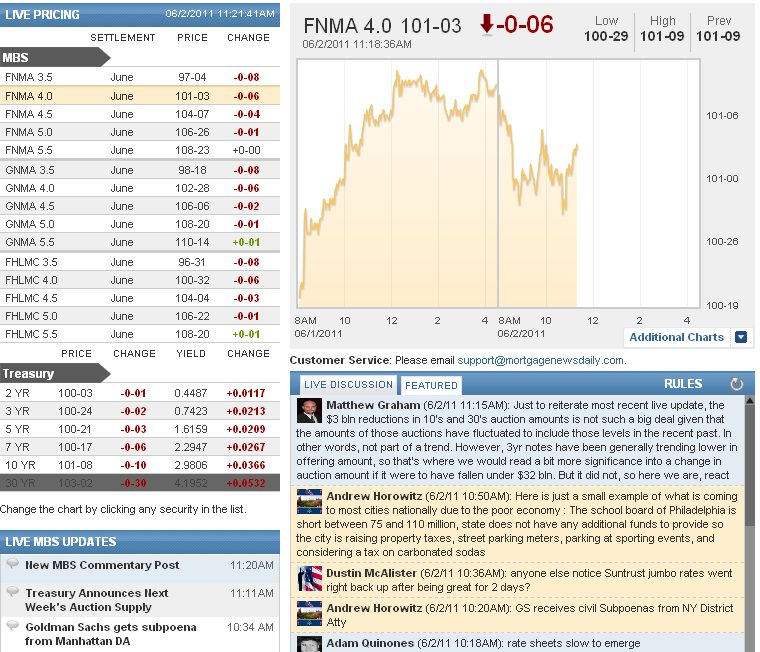

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:00 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:34AM :

Goldman Sachs gets subpoena from Manhattan DA

(Reuters) - Goldman Sachs Group received a subpoena from New York prosecutors seeking information on the investment bank's role leading into the global financial crisis, a person familiar with the matter said.

The subpoena from the Manhattan District Attorney's office is based on information contained in a Senate subcommittee investigation into Wall Street's role in the housing market collapse.

The Manhattan District Attorney's office was not immediately available to comment.

"We don't comment on specific regulatory or legal issues, but subpoenas are a normal part of the information request process and, of course, when we receive them we cooperate fully," Goldman said in a statement.

Goldman's shares were down 2 percent in a broadly flat market.

(Reporting by Lauren Tara LaCapra; Editing by Dan Wilchins andDerek Caney)

10:31AM :

Technical Support Holds. Reprice for Worse Targets Shared

10am data has come and gone and we find TSYs and MBS no better or no worse compared to pre-release levels. 3.00% support in the 10yrTSY note was briefly broken beforehand but that move was quick to correct thanks to weakness in stocks, which have yet to display sustainable strength today. Lenders have been slow to publish rate sheets so far. Of the pricing we've seen rebate has been reduced by 10-25bps. With MBS prices now lower by 8-10/32nds (25 to 32bps) the door is definitely open for early rate sheet publishers to recall and reprice for the worse. This weakness does however seem to be finding some support as stocks are failing to gain momentum in the wake of weak economic data. Benchmark 10s are holding the line below 3.00% and 30yr FN 4.0 MBS coupons are treading water above 101-00. A confirmed breakdown of these levels would force us to issue a "Reprice for the Worse" warning.

10:12AM :

ECON: Factory Orders Broadly Lower

(Reuters) - New orders received by U.S. factories declined in April, partly because of a sharp drop in demand for transportation goods, according to a Commerce Department report on Thursday. Overall orders fell 1.2 percent to a seasonally adjusted $440.4 billion after an upwardly revised 3.8 percent rise in March. That was steeper than the 1 percent fall that Wall Street economists surveyed by Reuters had forecast for April and implied some weakness in the factory sector that had performed relatively well until recently and helped support economic recovery. Transportation orders plunged 9.3 percent in April, nearly wiping out a 10.6 percent rise in March orders. It was the sharpest falloff in monthly transportation orders since an 11.9 percent fall in December. But order declines were widespread in April, affecting categories including primary metals, machinery, computers and electrical equipment in addition to cars and other transportation goods.

9:45AM :

Profit Taking Continues. TSYs Test Key Support

Profit taking continues to pressure Treasury yields higher and MBS prices lower this morning. We haven't seen many rate sheets yet but with 30yr MBS prices down 6 to 8/32nds we'd anticipate a 25bps reduction in loan pricing in 30yr note rates below 4.75%. Since mortgages are mostly playing "follow the leader" right now it's important to mention that benchmark 10yr TSYs are currently retesting key psychological support at 3.00%. While we do not believe a breakdown of this inflection level would lead to all-out selling across the yield curve, rate watchers should take note of the market's willingness to protect this pivot point. We'd like this level to hold and perhaps even draw out some bargain buying. This would be highly-encouraging.

8:56AM :

ECON: Jobless Claims Fall Less than Forecast

(Reuters) - New claims for unemployment benefits fell less than expected last week, according to a government report on Thursday. Initial claims for state unemployment benefits slipped 6,000 to a seasonally adjusted 422,000, the Labor Department said. The prior week's figure was revised up to 428,000. Economists polled by Reuters had forecast claims dropping to 415,000 from a previously reported count of 424,000. The four-week moving average of new jobless claims, considered a better gauge of labor market trends, fell 14,000 to 425,500. The number of people still receiving benefits under regular state programs after an initial week of aid slipped 1,000 to 3.71 million in the week ended May 21. Economists had expected so-called continuing claims to dip to 3.67 million from a previously reported 3.69 million. Initial claims have been volatile in recent weeks as supply chain disruptions from the March earthquake in Japan caused temporary motor vehicle plant closures. Claims have also been distorted by bad weather in some parts of the country and problems smoothing the data for seasonal variations. A Labor Department official said there was nothing unusual in the state-level data, but noted that four states and territories, including Virginia and Oklahoma, had been estimated because of the Memorial Day holiday on Monday. He also said Missouri had indicated that floods were affecting claims in the state, but provided insufficient information to quantify the impact. The number of people on emergency unemployment benefits rose 3,363 to 3.42 million in the week ended May 14, the latest week for which data is available. A total of 7.68 million people were claiming unemployment benefits during that period under all programs.

8:45AM :

ALERT:

Rate Sheets Set to Deteriorate as Investors Take Profits

Rate sheets look destined to shed some bps this morning as investors take profits on interest rate positions following a worse than expected read on initial jobless claims. Yes, you read that correctly. Econ data was WORSE than expected this morning and traders are still taking profits. This is not surprising given the speed and size of the recent rates rally. It isn't a sign of a bearish bias creeping into the bond market. This sort of behavior is actually to be expected ahead of a high-risk event (Employment Situation Report tomorrow morning) as investors look to secure a portion of their earnings "just in case". This should serve as a reminder of the risks associated with floating loans that must be locked on a short timeline. Even in a broader bullish trend, back-ups and reversals are always a threat.

8:28AM :

Rates Rise in Early Trading as Stocks Look to Rebound

Benchmark Treasuries begin the U.S. session slightly worse than yesterday's best levels after weak econ data pushed the 10-year Treasury yield down 11 basis points to 2.939% while equity markets shed more than 2%. The benchmark 10-year Treasury yield remains below the 3% mark at 2.96% in early trading, versus 2.939% at the previous close. Wednesday marked the first time the yield had dipped below the 3% mark since December.

Mortgages performed well yesterday, keeping up with Treasuries and even outperforming in some cases thanks to a lack of loan supply and steady buyer demand. Reprices for the better were reported. Loan pricing hasn't been this aggressive since late November 2010. Loan pricing does however look to weaken a bit this morning as TBAs are backing up a few ticks. The FNCL 4.0 is currently -3/32 at 101-06. S&P 500 futures are 2.00 points higher at 1,314. That compares with a 31 point drop Wednesday - the worst single day since last August. Dow futures are 6 points up at 12,283, versus a 280 points descent on Wednesday.

Global equities have been bathed in red following the U.S. sell-off. Markets in Asia fell between 1.40% and 1.70%, and the ongoing session is in Europe is about as bad: France's CAC-40 is down 1.12% and London's FTSE 100 is off 0.75%. "Global equities are on shaky ground this morning following yesterday's steep declines in North America after the weak ADP print spooked investors and put into question the strength of the U.S. economy," said economists at BMO Capital Markets. "Despite a downgrade to Greece's credit rating by Moody's - three notches lower to Caa1 - late Wednesday, taking it deep into junk territory, the EUR is bouncing back this morning following strong demand at a Spanish bond auction." Commodity prices are relatively flat. Light crude oil rose 0.12% overnight to $100.42 per barrel, and gold prices rose 0.10% to $1,544.70 per ounce.

7:39AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Andrew Horowitz : "Here is just a small example of what is coming to most cities nationally due to the poor economy : The school board of Philadelphia is short between 75 and 110 million, state does not have any additional funds to provide so the city is raising property taxes, street parking meters, parking at sporting events, and considering a tax on carbonated sodas"

Dustin McAlister : "anyone else notice Suntrust jumbo rates went right back up after being great for 2 days?"

Andrew Horowitz : "GS receives civil Subpoenas from NY District Atty"

Adam Quinones : "rate sheets slow to emerge "

Adam Quinones : "stocks back in to green on weaker than expected factory orders. has to be short covering...."

Adam Quinones : "Today 10:00 - U.S. APRIL FACTORY ORDERS -1.2 PCT (CONSENSUS -1.0 PCT) VS MARCH +3.8 PCT (PREV +3.4 PCT) Today 10:00 - U.S. APRIL DURABLES ORDERS UNREVISED AT -3.6 PCT Today 10:00 - U.S. APRIL NONDEFENSE CAP ORDERS EX-AIRCRAFT REVISED TO -2.3 PCT FROM -2.6 PCT Today 10:00 - U.S. APRIL FACTORY ORDERS EX-TRANSPORTATION -0.2 PCT VS MARCH +2.9 PCT (PREV +2.6 PCT) Today 10:00 - U.S. APRIL FACTORY ORDERS EX-DEFENSE -1.2 PCT VS MARCH +3.6 PCT Today 10:00 - U.S. APRIL NONDURABLES ORDERS +0.6 PCT VS MARCH"

Adam Quinones : "in relation to Andy's comment...volume just spiked into the equity down trade 4 min ago."

Andrew Horowitz : "Talked with a trader friend of mine last night, said the selling in stocks was "Fear driven""

Jeff Anderson : "GMAC off about 20 bps from their reprice at 12:20ish yeasterday."

Adam Quinones : "Stock lever helping us out...S&Ps down 0.25% now."

Daniel Kramer : "their rates are amazing right now"

Daniel Kramer : ".139 bos worse on their 30 yr fixed"

Daniel Kramer : "5/3 just came out with their rate sheet, the first one"

Adam Quinones : "yes. large rebate improvements seen yesterday."

Andrew Horowitz : "did the major investors pass through all of the gains yesterday?"

Andrew Horowitz : "nice 3.00 providing support and dow went red"

David Z. : "yes, still none here"

Adam Quinones : "rate sheets a little late this AM?"

Adam Quinones : "The ADP Private Sector Employment number only increased by 38,000 in May, far less than the 175k that was expected. But remember that the ADP number, while it grabs headlines, is of dubious predictive ability for tomorrow's government-produced employment number. Over the last 6 months alone ADP's initial figure has ranged from understating the gain in jobs by 5k to overestimating it by 184k!"

Chris Kopec : "gm everyone......In May of 2010, ADP was completely out of line with NFP....(+63k v +432k). Granted, that was I believe census related. Is there anything with respect to adjustments this month that might lead to another big miss?"

Ken Crute : "HA mg fyi, my secondary just took our .25% improvment from yesterday back, check and mate "

Adam Quinones : "agreed...plus technology is really adding some umph to efficiency"

Victor Burek : "or underestimate their fear of losing their job"

Adam Quinones : "i love it. economists continue to underestimate the productivity potential of US firms and workers."

Adam Quinones : "Today 08:30 - U.S. Q1 NON-FARM PRODUCTIVITY REVISED TO +1.8 PCT (CONS +1.7 PCT), PREV +1.6 PCT Today 08:30 - U.S. Q1 NON-FARM UNIT LABOR COSTS REVISED TO +0.7 PCT (CONS +0.8 PCT), PREV +1.0 PCT "

Adam Quinones : "Today 08:30 - US JOBLESS CLAIMS FELL TO 422,000 MAY 28 WEEK (CONSENSUS 415,000) FROM 428,000 PRIOR WEEK (PREVIOUS 424,000) Today 08:30 - US JOBLESS CLAIMS 4-WK AVG FELL TO 425,500 MAY 28 WEEK FROM 439,500 PRIOR WEEK (PREVIOUS 438,500) Today 08:30 - US CONTINUED CLAIMS FELL TO 3.711 MLN (CON. 3.670 MLN) MAY 21 WEEK FROM 3.712 MLN PRIOR WEEK (PREV 3.690 MLN) Today 08:30 - US INSURED UNEMPLOYMENT RATE UNCHANGED AT 3.0 PCT MAY 21 WEEK "

Mike Drews : "Our secondary dept actually sent an email out last night strongly urging all to considering locking up by the end of the day today...i've never seen them express an opinion before"