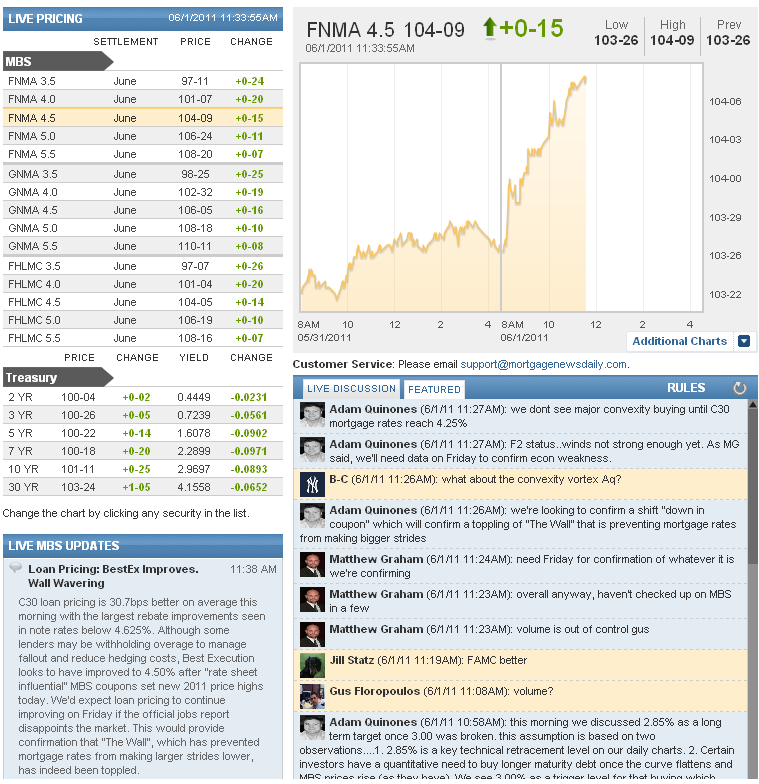

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:02 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:24AM :

ALERT:

MBS Reach New 2011 Highs. Positive Reprices, Delays Possible

"Rate sheet influential" MBS prices are being pulled to new 2011 price highs as Treasuries rally (into the 2.00% handle) in the wake of weak jobs and manufacturing data. The Fannie Mae 30yr 4.0 MBS coupon is currently +16/32 at 101-03 while the Ginnie Mae 4.0 coupon is +15/32 at 102-28. If your lock desk has not already released loan pricing it may be delayed until the market settles. If you've already received your rate sheet, it may be recalled and repriced for the better.

10:18AM :

Renovations Lift Construction Spending in April

(Reuters) - U.S. construction spending rose in April to record the largest gain in six months, likely boosted by home renovations, but the prior month's outlays were revised down sharply, a government report showed on Wednesday. Construction spending increased 0.4 percent to an annual rate of $764.98 billion, the Commerce Department said. March's construction spending was revised to show a modest 0.1 percent increase rather than the previously reported 1.4 percent advance. Economists polled by Reuters had forecast construction spending rising 0.3 percent in April. Overall construction spending dropped 9.3 percent from a year ago. Private construction spending rose 1.7 percent as investment in residential projects climbed 3.1 percent to $232.13 billion, most likely because of an increase in renovations as housing starts fell sharply in April. Spending on new single family home construction fell 1.0 percent, while outlays on multifamily homes eased 0.1 percent in April. Private nonresidential outlays rose 0.5 percent. Spending on public construction fell 1.9 percent in April, with outlays on federal projects dropping 2.0 percent. Construction spending by state and local governments declined 1.9 percent. (Reporting by Lucia Mutikani, Editing by Andrea Ricci)

10:15AM :

Manufacturing Sector Sees Slowest Growth Since Sept 2009: ISM

(Reuters) - The pace of growth in the U.S. manufacturing sector tumbled in May, slackening more than expected to its slowest since September 2009, according to an industry report released on Wednesday. The Institute for Supply Management (ISM) said its index of national factory activity fell to 53.5 in May from 60.4 the month before. The reading missed economists' expectations for 57.7.

A reading below 50 indicates contraction in the manufacturing sector, while a number above 50 means expansion.

New orders fell to 51.0 from 61.7 in April, the lowest since June 2009. The index for prices paid fell to 76.5 from 85.5, below expectations of 82.0.

The data echoed earlier regional reports that showed softer manufacturing growth last month. (Reporting by Leah Schnurr, Editing by Chizu Nomiyama)

8:38AM :

New MBS Commentary Post

8:33AM :

ALERT:

Loan Pricing Looks to Improve After Weak Jobs Report

Loan pricing is set to improve by 12 to 25bps this morning after the ADP Private Payrolls survey indicated disappointing job growth in May. "Rate sheet influential" MBS coupon prices are up 5 to 8/32 and the benchmark 10yr note is testing psychological resistance at 3.00% as stock futures fall. While this report is not the "be all, end all" in terms of jobs data, it does provide a preview of things to come this Friday when the BLS releases the official Employment Situation Report.

8:26AM :

Private Sector Job Growth Greatly Disappoints in May: ADP

The ADP Employment Report shows U.S. private payrolls increased by a disappointing 38,000 private sector jobs in May. This was well below economists' expectations for a gain of 175,000 jobs and is the lowest print since September 2010. From the release: A deceleration in employment, while disappointing, is not entirely surprising. In the first quarter, GDP grew at only a 1.8% rate and only about 2¼% over the last four quarters. This is below most economists’ estimates of the economy’s potential growth rate and normally would be associated with very weak growth of employment. While employment in the service-providing sector rose by 48,000, marking 17 consecutive months of employment gains, employment in the goods-producing sector fell 10,000 following six months of increases. Manufacturing employment fell 9,000 in May following seven consecutive monthly gains. Employment in the construction industry dropped 8,000 in May, completely reversing April’s increase. The total decrease in construction employment since its peak in January 2007 is 2,124,000. Employment in the financial services sector decreased 6,000 in May.

8:15AM :

Refi Demand Declines Despite 2011 Rate Lows

Mortgage applications decreased 4.0 percent from one week earlier, according to data from the Mortgage Bankers Association's Weekly Mortgage Applications Survey for the week ending May 27, 2011. The Market Composite Index, a measure of mortgage loan application volume, decreased 4.0 percent on a seasonally adjusted basis from one week earlier. The Refinance Index decreased 5.7 percent from the previous week. The seasonally adjusted Purchase Index was essentially unchanged from one week earlier. "Interest rates fell last week as incoming economic data was weaker than anticipated. Despite this drop in rates, the number of refinance applications fell. In fact, the last time mortgage rates were this low, refinance volume was more than twenty percent higher. It is likely that many borrowers still cannot qualify to refinance given the lack of equity in their homes," said Mike Fratantoni, MBA's Vice President of Research and Economics.

8:10AM :

Planned Layoffs: +1.8% to 37,135 in May

The pace of downsizing remained virtually unchanged in May, as U.S. employers announced plans to cut 37,135

positions from their payrolls during the month. That is just 1.8 percent more than the 36,490 job cuts in April, according to the report released Wednesday by global outplacement firm Challenger, Gray & Christmas, Inc. The May total was also about the same as a year ago, declining just 4.3 percent from the 38,810 job cuts announced in May 2010. May marks the third time this year and the tenth time in the last 14 months that announced job cuts totaled less than 40,000. Employers have now announced 204,374 job cuts in 2011, 21 percent fewer than the 258,319 planned layoffs reported in the first five months of 2010. The government and non-profit sector continues to dominate monthly

job-cut announcements, with these employers reporting 14,755 in May or nearly 40 percent of all job cuts announced during the month. The May total was up 37 percent from April’s 10,371, but 11.6 percent lower than the 16,697 government job cuts announced in May 2010. Since January 2009, the government and non-profit sector has announced 380,523 job cuts.

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "this morning we discussed 2.85% as a long term target once 3.00 was broken. this assumption is based on two observations....1. 2.85% is a key technical retracement level on our daily charts. 2. Certain investors have a quantitative need to buy longer maturity debt once the curve flattens and MBS prices rise (as they have). We see 3.00% as a trigger level for that buying which creates a vortex that could suck 10s down to 2.85% in a short timeframe. This is not a guaranteed event but it is a behav"

Jeff Anderson : "AQ/MG, do we have any significant resistance in the picture prior to the 2.85% everyone was talking about?"

Chris Kopec : "The good news is that I've learned from 2010 Q4. I'm like a freaking ninja now."

Jeff Anderson : "Merrimack repriced already."

Matthew Graham : "perhaps even higher, but no 1pm auction today"

Matthew Graham : "volume on par with the 2mil + contracts day from thursday last week"

Chris Kopec : "AQ/MG: Volume heavy ?"

Matthew Graham : "3 ticks narrower between 4.5's and 4's since data"

Adam Quinones : "Today 10:00 - US APRIL TOTAL CONSTRUCTION SPENDING LARGEST RISE SINCE +1.1 PCT IN OCTOBER 2010 "

Adam Quinones : "Today 10:00 - US APRIL CONSTRUCTION SPENDING +0.4 PCT (CONSENSUS +0.3) TO $765.0 BLN VS MARCH +0.1 PCT (PREV +1.4 PCT) "

Adam Quinones : "Today 10:00 - US APRIL CONSTRUCTION SPENDING +0.4 PCT (CONSENSUS +0.3) TO $765.0 BLN VS MARCH +0.1 PCT (PREV +1.4 PCT) "

Adam Quinones : "Today 10:00 - ISM U.S. MANUFACTURING PRICES PAID INDEX 76.5 IN MAY (CONSENSUS 82.0) VS 85.5 IN APRIL "

Adam Quinones : "Today 10:00 - ISM U.S. MANUFACTURING NEW ORDERS INDEX 51.0 IN MAY VS 61.7 IN APRIL "

Adam Quinones : "Today 10:00 - ISM REPORT ON U.S. MANUFACTURING SHOWS PMI AT 53.5 IN MAY (CONCENSUS 57.7) VS 60.4 IN APRIL "

Jeff Anderson : "Morning Team. Just catching up on the posts. Wow. Amazed about the 2mm job losses in construction since 2007 post. And don't see that roaring back anytime soon. What other field would they go into?"

Jill Statz : "I am wholesale with them so not sure about corrs"

Ira Selwin : "famc corres?"

Jill Statz : "FAMC just sent out a 5 page memo on guidelines...seems they are loosing them up"

Adam Quinones : "not seeing a strong move "down in coupon"...still mostly directional to rates aka "follow the leader".Only modest buying from real$ accounts. Not much originator hedging w/ 4.0s still...."

Adam Quinones : "that will bring you up to speed on what is going on in the economy"

Adam Quinones : "hi Joe! it's related to the economic slowdown and the end of QEII"

Joe Ridings : "Hey guys! Been gone for a while. Is the current rally related to the end of QE2 or the anticipation of QE3? "

Adam Quinones : "2.85 has always been our 10yr rally target in the event of "repeated history". It is a key retracement level. There is little resistance in the way between 3.00 and 2.85...this is a convexity vortex where real$ buyers will be forced to adjust their cash flows to better match shortening asset durations. "

Adam Quinones : "2.85 is our target Ira"

Adam Quinones : "not out the gate Brent. More likely down the road if the slowdown intensifies"

Ira Selwin : "MG - you mentioned 2.85 on the low side to watch the other day right?"

Brent Borcherding : "AQ--It is likely, though, that they'll let it expire and then we would look at a qtr or 2 without it right?"

Andy Pada : "at least the rumor will begin resurface with some bark"

Brent Borcherding : "The worse the data gets the more likely it gets. "

Adam Quinones : "no Andy. Not at all."

Andy Pada : "QE3 really out of the question?"

Adam Quinones : "the shift "down in coupon" matters to loan originators because it increases demand for 4.0 MBS coupons which makes it easier to hedge loan pipelines with 4.0 coupons which allows secondary to offer better pricing on mortgage rates below 4.625%"

Adam Quinones : "Down in Coupon: Trading lower on the MBS coupon stack, i.e. going from a holding of 6.0s to 4.0s, or 4.5%s to 4.0%. The purpose of the trade in most instances is to buy a longer duration security to prosper as rates rally. That also infers a flatter yield curve, where longer maturities are gaining at a faster pace than shorter ones (10yrs outperforming 2yr notes for example). This trade reduces prepay risk as declining mortgage rates insinuate higher MBS coupons will be called out (prepaid) at p"

Adam Quinones : "down in coupon in progress......."

Adam Quinones : "we havent seen much hedging with 4.0 coupons yet Chris. As soon as we see that it will indicate "The Wall" is falling."

Christopher Stevens : "Are we really going to see a 4.250% 30YR CONV mortgage again. "

Matthew Graham : "to give you an idea, in the 5 minutes following Thursday's 830am data, just over 50k 10yr contracts were traded. In the 5 minutes following this morning's ADP, 71k. "

Matthew Graham : "volume spike following ADP. "

Adam Quinones : "today s/be interesting. there will be a deluge of hedging once this rally is confirmed."

Adam Quinones : "not until we see some production flow into that coupon"

Victor Burek : "4.0 the title holder now?"