MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:01 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:37AM :

ALERT:

Positive Reprices and Delays Possible. BEWARE OF PROFIT TAKING

This alert is intended to inform you of improving price levels in the MBS market. Appreciations haven't been huge but the uptick has been big enough to force some lenders into delaying the release of their rate sheets until stable ground is found. Reprices for the better are possible if your lender did not reprice for the better yesterday afternoon and they issued before 9am today. BEWARE OF PROFIT TAKING THOUGH. Stocks are attempting a recovery rally and bonds are overbought.

10:08AM :

ECON: Home Prices Fall 0.3 pct in March - FHFA

According to purchase prices of homes financed with Fannie or Freddie loans, home prices dropped 0.3 pct in March, bringing the FHFA's Home Price Index to 181.3. The 12 month decline now stands at -5.8 pct. Despite the ongoing declines, the -0.3 pct pace is slower than Feb's 1.5 pct decline and Jan's -1.6 pct.

10:02AM :

Mortgage Banks Focus on Controlling Expenses

(Bloomberg) - Wells Fargo & Co. (WFC), the biggest U.S. home lender, is concentrating on controlling expenses including the cost of bad mortgages, Chief Executive Officer John Stumpf said. The bank “continued to focus on corporate-wide expense reductions,” according to a presentation by Stumpf today at a London investor conference sponsored by Barclays Plc. Non- interest expenses dropped 5 percent in the first quarter from the final three months of 2010, the presentation said.

The first quarter didn’t yet reflect a new company-wide effort to identify reductions, and the San Francisco-based bank expects expenses tied to soured loans will drop if the economy doesn’t weaken, according to Stumpf’s prepared remarks. Wells Fargo, as the second-largest U.S. mortgage servicer, faces scrutiny from federal regulators, state officials and consumer advocates over its handling of foreclosures. The lender was one of 14 of the largest servicers to sign consent decrees compelling them to overhaul procedures for seizing homes and pay back homeowners for losses on foreclosures that were mishandled. State and federal officials have been negotiating with the mortgage servicers, which include Citigroup Inc., Bank of America Corp., JPMorgan Chase & Co. and Ally Financial Inc., which handle almost 60 percent of U.S. home loans. The five banks proposed paying $5 billion to settle the probe by all 50 states that’s being led by Iowa Attorney General Tom Miller into the mortgage servicing industry, two people familiar with the matter said earlier this month. Stumpf declined today to predict the outcome.

9:25AM :

MBS Into Best Levels. TSYs Rally on ECB Comments

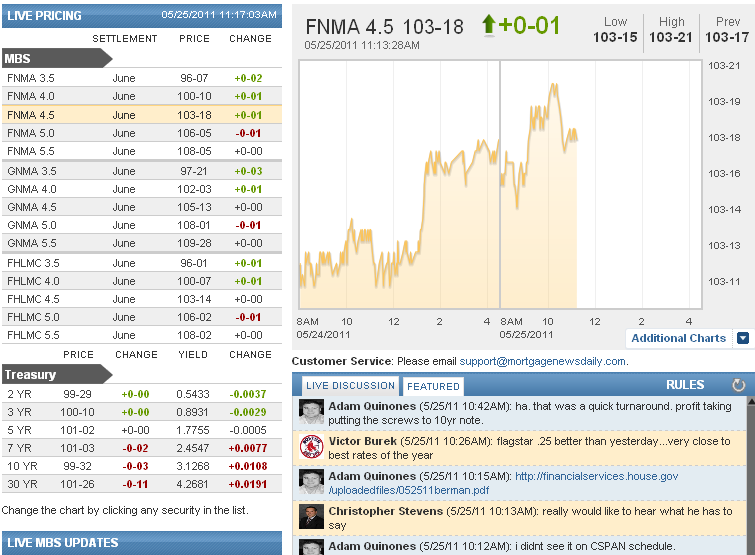

Another day, another chance for US Treasuries to rally on an EU-periphery-driven flight-to-safety. Benchmark 10yr notes were already content with holding supportive levels near their previous lows of the day and had been inching back from there. But beginning with comments from ECB's Stark regarding the dire situation for Greece and culminating with EU Commissioner Damanaki's comment that Greece's Euro-Zone membership is at risk and that the country must adopt tough austerity measures or return to the Drachma, 10yr yields moved to their lowest levels of the day, 3.11. S&P futures continued to weaken as well. FNCL 4.5 MBS paced the brief rally fairly well, also moving to their best levels of the day at 103-19.

9:00AM :

Foreclosuregate: Banks Threatened by State Attorneys

(WSJ) - State attorneys general told five of the nation's largest banks on Tuesday they face a potential liability of at least $17 billion in civil lawsuits if a settlement isn't reached to address improper foreclosure practices, according to people familiar with the matter. The figure doesn't cover additional billions of dollars in potential claims from federal agencies such as the Department of Housing and Urban Development and the Justice Department. State and federal officials haven't proposed a specific comprehensive settlement figure, but Tuesday's discussions represented the first effort to formally quantify potential liability. Banks and federal officials have made halting progress over two months to settle allegations of abuses related to mortgage servicing, and the numbers floated Tuesday indicate that the two sides are still far apart on the size of the penalty.

Banks have proposed a $5 billion settlement that would be used to compensate any borrowers previously wronged in the foreclosure process and provide transition assistance for borrowers who are ousted from their homes. Federal and state officials have dismissed that as insufficient. Some officials have pushed for a total price tag of more than $20 billion to resolve foreclosure-handling abuses that surfaced last fall. State attorneys general from all 50 states and the District of Columbia announced investigations last fall. Tuesday's discussions highlighted the potential for lawsuits alleging unfair and deceptive practices if a settlement isn't reached.

8:52AM :

Money Moving to Sidelines Following Durable Goods

Despite a weaker than expected reading on Advance Durable Goods, both bond markets and stocks are weaker following the report. FNCL 4.5's moved from 103-18 to 103-14 but have moderated to 103-16. 10yr yields moved up around 1.5 bps to 3.13, matching their weakest levels of the morning, but so far have not gotten any weaker. The next scheduled data is FHFA's Home Price Index at 10am.

8:45AM :

OECD: Structural Unemployment is Pressing Issue

(OECD) - The global recovery is firmly under way, but is taking place at different speeds across countries and regions, according to the OECD’s latest Economic Outlook. The top challenge facing countries continues to be dealing with widespread unemployment, which affects more than 50 million people in the OECD area. Governments must ensure that employment services and training programs actually match the unemployed to jobs. They should also rebalance employment protection towards temporary workers; consider reducing taxes on labor via targeted subsidies for low paid jobs; and promote work-sharing arrangements that can minimize employment losses during downturns. “This is a delicate moment for the global economy, and the crisis is not over until our economies are creating enough jobs again,” said OECD Secretary-General Angel Gurría. “There is also some concern that if downside risks reinforce each other, their cumulative impact could weaken the recovery significantly, possibly triggering stagflation in some advanced economies.” n advanced economies structural reforms can play a greater in role in boosting growth as governments are forced to withdraw fiscal and monetary stimulus launched in reaction to the crisis. In emerging-market economies, structural reforms have the potential for making growth more sustainable and inclusive, while contributing to global rebalancing and enhancing long-term capital flows, the OECD said. Emerging economies must also pay particular attention to the danger of overheating, which is increasing inflationary pressures, and in some cases, widening current account imbalances.

8:35AM :

ECON: Durable Goods Orders Fall More Than Expected

New orders for manufactured durable goods in April

decreased $7.1 billion or 3.6 percent to $189.9 billion,

the U.S. Census Bureau announced today. This

decrease, down two of the last three months, followed a

4.4 percent March increase. Excluding transportation,

new orders decreased 1.5 percent. Excluding defense,

new orders decreased 3.6 percent. Transportation equipment, also down two of the last

three months, had the largest decrease, $4.9 billion or

9.5 percent to $46.7 billion. Inventories of manufactured durable goods in April, up

sixteen consecutive months, increased $3.2 billion or 0.9

percent to $350.5 billion. This was at the highest level

since the series was first published on a NAICS basis in

1992 and followed a 1.7 percent March increase.

Transportation equipment, also up sixteen consecutive

months, had the largest increase, $1.0 billion or 1.0

percent to $106.1 billion. This was also at the highest

level since the series was first published on a NAICS

basis in 1992 and followed a 2.4 percent March increase.

7:47AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "our comments re: mini-refi boom: http://www.mortgagenewsdaily.com/05252011_mba_applications.asp"

Adam Quinones : "Color from MBS Trader. It line with our thoughts, " Higher coupons taking a breather today as most flows this

morning are down in coupon. 5% and higher are 1 to 2 ticks

weaker vs USTs and 3.5% and 4% are 2 to 3 ticks tighter. This

is most likely profit taking as UIC has had a tremendous run.

Refi index slightly higher this morning, but don't believe any

real refi expections with rates near 4.5%. Origination has

been mostly 1bnish/day and woul"

Adam Quinones : "ha. that was a quick turnaround. profit taking putting the screws to 10yr note."

Victor Burek : "flagstar .25 better than yesterday...very close to best rates of the year"

Adam Quinones : "http://financialservices.house.gov/uploadedfiles/052511berman.pdf"

Christopher Stevens : "really would like to hear what he has to say"

Adam Quinones : "i didnt see it on CSPAN schedule. "

Christopher Stevens : "does anyone know if the Michael Berman testifying in front of House subcommitte is being webcast?"

Andrew Horowitz : "Wow mark Haines Died"

Victor Burek : "it is AQ...but would rahter pretend witha 4.25% rate thena 6% rate"

Ken Crute : "VB to your point, I 99% agree, (mostly since my argument is so flawless) but how many are taking their savings from their refi an spending it, most seem to be paying down debt or saving, "

John Rodgers : "ST hit the Key loan program 1 point worse to price today. I hate lenders that do that."

Adam Quinones : "bc homes are worth less which means payoffs will be short."

Victor Burek : "why not allow more to refi without appraisals"

Adam Quinones : "* "more losses""

Adam Quinones : "seems logical..just gotta figure out that whole "underwater" issues. MBS holders gotta take losses."

Victor Burek : "but refi'ing to lower rate frees up monthly cashflow which will be spent into the economy...which can helpe create jobs which would help the housing market"

Ken Crute : "refi boom would be great, as my creditors really like getting paid everymonth and I like to eat food, but don't think it will fix long term housing issues, seems like the ones we refid for the most part were not in danger of default, and now less likely to sell down the road if they are locked at 4.25.... my ever so humble opinion that is 100% accurate "

Mike Drews : "hmmm...GMAC 15 year pricing is worse this morning"

Christopher Stevens : "interesting.. http://www.marketwatch.com/story/why-bernanke-will-be-forced-to-institute-qe3-2011-05-25"

Adam Quinones : "Rates are at 6-month lows but loan demand hasn't increased as much as one might have anticipated. Last week we wrote, "Right now we're witnessing the beginnings of a mini-refinance boom in the primary mortgage market, but there has been little activity in the secondary market that would indicate increased rate locking by consumers." says MND's Managing Editor Adam Quinones. "However, if conventional 30-year rates reach 4.25%, we'd expect to see a mini-boom scenario play out. There is much stored"

Adam Quinones : "Loan Demand Lags Interest Rate Rally. Several Reasons Cited: http://www.mortgagenewsdaily.com/05252011_mba_applications.asp"

Ken Crute : "The following updates have been made regarding retirement accounts:

The requirement to document the terms of allowing a withdrawal from a retirement account was removed. A new policy was added that disallows retirement accounts as an asset for reserve calculation purposes when withdrawals for any reason are prohibited currently."

Ken Crute : "just got this on my desk this morning FNMA 2011-04, anyone else see it? "

Brent Borcherding : "1% in rate is equal to the same payment because of new MI"

Mike Drews : "you have to drop someone's rate about a full point for it to make sense."

Ken Crute : "didn't do a lot of FHA refis, most were DURP "

Ira Selwin : "I agree VB, haven't seen a streamline come across my desk in quite awhile"

Victor Burek : "ken...the new monthly MI on FHA pretty much put the brakes on another refi boom"

Matthew Graham : "ECB'S STARK SAYS NO CERTAINTY THAT EVENTS WE HAVE JUST LIVED THROUGH WON'T BE REPEATED "

Adam Quinones : "60/40 bc my econ outlook is one of disappointment."

Terry Colabrese : "AQ, what's your feeling as to the probability of "sustained commitment to lower yields"?"

Adam Quinones : "moving down in coupon from here gets pricey from a hedging perspective."

Adam Quinones : "a sustained commitment to lower yields."

Victor Burek : "whats it gonna take to break through this current level?"