MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:01 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:24AM :

ECON: Job Openings Rate Unchanged - BLS

There were 3.1 million job openings on the last business day of March,

the U.S. Bureau of Labor Statistics reported today. The job openings

rate (2.3 percent) was unchanged over the month, following a gain in

February. The hires rate (3.1 percent) and the separations rate (2.9

percent) also were unchanged in March. This release includes estimates

of the number and rate of job openings, hires, and separations for the

total nonfarm sector by industry and geographic region.

Job Openings

The number of job openings in March was 3.1 million, up from 3.0

million in February. (See table 1.) This marks the first time since

November 2008 that job openings have been at or above 3.0 million for

two consecutive months. The job openings level has trended up since

the end of the recession in June 2009 (as designated by the National

Bureau of Economic Research) but remains well below the 4.4 million

openings when the recession began in December 2007.

The number of job openings in March (not seasonally adjusted)

increased from 12 months earlier for total nonfarm, total private,

eight industries, and the Northeast and Midwest regions. The level

decreased over the year for government due to decreases for federal

government. Over-the-year comparisons for federal

government are impacted, in part, by the large number of temporary

workers employed to conduct the 2010 Census.

10:02AM :

Mortgage Rates, Loan Demand and the End of QEII

Although the Fed's daily asset purchases have indeed been supportive of lower benchmark yields, there are big picture factors to consider in the directional move we've witnessed over the past month. Expansion in the global economy seems to be slowing and investors are acting increasingly nervous about their allocation choices. If it is confirmed that emerging economies have hit a rough patch, the impact of such a slowdown would spread through the U.S. economy starting with the manufacturing sector. This would be a favorable development for interest rates and serve as a reminder of how sensitive our economic recovery really is in the long run. The Federal Reserve is scheduled to complete its quantitative easing (QE) program by the end of June. If the economy does indeed slide for the worse and the Fed does not decide to re-up its QE program, it may actually lead interest rates lower as the broader economy suffers from reduced liquidity in financial markets.

Would significantly lower interest rates spark an increase in loan demand? We think 30-year fixed mortgage rates need to approach 4.25% before a sizable uptick in refinance demand is observed. On the buyer front, since early February we've heard reports from originators about a seasonal increase in purchase loan demand, since then purchase business seems to have slowed. Falling rates will certainly increase affordability conditions though, which helps offset the notion that home prices have more room to run lower. The road ahead is long and paved with much uncertainty....the economic recovery will be choppy at best until the housing market is able to sustain consistent positive progress.

9:02AM :

ALERT:

MBS Indicated Lower. Rebate Reductions Expected

There is little market reaction to speak of after 830 trade deficit data revealed a wider than expected gap in March, which can be attributed to a spike in oil prices. Benchmark 10s are consolidating around the 3.21% pivot, driven mostly by pre-auction positioning which includes short-covering at recent price lows/yield highs. Mortgages are performing well after the roll as lower dollar prices have led some folks to buy back their hedges (short covering), which effectively reduces the amount of "coverage" secondary has on its loan pipeline. Reprices for the worse were noted yesterday afternoon, with MBS indications tailing off a bit more this AM, look for rate sheets to shed a few more bps. Rebate reductions should be minimal though, no change in Best Execution is expected. NEXT EVENT: $24bn 10yr note auction at 1pm.

8:35AM :

ECON: Trade Deficit Wider on Higher Oil Prices. Exports Still Impressive

Reuters) - The U.S. trade deficit widened more than expected in March, as exports leapt to a new record but imports rose nearly 5 percent as oil prices jumped, a U.S. government report showed on Wednesday. The deficit rose to $48.2 billion, the widest since June 2010, from a slightly downwardly revised $45.4 billion in February. Analysts surveyed before the report had pegged the March trade gap at $47.0 billion. U.S. exports grew 4.6 percent in March to a record $172.7 billion, in the biggest month-to-month gain since March 1994. But imports grew 4.9 percent to $220.8 billion as the average price for imported oil hit $93.76 per barrel, the highest since September 2008. The wider-than-expected trade gap could prompt analysts to trim their estimates of already weak first-quarter U.S. economic growth. But the rise in imports and exports also suggested strengthening U.S. and global demand as trade returns to pre-crisis levels. Both U.S. goods and U.S. services exports set records in March, as did two sub-categories - foods, feeds and beverages and industrial supplies. U.S. exports to Canada and South and Central America also set records and exports to the European Union were the highest since July 2008. U.S. imports were the highest since August 2008, just as the global financial crisis was beginning to bite into trade. Imports hit a record $232.1 billion in July 2008, before tumbling sharply over the next six months. U.S. petroleum imports were also the highest since August 2008 and the U.S. petroleum trade deficit was the widest since October 2008. The closely watched U.S. trade deficit with China narrowed slightly in March to $18.1 billion, as U.S. exports to that country grew faster than imports from the Asian giant. However, the trade shortfall with China for the first quarter of 2011 totaled $60.2 billion, putting it on a pace to exceed last year's record of around $273 billion. (Reporting by Doug Palmer, Editing by Andrea Ricci)

8:33AM :

Newly Issued 3-Year Treasury Note Carries Lower Coupon

You might notice today on the MBS dashboard what seems to be excessive price weakness in the 3-year Treasury note. This is not the case. What you are seeing is the day over day price change between the old "on the run" 3-year Treasury note vs. the new "on the run" 3-year Treasury note, which was just issued yesterday during the 3-year note auction. The reason for the large price discrepancy has to do with the coupon rate that was assigned to the new 3-year note yesterday. The previous "on the run" note had a 1.25% coupon rate while the new note has a 1.00% coupon. The new 1.00% coupon rate resets par pricing on the 3-yr note at 1.00% whereas the previous OTR 3-year note had par pricing (100-00) set at 1.25%. Remember, what you are seeing today is the price change between the old 1.25% coupon vs. the new 1.00% coupon.

8:24AM :

Notification Day Reminder: Why Do MBS Prices Seem to Fall?

Yesterday was Class A Notification Day in the TBA mortgage market. The MBS coupons that determine rate sheet pricing are traded in the TBA MBS market. In the TBA market, at the time a trade is made, buyers and sellers agree to a few specific terms like what coupon, the issuing agency (Fannie, Freddie, Ginnie), size of trade, and the trade price....the actual pools of loans are NOT allocated at the time of this commitment. Instead, the MBS buyer and the seller make an agreement to complete the transaction at a later date. Agency TBA MBS trades typically settle once a month. These dates are also known as "good-day settlement". Two days before the pre-scheduled settlement date, the MBS seller "notifies" the MBS buyer of the specific pools that they will deliver to satisfy the previously agreed upon terms of the trade ."Notification" is part of the "allocations" process, in which pools are delivered against TBA trades at settlement. Class A MBS coupons consist of Fannie Mae and Freddie Mac 30 year pass-throughs. (Class B is comprised of all 15-year fixed pools; Class C consists of 30-year Ginnie I's and II's.) Prices don't really "fall" like they would in a selloff . The price decline reflects the fact that the front month is changing. This is because the front month coupon has just begun the settlement process and the back month has about 30 more days until it settles. The reason that prices for the different months are different is because the economics are different. Buying for front-month settlement means that the investor owns and receives the principal and interest cash flows for that month. Investors that buy for the back month forgo those net benefits; therefore the back month price is generally lower. (The difference between the two months is called "the drop.") This is discussed in more depth here: http://www.mortgagenewsdaily.com/mortgage_rates/blog/210868.aspx

8:18AM :

Mortgage Apps: Refinancing +9%. Purchases +6.7%

The just-released Mortgage Application Index from MBA bumped up 8.2% in the week ending May 6. Refinancings, which account for nearly two-thirds of the index, moved up 9% to their highest level since mid-March, while purchases climbed 6.7%. Compared to last year, however, purchases are down nearly 26%. MBA' Michael Fratantoni commented: "Rates dropped again last week as the Federal Reserve continued its QE2 asset purchase program. The 30-year fixed mortgage rate is now 46 basis points below its 2011 peak, and has decreased for four straight weeks by a total of 31 basis points. Over this four week span, the refinance index has increased by about 18%. Despite the recent increases however, refinance application volumes remain more than 50% below levels seen last fall." The average 30-year fixed-rate mortgage rate fell to 4.67% in the week from 4.76%.

8:17AM :

Rates Moving Higher Ahead of Auction

Interest rates rose yesterday as stocks rallied and bond investors made room for today's $24 billion 10-year Treasury note auction. Equity futures continue to rally this morning after approaching calendar year highs Tuesday thanks to three positive sessions since initiated by Friday's nonfarm payrolls employment report. S&P 500 futures are 0.25 points higher at 1,354 and Dow futures are 32 points up at 12,732. The two indexes closed 10.9 points and 75.7 points higher on Tuesday, respectively. Some attributed the rally to Microsoft's $8.5 billion purchase of Skype. The 10-year Treasury note backed up six basis points Tuesday to 3.20%, denting a rally that began April 11 which pushed the note yield more than 40 basis points lower to its lowest level since late December. Benchmark 10s are currently -4/32 at 103-10 yielding 3.228%. The yield curve is 1bp steeper at 263bps wide. In mortgages, we saw an uptick in originator loan sales yesterday (hedging) as MBS prices seems to have hit at least a short term peak. Most of that hedging was either 4.0 coupon swaps or 4.5 coupon sales outright. The June delivery FNCL 4.5 MBS coupon is -5/32 at 102-28 and the FNCL 4.0 is -4/32 at 99-22. (Don't forget yesterday was Class A Notification Day!). Oil prices fell 0.78% overnight but remain in triple-digits, at $102.60 (-1.23%). Gold prices gained nearly 1% to $1,516.90 in overnight trading but are currently -0.15% at $1514.60

Meantime, China released more economic data for April, showing consumer price inflation CPI dipped less than expected to 5.3% y/y. "That's the second straight month above 5% and suggests that China will be tightening monetary policy further," said economists at BMO Capital Markets. "While more rate hikes are likely, faster yuan appreciation appears increasing probable as well, with the National Bureau of Statistics noting that pressure from imported inflation remains high."

7:50AM :

Banks float $5 billion deal to settle foreclosure probe: report

(Reuters) - Major banks are willing to pay as much as $5 billion to settle claims by federal and state officials of improper mortgage foreclosure practices, the Wall Street Journal reported, citing people familiar with the situation.

The banks' offer comes as mortgage companies and state and federal officials continue their efforts to strike a settlement of investigations sparked by allegations of "robo-signing" and other questionable foreclosure practices that came to light last fall, the Journal said. The banks intend to propose that as much as $5 billion be used to compensate any borrowers previously wronged in the foreclosure process and provide transition assistance for borrowers who are ousted from their homes, the WSJ said, citing people familiar with the matter.

7:07AM :

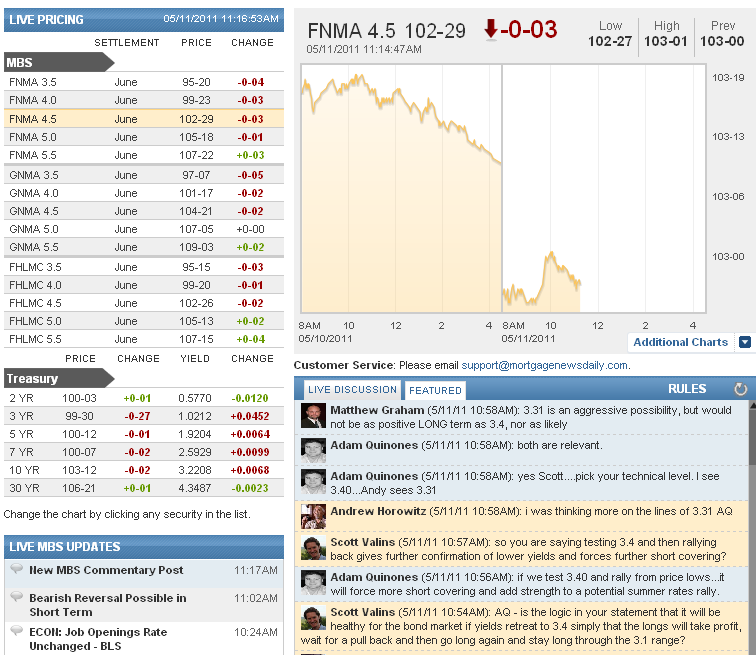

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "3.31 is an aggressive possibility, but would not be as positive LONG term as 3.4, nor as likely"

Adam Quinones : "both are relevant."

Adam Quinones : "yes Scott....pick your technical level. I see 3.40...Andy sees 3.31"

Andrew Horowitz : "i was thinking more on the lines of 3.31 AQ"

Scott Valins : "so you are saying testing 3.4 and then rallying back gives further confirmation of lower yields and forces further short covering?"

Adam Quinones : "if we test 3.40 and rally from price lows...it will force more short covering and add strength to a potential summer rates rally."

Scott Valins : "AQ - is the logic in your statement that it will be healthy for the bond market if yields retreat to 3.4 simply that the longs will take profit, wait for a pull back and then go long again and stay long through the 3.1 range?"

Gus Floropoulos : "im locked up...market has been more than generous....whats that saying AQ about pigs?"

Adam Quinones : "so knee jerk bias becomes SELL"

Adam Quinones : "techs are turning bearish though. market is overbought."

Adam Quinones : "that and CPI too."

Chris Kopec : "AQ....think the market would await UE tomorrow before such a breakout?"

Adam Quinones : "you'd certainly lose some rebate but it would be healthy if rates are to move lower this summer."

Chris Kopec : "Retest of 3.40 would be brutal."

Adam Quinones : "My latest tweet.... AQ_MND: A weak 10yr auction today will confirm a bearish turn-around in rate technicals. Retest of 3.40-42% possible in 10s. 4.875% C30 BestEx"

Andy Pada : "As per appraisals, the underlying problem are the GSEs pushing buybacks based on retrospective appraisals. This policy forces all lenders and appraisers to be unduly conservative. "

Chris Kopec : "We could solve a huge appraisal problem by just allowing the appraiser to get business wherever he wants. Allow the borrower to select the appraiser, and hold a hammer over both of them with respect to non-influence. Make the borrower and the appraiser sign an addendum that is part of the report confirming no relationship/influence. And then, allow lenders to reserve the right to accept/reject/counteroffer any appraisal based upon their internal review (i.e., desk reviews). This crap isn't r"

Chris Kopec : "NMLS is a regulation that is keeping our jobs from being outsourced to India."

Chris Kopec : "Licensing is a regulation that confers professionalism and trust. That's what I'm talking about with appraisers."

Andrew Horowitz : "and the appraisers to be better trained"

Andrew Horowitz : "what you need is appraiser independence"

Adam Quinones : "AMCs make that happen."

Adam Quinones : "my own mother is an appraiser. ive this talk over and over with her. some appraisers are just plain lazy while others dont understand local markets."

Matthew Graham : "if a great comp is distressed, but there are no other distressed homes on the market and haven't been, don't use em... if there are currently comparable homes on MLS for less than the asking price and distressed homes are prevalent enough to be reasonably included as "part of that market" then guess what.... "

Adam Quinones : "ugh. more regulation sounds brutal. we need better training and better appraisers."

Andrew Horowitz : "and the AMC's are more concerned with losing their big contracts with the big banks that they are overly cautious with valuations"

John Rodgers : "we don't need anymore regulations"

Chris Kopec : "Big time regulation AH.....but with a payoff. Appraisers should be the front end of the process. I'd prefer if the appraisal were completed before I even sat down with a client."

Chris Kopec : "I agree 100% AH.....they need to turn appraisers into CPA's, including completing severing their dependence on anyone. To go from depending on mortgage brokers to depending on AMCs is like going from the frying pan into the fire."

Matthew Graham : "not saying this is exactly what I read you as saying AH, but in general, we need to stop looking at valuation as it relates to the appraisal process and underwriting process and rather look at it much much more simply... what someone is willing to pay, and then logically deduce the factors that can affect that on an objective basis"

Chris Kopec : "Correct, AH. I just recently closed a property in my hometown. Appraisal #1 pulled shorts/foreclosures - despite a market history that suggested they were NOT prevalent. Appraisal #2 used non-distressed sales. The difference in values was over $150,000."

Andrew Horowitz : "you can't disregard it, it has already played a factor in the pricing of the property to begin with, but to utilize additional distressed sales when there are sufficient comps in a mile radius makes no sense"

Chris Kopec : "Shorts and foreclosures should in turn drive what non-distressed sellers can offer. So, the market adjustment is already baked into the cake. No need to go even further."

Matthew Graham : "if they're a part of available supply that buyers might reasonably consider as alternatives then they are absolutely effecting the value of the house next door"

Jason York : "actually lenders need to takes FHA's rules as they are written, FHA says that if there is a short sale with no lates, then there is no penalty period, but if there are lates, then it has a 3yr wait period, that is the difference in short sales, whether it was because of the market or because of financial difficulty"

Adam Quinones : "there are definitely instances where appraisers should be including distressed properties in their valuations."

Adam Quinones : "if there are other comps to work with or the area is not totally underwater with distressed props."

Andrew Horowitz : "most appraisers should already be ignoring distressed sales if they are any good CK"

Chris Kopec : "gm all....little late to the foreclosure/short sale debate. My opinion is short sales should not be treated as foreclosures. However, I think both shorts and foreclosures should be firewalled from being used as appraisal comps. We've had a ton of government intervention since the crash.....a little more intervention that actually HELPED the market would be welcome, and a law that requires appraisers to utilize non-distressed sales would be a boon to responsible homeowners who are currently ge"

Jason Zimmer : "a loan mod is a good example of renegotiaed contract where one still meets the obligation under newly agreed upon terms...not a short sale...that's it for me, not going to go back and forth, but i do see your point JR"

John Rodgers : "have you ever seen a foreclosure after the owners move out. They are nomrally trashed and fixtures are usually removed or destroyed. "

John Rodgers : "We are a nation of contracts and contracts can be renegotiated. If a lender agrees to allow a borrower to negotiate a lower pay off in order to forgo a foreclosure then how is that the borrowers moral obligation? "

Jason Zimmer : "you don't pay your obligation means you didn't pay your obligation...no matter what you call it, you didn't meat your obligation"

Victor Burek : "but isnt a foreclosure worse than a short sale?"

Jason Zimmer : "i disagree...they get a reprive, it's called moral obligation"

Victor Burek : " i agree JR"

Jason Zimmer : "JR- it's not an issue with streamlines, you just have to puit a pay stub in the file"

Brent Borcherding : "Why should the get relief?"

John Rodgers : "why don't borrowers get any reprieve from short sales? To treat them as a foreclosure is just not right. They might as have just walked away instead of fooling with the hassle of the short sale process!"

Adam Quinones : "RTRS -GOOLSBEE - OIL PRICES A NEGATIVE, BUT WILL NOT PUSH US BACK INTO RECESSION "