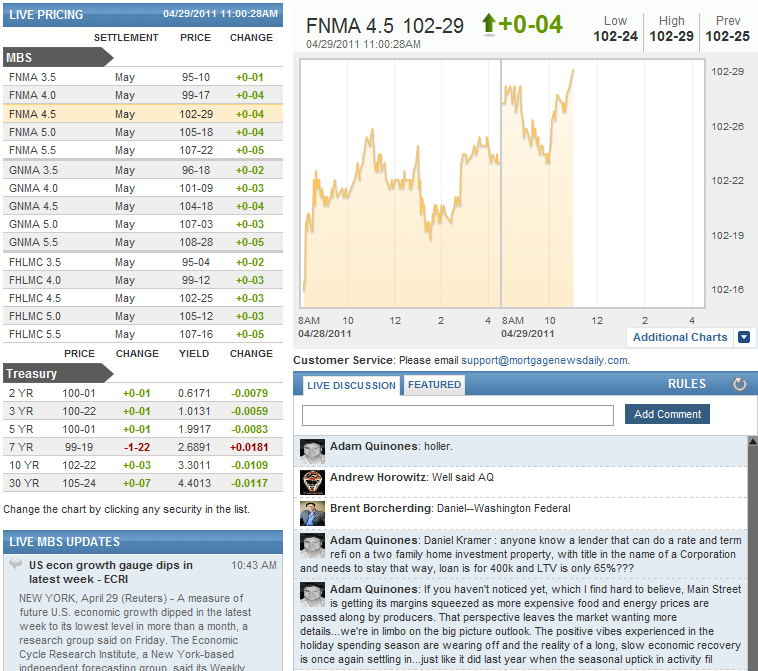

MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:01 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:43AM :

US econ growth gauge dips in latest week - ECRI

NEW YORK, April 29 (Reuters) - A measure of future U.S. economic growth dipped in the latest week to its lowest level in more than a month, a research group said on Friday.

The Economic Cycle Research Institute, a New York-based independent forecasting group, said its Weekly Leading Index slipped to 129.3 in the week ended April 22 from 131.7 the previous week. It was the lowest level since 129.1 in the week of March 18.

The index's annualized growth rate also dipped to 7.5 percent from 7.7 percent a week earlier.

(Reporting by Leah Schnurr, Editing by Chizu Nomiyama)

9:57AM :

DATA FLASH: Consumer Sentiment Near Expectations

* THOMSON REUTERS/U. OF MICH CURRENT CONDITIONS INDEX FINAL APRIL 82.5 (CONSENSUS 82.7) VS PRELIMINARY APRIL 82.7 * THOMSON REUTERS/U. OF MICH CONSUMER EXPECTATIONS INDEX FINAL APRIL 61.6 (CONSENSUS 61.3) VS PRELIMINARY APRIL 61.2 * THOMSON REUTERS/U. OF MICH US CONSUMER SENTIMENT FINAL APRIL 69.8 (CONSENSUS 69.9) VS PRELIMINARY APRIL 69.6 * THOMSON REUTERS/U. OF MICH 12-MONTH ECONOMIC OUTLOOK INDEX FINAL APRIL 80 VS PRELIMINARY APRIL 75 * THOMSON REUTERS/U. OF MICH 1-YEAR INFLATION OUTLOOK FINAL APRIL 4.6 PCT VS PRELIMINARY APRIL 4.6 PCT * THOMSON REUTERS/U. OF MICH 5-YEAR INFLATION OUTLOOK FINAL APRIL 2.9 PCT VS PRELIMINARY APRIL 2.9 PCT

9:54AM :

New MBS Commentary Post

9:46AM :

DATA FLASH: Chicago PMI Slightly Lower

* CHICAGO PURCHASING MANAGEMENT INDEX 67.6 IN APRIL (CONSENSUS 68.5) VS 70.6 IN MARCH * CHICAGO PURCHASING MGMT NEW ORDERS INDEX 66.3 IN APRIL VS 74.5 IN MARCH * CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX 81.8 IN APRIL VS 83.4 IN MARCH * CHICAGO PMI EMPLOYMENT INDEX 63.7 IN APRIL VS 65.6 IN MARCH * CHICAGO PURCHASING MANAGEMENT PRODUCTION INDEX 70.0 IN APRIL VS 74.2 IN MARCH

9:10AM :

MBS and TSYs Slightly Weaker After Econ Data

Whew! It's been quite week in terms of economic goings-on and market movements! Despite today containing just as many data releases as any other, we're sensing a bit of exhaustion in the markets as volume has dropped off substantially and movements have been "safe" as opposed to daring or significant. The slower pace of life this morning likely has to do with the week's "biggies" having come and gone. Today's data is not insignificant, but in the context of FOMC-related events of Wednesday and the auction cycle, it's not up to the task of inspiring a market that is already at an aggressive limit with 10yr yields hovering around 3.30... There's important technical resistance to further improvements here and the moderate weakness so far this morning could, in large part, be resulting from that. MBS are a few ticks from their highs as yields are backing off from their lows in TSYs. We'll see in an upcoming commentary post that this bounce in TSY yields coincides with some large, long-term technicals. Stay tuned!

8:33AM :

DATA FLASH: Employment Cost Index +0.6 pct

* U.S. Q1 EMPLOYMENT COST INDEX +0.6 PCT (CONSENSUS +0.5 PCT) VS Q4 +0.4 PCT (PREV +0.4 PCT) * U.S. Q1 WAGES/SALARIES +0.4 PCT VS Q4 +0.4 PCT (PREV +0.4 PCT) * U.S. Q1 BENEFIT COSTS +1.1 PCT VS Q4 +0.5 PCT (PREV +0.5 PCT)

8:31AM :

DATA FLASH: Incomes and Outlays

* US MARCH PERSONAL SPENDING +0.6 PCT (CONSENSUS +0.5 PCT) VS FEB +0.9 PCT (PREV +0.7 PCT) * US MARCH PERSONAL INCOME +0.5 PCT (CONS +0.4 PCT) VS FEB +0.4 PCT (PREV +0.3 PCT) * US MARCH CORE PCE PRICE INDEX +0.1 PCT (+0.1308; CONS +0.1 PCT) VS FEB +0.2 PCT (PREV +0.2 PCT) * US MARCH OVERALL PCE PRICE INDEX +0.4 PCT (+0.4022) VS FEB +0.4 PCT (PREV +0.4 PCT) * US MARCH YEAR-OVER-YEAR PCE PRICE INDEX +1.8 PCT VS FEB +1.6 PCT (PREV +1.6 PCT); CORE +0.9 PCT VS FEB +0.9 PCT (PREV +0.9 PCT) * US MARCH REAL CONSUMER SPENDING +0.2 PCT VS FEB +0.5 PCT (PREV +0.3 PCT) * US MARCH PERSONAL SAVING RATE 5.5 PCT VS FEB 5.5 PCT * US MARCH MKT-BASED PCE PRICE INDEX +0.4 PCT (FEB +0.5 PCT), CORE +0.1 PCT (FEB +0.2 PCT) * US MARCH MKT-BASED YEAR-OVER-YEAR PCE PRICE INDEX +2.1 PCT, CORE +1.0 PCT * US MARCH YEAR-OVER-YEAR PCE PRICE INDEX RISE LARGEST SINCE MAY 2010 (+2.1 PCT)

8:21AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "If you haven't noticed yet, which I find hard to believe, Main Street is getting its margins squeezed as more expensive food and energy prices are passed along by producers.

That perspective leaves the market wanting more details...we're in limbo on the big picture outlook. The positive vibes experienced in the holiday spending season are wearing off and the reality of a long, slow economic recovery is once again settling in...just like it did last year when the seasonal uptick in activity fil"

Mike Drews : "gmac .19 better"

Victor Burek : "flagstar about .1better than yesterday"

Matthew Graham : "it's not in the live update, but March's 5yr inflation expectations was 3.2. Then April's initial reading was 2.9 earlier this month and now we have Aprils final reading unrevised at 2.9. That make sense to all? no change versus preliminary, but improvement versus previous survey? (btw, feb and jan were also 2.9)"

Adam Quinones : "Japan is out for 黄金週間 (Golden Week) and London is shut down for the Royal Wedding. Add in event exhaustion and another high-risk event in the week ahead (Jobs Data)....and there isn't much reason to make a trade unless you're squaring a position to flatten out some risk. Volume in the bond market reflects that sentiment...."