MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:00 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:55PM :

Last Two Days This Week Have Market Moving Potential

Everything had been building up to the biggest potential market mover of the week: today's FOMC Announcement and subsequent press conference. But with those events having come and gone without ruffling the market's feathers too much, the last two days of the week take on renewed importance. That notwithstanding, they contain some important economic data anyway, as well as the last Treasury auction of the week tomorrow. The 830am time slot is busy, containing first quarter preliminary GDP and Jobless Claims on the econ data front, as well as Fed-Speak from Elizabeth Duke at the Community Affairs Research Conference in Arlington, VA. Pending Home Sales hits at 10am, followed by Fed-Speak from Lockhart at 12:40 and then the afternoon biggie: the 7 yr Treasury Auction results. With us as always will be the Fed Balance Sheet and Money Supply reports at 430pm. For a look at what Friday will add to that, as well as an overview of the rest of the week's economic events, see the link below.

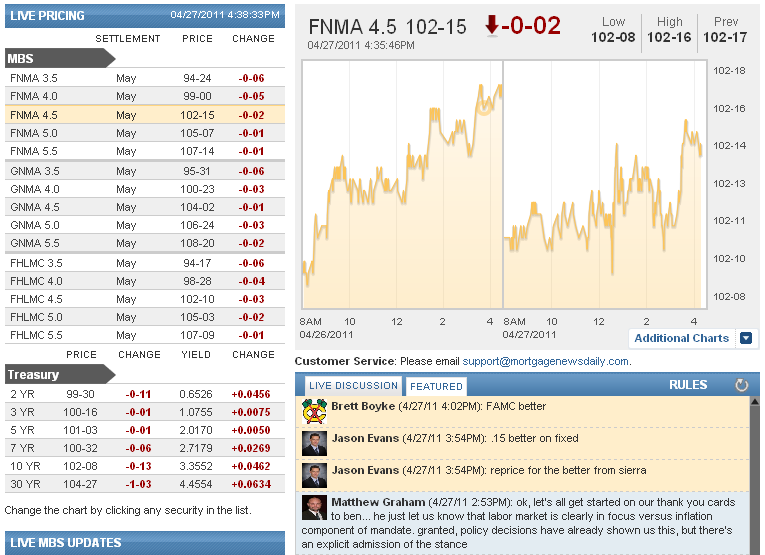

3:33PM :

MBS and TSYs Hold Support. Battling Back From Lows

One of the benefits if the previously mentioned narrow trading range in MBS today is that it's not too much to ask for prices to move from one extreme to the other. That's what has happened over the past 20 minutes as FNCL 4.5's moved from 102-10 to 102-14. Similarly, 10yr notes are down to 3.355 from their weakest levels of the day at 3.37. This effectively eliminates what had been a potentially increasing risk that we'd reach prices under 102-10 which could have prompted reprices for the worse.

3:10PM : Dual Mandate: Labor Market Trumps Inflation

A window into the Fed's decision making process perhaps... Although this could be well-inferred from previous verbiage and policy decisions, as far as the dual mandate of inflation and labor markets, Bernanke is making no pretense about which of those two components is in focus these days. In two separate parts of the Q&A, there were important comments that linked the separate mandate components as interdependent. When questioned about zero inflation, he responded: "Attempting to maintain inflation at zero will increase the risk of experiencing an extended bout of deflation or falling wages and prices, which in turn can lead employment to fall below its maximum sustainable level for a protracted period. The goal of zero inflation is not consistent with the Federal Reserve's dual mandate." Later in the session, he noted that "long term unemployment is the worst it has been in the post-war period," further saying that it is a "very significant concern" and "the reason the Fed has been so aggressive." This is a firm suggestion that developments in the labor market will continue to be the primary concern for the Fed and the primary driver of ongoing policy. the pace of improvement is still quite slow and we are digging ourselves out of a very, very deep hole. We are still something like 7 million plus jobs below where we were before the crisis and so clearly the fact that we are moving in the right direction, even though that is encouraging, doesn't mean that the labor market is in good shape. Obviously, it is not. We are going to have to continue to watch and hope that we will get stronger and increasingly strong job creation going forward."

2:47PM :

ALERT:

Negative Reprice Risk Increases as MBS Flirt With Lows

With the exception of the initial knee-jerk after the earlier FOMC statement, MBS just hit their lowest marks of the day at 102-10 in FNCL 4.5's. They've already ticked back up to 102-11, and as of now, there's no way to tell how this Q&A session will ultimately be traded, but any time MBS hit lows of the day, it constitutes a moderate increase in reprice risk. A caveat to that generality is that today's trading has been mostly contained in a mere 4 tick range. While reprices for the worse are probably not likely right now, we wanted you to be aware that prices had moved closer to riskier levels, and trading is active. We'll send another alert if we break 102-10.

1:51PM :

MBS Making up for Yesterday's Underpeformance vs TSYs

As markets gear up for the 2:15pm press conference, MBS and TSYs have improved just slightly. But Treasuries whereas MBS haven't had a sustained downtrend today, TSYs mostly worsened heading into the FOMC Announcement. That leaves MBS as the noticeable outperformer today. Current coupon spreads to the 10yr have tightened 3bps, almost exactly matching the amount by which they widened yesterday. FNCL 4.5's are down only 3 ticks at 102-14. 10yr notes are up just over 4bps at 3.3496. If MBS make it to 102-16, reprices for the better become a possibility, increasing in likelihood the longer or more stably that's achieved.

1:08PM :

FOMC Announcement out of the way, What's Next?

(Reuters) - The Federal Reserve signaled on Wednesday it is in no rush to scale back its extensive support for the U.S. economy and said a run-up in commodity prices that has dented growth should be fleeting.

The Fed's policy-setting Federal Open Market Committee said in a statement after a two-day meeting it intends to complete its $600 billion bond buying program in June as scheduled.

In the face of headwinds from high oil prices, the U.S. central bank said the economic recovery was proceeding at a "moderate pace" -- dialing back slightly from a statement in March when it said the economy was on "firmer footing."

It again expressed confidence a surge in the cost of oil and other commodities would be transitory and not spark a broader inflation.

"Inflation has picked up in recent months, but longer-term inflation expectations have remained stable and measures of underlying inflation are still subdued," it said.

There were few surprises in the Fed's statement and financial markets largely took it in stride. Stocks inched higher, the dollar held roughly steady and bonds cut losses.

"We did not expect any material surprises in the FOMC statement and there was none," said Bret Barker, portfolio manager at TCW in Los Angeles. "It remains quite dovish."

Nevertheless, the statement marked a near-conclusion -- at least for now -- of the massive expansion of the Fed's balance sheet that helped pull the economy out of its deep recession. The central bank said it would continue to reinvest proceeds from maturing securities it holds to keep its economic support in place.

The big question for investors, however, is what comes next.

Markets will look for clues in a question and answer session Fed Chairman Ben Bernanke will hold with journalists at 2:15 p.m. The briefing marks the first regularly scheduled news conference by a Fed chairman in the central bank's 97-year history.

12:48PM :

FOMC ANNOUNCEMENT RELEASED: NO SURPRISES

The Fed continues to note the "moderate pace" and "gradual improvement" of the economic recovery. While long term inflation continues to be seen as stable and underlying inflation "subdued," there was specific mention of inflation picking up in recent months. The Fed says it will continue to monitor inflation but for now sees even the underlying inflation metrics as "somewhat low, relative to levels that the committee judges to be consistent, over the longer run, with its dual mandate." The $600 billion of long term Treasury buying will continue and complete as scheduled, though the committee will continue to review those holdings and make adjustments based on new information "as needed." The statement specifically notes that it's "maintaining its existing policy of reinvesting principal payments from its securities holdings." This is an important consideration in determining what the Fed's role might be in acting as a buyer in the Treasury market. So we're essentially left with no change to previous verbiage, plus a slight acknowledgment of oil prices exerting pressure on short term inflation. Markets may show signs of fear surrounding that type of inflation at times, but the Fed is essentially saying "we don't see that as an issue but we'll let you know when/if that changes, and we'd do something about it if that happens." Bottom line: no surprises and open to interpretation. In light of the absence of groundbreaking comments, the press-conference later today and even the remaining economic data this week have NOT been rendered inconsequential by the Announcement and will have plenty of opportunities to move markets in the coming hours and days.

12:36PM :

New MBS Commentary Post

11:49AM :

TSYs Unwind Some Pre-Auction Concession. MBS at Highs

Both in the overnight session and in the last half hour before the auction, Treasury yields moved higher. This type of "concession" is a normal way that markets get in position for TSY auctions and not an alarming indication of broader momentum. The selling took 10 yr yields as high as 3.37, but the initial reaction to the auction brings yields right back to their previous range this morning between 3.355 and 3.345. FNCL 4.5's briefly touched their best mark of the day at 102-13, but are a tick off that now at 102-12. That's 5 ticks worse on the day and very much in line, albeit on the higher side, of the morning trading range. Both MBS and TSYs are effectively saying "bring on the Fed" as the 1230pm FOMC announcement and 215pm Press Conference continue to be the best candidates for market movers today.

11:45AM :

New MBS Commentary Post

11:33AM :

5yr Treasury Auction Results

* U.S. SELLS $35 BLN 5-YEAR NOTES AT HIGH YIELD 2.124 PCT, AWARDS 22.11 PCT OF BIDS AT HIGH * U.S. 5-YEAR NOTES BID-TO-COVER RATIO 2.77, NON-COMP BIDS $101.77 MLN * US TREASURY - PRIMARY DEALERS TAKE $17.04 BLN OF 5-YEAR NOTES SALE, INDIRECT $13.96 BLN

11:30AM :

Reprice Outlook: Rebate Flat into Lower MBS Indications

Even though "rate sheet influential" MBS prices are down 6/32, C30 loan pricing is basically unchanged today. This makes sense as most lenders were hesitant to reprice for the better yesterday, so there was some cushion in loan pricing to absorb weakness in the secondary market. That said, if FNCL 4.5 prices drop another 4-5 ticks from current levels...reprices for the worse will be likely. On the other hand, if FNCL 4.5 prices recover current intraday losses...rate sheets will be due about 0.125 in rebate.

11:17AM :

New MBS Commentary Post

11:15AM :

Pre-Auction Outlook: Decent Concession Baked In

Treasury is set to sell $35-billion 5yr notes. TAAPS cuts-off bids at 11:30am today instead of the normal 1pm deadline. This change was implemented to give traders an opportunity to prepare for the new FOMC meeting schedule where the Statement is released at 12:30 followed a press conference at 2:15pm (only 4x a year). In regard to the auction itself, here is some history. The bid to cover ratio is averaging 2.74 in the last five auctions. Dealers have had to increase their takedowns lately as bidside interest has generally declined. Dealers are adding near 52% of the competitive bid in the last five auctions. Direct bidders are averaging a 10% award while indirects have been awarded 38% of the issue on average. In terms of yields, 5s have "tailed" in five of the last six auctions. Tailed means the auction high-yield came in above the "When Issued" yield. This implies bidders were only willing to purchase supply at cheaper prices/higher yields. The "When Issued" yield is currently 2.116% vs. the OTR yield of 2.074%. Benchmark 5-yr yields have backed-up 6.1bps this AM. This is a decent size pre-auction concession and should provide incentive to "wave in" new inventory.

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Jason Evans : ".15 better on fixed"

Jason Evans : "reprice for the better from sierra"

Matthew Graham : "ok, let's all get started on our thank you cards to ben... he just let us know that labor market is clearly in focus versus inflation component of mandate. granted, policy decisions have already shown us this, but there's an explicit admission of the stance"

Matthew Graham : "BERNANKE-LONG-TERM UNEMPLOYMENT A VERY SIGNIFICANT CONCERN, A REASON FED HAS BEEN SO AGGRESSIVE "

Matthew Graham : "Bernanke mentions inflation expectations AGAIN"

Matthew Graham : " BERNANKE-TRADE-OFFS OF DOING MORE QE ARE GETTING LESS ATTRACTIVE AS INFLATION IS GETTING HIGHER"

Matthew Graham : "BERNANKE-WE WERE CLEAR IT WASN'T A PANACEA. BUT IT TURNED ECONOMY IN RIGHT DIRECTION "

Matthew Graham : "BERNANKE-CONCLUSION THAT QE2 WAS INEFFECTIVE CAN ONLY BE VALIDATED IF YOU THOUGHT THE STEP WAS A PANACEA "

Matthew Graham : "have to base that decision on evolving outlook"

Matthew Graham : "BERNANKE-AT SOME POINT IN OUR EXIT PROCESS, IT IS LIKELY AN EARLY STEP WOULD BE TO STOP REINVESTING"

Matthew Graham : "amount of securities to remain approximately constant"

Matthew Graham : " BERNANKE-LABOR MARKET OBVIOUSLY NOT IN GOOD SHAPE"

Matthew Graham : "WE WANT TO MAKE SURE LABOR MARKET RECOVERY IS SUSTAINABLE, IMPROVEMENT IN RECENT MONTHS "ENCOURAGING""

Matthew Graham : "BERNANKE-OUR VIEW IS THAT MOST LIKELY GAS PRICES WILL NOT CONTINUE TO RISE AT RECENT PACE"

Matthew Graham : "BERNANKE-NOT MUCH FED CAN DO TO TACKLE GAS PRICES PER SE, AT LEAST NOT WITHOUT DERAILING GROWTH"

Adam Quinones : "MARGIN SQUEEZE ON MAIN STREET!"

Matthew Graham : " BERNANKE-ESSENTIALLY ALL INCREASE IN DEMAND FOR OIL HAS COME FROM EMERGING MARKET ECONOMIES"

Matthew Graham : " FED'S BERNANKE-HIGHER GAS PRICES ADD TO INFLATION, BUT ALSO DRAIN PURCHASING POWER, BAD FOR RECOVERY"

Matthew Graham : "FED'S BERNANKE-GAS PRICES HAVE RISEN QUITE SIGNIFICANTLY, CREATING FINANCIAL HARDSHIP FOR A LOT OF PEOPLE "

Matthew Graham : "BERNANKE-DOLLAR FLUCTUATES, ONE FACTOR IN CRISIS WAS SAFE HAVEN EFFECT "

Matthew Graham : "BERNANKE-A STRONG, GROWING ECONOMY IS GOING TO BE GOOD FOR THE DOLLAR "

Andrew Horowitz : "xtended period meant to be purposefully Vague"

Matthew Graham : "BERNANKE-FED BELIEVES A STRONG, STABLE US DOLLAR IN AMERICAN, GLOBAL ECONOMY INTEREST "

Matthew Graham : "hmmm, commenting on dollar... interesting"

Matthew Graham : "BERNANKE-DON'T KNOW EXACTLY HOW LONG EXTENDED PERIOD LANGUAGE IS, SUGGESTS A COUPLE OF MEETINGS AT LEAST "

Matthew Graham : "BERNANKE-OUR EXPECTATION IS THAT INFLATION WILL COME DOWN TO A MORE NORMAL LEVEL "

Matthew Graham : "= pay attention to those consumer polls! fed actually cares!"

Matthew Graham : ""important for inflation expectations to remain well-anchored""

Matthew Graham : "BERNANKE-WE WILL BE LOOKING CAREFULLY TO SEE IF RECOVERY IS INDEED SUSTAINABLE, AS WE BELIEVE IT IS "

Matthew Graham : "good question, even if it was expected"

Matthew Graham : "he was just asked to quantify "extended period""

Matthew Graham : "BERNANKE-WE HAVE TAKEN OUR FORECAST DOWN JUST A BIT, TO TAKE INTO ACCOUNT POSSIBLY A BIT LESS MOMENTUM IN ECONOMY "

Adam Quinones : "said "possibly less momentum in the economy""

Adam Quinones : "haha he used "transitory" to describe the GDP slowdown."

Matthew Graham : "this is what the market is waiting for according to lackluster volume and directionality so far!!!"

Matthew Graham : "question time now"

Adam Quinones : "Stagflation or Stagnation...one or the other."

Matthew Graham : "this is worth a chuckle IMO... ben says inflation, bonds lose... ben says growth downgrade, bonds immediately turn around... spreads gap out as the opposing messages suggest opposite trades"

Adam Quinones : "TBAs illiquid. bid/ask spreads just gapped out. "

Matthew Graham : "slight downgrade to growth projection"

Matthew Graham : "FED SEES LONG-RUN PCE INFLATION AT 1.7-2.0 PCT (PVS 1.6-2.0 PCT); SEES JOBLESS RATE AT 5.2-5.6 PCT (PVS 5.0-6.0 PCT); SEES GDP AT +2.5-2.8 PCT (PVS +2.5-2.8) "

Matthew Graham : "FED SEES 2011 U.S. GDP AT +3.1-3.3 PCT (PVS +3.4-3.9 PCT); SEES 2012 AT +3.5-4.2 PCT (PVS +3.5-4.4 PCT); SEES 2013 AT +3.5-4.3 PCT (PVS +3.7-4.6) "

Adam Quinones : "from 3.4 to 3.9 to 3.1 to 3.3"

Matthew Graham : "FED SEES 2011 U.S. JOBLESS RATE AT 8.4-8.7 PCT (PVS 8.8-9.0 PCT); SEES 2012 AT 7.6-7.9 PCT (PVS 7.6-8.1 PCT); SEES 2013 AT 6.8-7.2 PCT (PVS 6.8-7.2) "

Matthew Graham : "FED SEES 2011 CORE PCE INFLATION AT 1.3-1.6 PCT (PVS 1.0-1.3 PCT); SEES 2012 AT 1.3-1.8 PCT (PVS 1.0-1.5 PCT); SEES 2013 AT 1.4-2.0 PCT (PVS 1.2-2.0) "

Adam Quinones : "downgraded GDP"

Adam Quinones : "really good observation Scott."

Scott Valins : "im with you guys - sat on that WSJ analysis for a moment and thought i'd share. i like your use of two very's to suggest how subtle the change is"

Brett Boyke : "from CNBC - Did The Fed Just Tip Its Hand To a Third Round of Easing?

Fed Chairman Ben Bernanke oversaw a tweaking of wording in the Fed’s post-meeting statement that had trading floors buzzing.

"

Adam Quinones : "door still wide open for downgrade though."