MBSonMND: MBS MID-DAY

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 11:01 AM EST | ||||||||||||||

Morning Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

10:51AM :

ALERT:

Possible Reprices for the Better Approaching

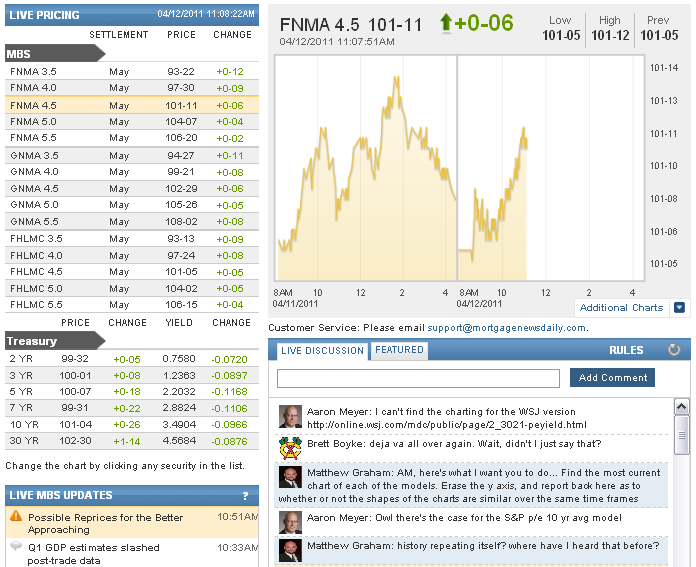

Though some lenders may reprice even at current levels, we'd expect more to get on board with any sort of sustained action around 101-12 in FNCL 4.5's. They're currently at 101-11 and have been rallying as 10yr notes toy with the 3.50 technical level. 10's are currently at 3.494 and have been closely tracking the progressive weakness in stocks. Same reprice philosophy as always: the longer these levels hold for MBS or the higher they go, the more likely reprices become. We've seen enough gains to get some reprices already from lenders who priced before 9:30am though.

10:33AM :

Q1 GDP estimates slashed post-trade data

(MarketWatch) -- The trade data for February has led several economists to mark down their already-battered estimates for first-quarter growth. Morgan Stanley slashed their estimate to 1.5% from 1.9% after what they called "a very weak report." RBS Securities cut their estimates to 1.7% from 2%, and adding that while some of the cooling reflects special factors, "the combination of slowing growth and rising prices puts the Fed in an increasingly uncomfortable position." RDQ Economics, which is waiting until Wednesday's retail sales report to adjust their numbers, said "the quarter is looking very soft from the expenditure side."

10:28AM :

MBS and TSY's at Best Levels, Stocks Near Lows

S&P's are down sharply on the day and continuing to slide, currently at their lows of the day at 1312.11 in S&P's, versus a 1324 close yesterday and nearly a 1319 high level so far this morning. Bonds are at their best levels of the day with 10's prodding through what had previously been resistance at 3.51, now at 3.505. FNCL 4.5's are up 14 ticks on the day at 101-09. Though lenders are normally a bit tentative with reprices for the better ahead of auction supply, lenders that were out with pricing early this morning may consider repricing for the better if current trends continue.

9:27AM :

Fed's Dudley and ECB's Stark Speaking in Hong Kong

*** -FED'S DUDLEY SAYS FIRST QUARTER U.S. ECONOMIC GROWTH WILL BE SOMEWHAT" DISAPPOINTING" 3 PERCENT OR LESS *** -FED'S DUDLEY SAYS THE RISK OF DEFLATION HAS GREATLY DIMINISHED *** -FED'S DUDLEY SAYS CONFIDENT THE ABILITY TO PAY INTEREST ON EXCESS RESERVES SUFFICIENT TO CONTAIN INFLATION *** -ECB'S STARK SAYS EXPECTS FIRST QUARTER ECONOMIC GROWTH TO BE A BIT STRONGER THAN EXPECTED IN THE EURO AREA AS A WHOLE *** -ECB'S STARK SAYS EXPECTS INFLATION RATE TO BE AROUND 2 PERCENT ON AVERAGE IN 2011 *** -FED'S DUDLEY SAYS NOT CLEAR STRENGTH IN U.S. EMPLOYMENT GAINS IN LAST FEW MONTHS WILL BE SUSTAINED *** -ECB'S STARK SAYS INTEREST RATE HIKE A STEP TOWARDS NORMALISATION *** -FED'S DUDLEY SAYS U.S. VERY FAR FROM WHERE IT WANTS TO BE ON EMPLOYMENT *** -FED'S DUDLEY SAYS IF U.S. CAN'T GENERATE STRONG JOB GROWTH SOON, WILL CAUSE LONG-TERM NEGATIVE ECONOMIC CONSEQUENCES *** -FED'S DUDLEY: IF INFLATION EXPECTATIONS GO UNANCHORED, WOULD BRING FORWARD TIMING OF POLICY EXIT VERY QUICKLY *** -FED'S DUDLEY: QE2 WAS NOT UNDERTAKEN TO WEAKEN THE DOLLAR

9:01AM :

Technical Levels and Reprice Targets for the Day

With the markets making directional movements this morning, reprice risk levels for MBS will largely be a factor of when a particular lender releases initial rate sheets. However, one level that stands out on the upside is 101-12. On the downside, this morning's rally helps 101-05 / 101-06 stand out as a 2 day low, though the recent "bottoming trend" in 4.5's bumped around in a 101-04 range on the 8th. Reading any significance into these levels would require this morning's strength to hold relatively steady, or improve. From a technical perspective, the general "positive vs. negative" trends should be better indicated by benchmark Treasuries. The 10yr tech of the day is more of a "band of yields" than one specific level. In early April, we've seen 3.51 act as resistance as yields attempt to rally lower, and in late March, heading into April, it's been the 3.50 mark that has most pertinent as support. It would be quite a feat for 10's to start making supportive bounces there ahead of the auction cycle produces at least it's first result of the week. On the upside anything around the mid 3.5's could be looked to for support, especially the long term target of 3.56. If things get super ugly, 3.60 is the last line of defense before the castle is breached.

8:39AM :

NFIB Survey: Hiring Up, Optimism Down in March

The Index of Small Business Optimism gave up 2.6 points in March,

falling to 91.9. Four components rose or were unchanged, while six lost

ground. The “hard” components of the Index (job creation, job openings,

capital spending plans and inventory plans) added two points while the

“soft” components (the other six in the table above) gave up 31 points.

Index was driven by weaker expectations for real sales gains and business

conditions and a marked deterioration in profit trends. The decline in the

percent of owners expecting higher real sales and better business

conditions in six months alone account for 76 percent of the decline in the

Index.

(see link for full report and charts)

8:32AM :

March import prices rise 2.7 pct

*** U.S. MARCH IMPORT PRICES +2.7 PCT (CONS. +2.2 PCT) VS FEB +1.4 PCT (PREV +1.4 PCT) *** U.S. MARCH EXPORT PRICES +1.5 PCT (CONS. +0.8 PCT) VS FEB +1.4 PCT (PREV +1.2 PCT) *** U.S. MARCH PETROLEUM IMPORT PRICES +10.5 PCT, LARGEST MONTHLY INCREASE SINCE +17.2 PCT IN JUNE 2009, VS FEB +4.0 PCT *** US MARCH YEAR-OVER-YEAR IMPORT PRICES +9.7 PCT, EXPORT PRICES +9.5 PCT *** U.S. MARCH NON-PETROLEUM IMPORT PRICES +0.3 PCT, YEAR-OVER-YEAR +4.1 PCT *** U.S. MARCH IMPORT PRICES RISE LARGEST SINCE MATCHING +2.7 PCT INCREASE IN JUNE 2009 *** U.S. MARCH FOOD IMPORT PRICES +4.2 PCT, LARGEST INCREASE SINCE +4.3 PCT IN JULY 1994

8:31AM :

Feb trade gap narrowed to $45.76 bln

*** US FEB TRADE DEFICIT $45.76 BLN (CONSENSUS $44.50 BLN) VS JAN DEFICIT $46.97 BLN (PREV $46.34 BLN) *** US FEB EXPORTS -1.4 PCT VS JAN +2.6 PCT, IMPORTS -1.7 PCT VS JAN +5.4 PCT *** US FEB GOODS DEFICIT $59.34 BLN, SERVICES SURPLUS RECORD $13.58 BLN *** US FEB EXPORTS $165.12 BLN VS JAN $167.54 BLN, IMPORTS $210.88 BLN VS JAN $214.51 BLN *** U.S. FEB CAPITAL GOODS IMPORTS $39.61 BLN VS JAN IMPORTS $41.70 BLN *** U.S.-CHINA FEB TRADE DEFICIT $18.84 BLN VS JAN DEFICIT $23.27 BLN *** US-OPEC FEB TRADE DEFICIT $9.38 BLN VS JAN DEFICIT $9.95 BLN *** US FEB OIL IMPORT PRICE $87.17/BBL VS JAN $84.34/BBL, +19.5 PCT FROM FEB'10 $72.92/BBL *** US FEB OIL IMPORT PRICE HIGHEST SINCE OCT 2008 ($91.73/BBL)

7:52AM :

New MBS Commentary Post

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Adam Quinones : "stabilized at lows Mike."

Mike Drews : "stocks attempting another break?"

Victor Burek : "at 5.25 i show .125 better, 5.0 to 4.75 a .25 better, and .4 better at 4.6 and 4.5"

Ken Crute : ".375% better on Conventional "

Scott Valins : "VB I see Flag as only .12 better"

Adam Quinones : "Short covering played a role in the AM bond market rally."

Adam Quinones : "S&Ps trying to move off overnight lows but finding it difficult."

Adam Quinones : "MBS market pretty thin right now. Drifting directionally with benchmarks. "

Matthew Graham : "thing about techs and MBS on a day like today is this: 1. the shorter the time frame you're looking at, the less pertinent it usually is. 2. MBS vs Treasuries = TSY's win, a lot. 3. Auctions coming up that will trump any short term developments. 4. 10's have some significantly more important techs in play with the 3.5 and 3.56 levels. "

Andy Pada : "Not really seeing an increase in purchase activity; I would describe as steady month over month"

Matthew Graham : "I wouldn't read hardly anything into short term techs in MBS"

Brent Borcherding : "Beginning of a flag on 4.5? "

John Rodgers : "however, everything I have is new construction. No resale."

Thomas Quann : "I am turning people down at the door for Purchases...."

Ken Crute : "every 1st time homebuyer shopping under $120k that needs a grant for down payment has somehow found my phone number "

John Rodgers : "Yes VERY BUSY with PURCHASES"

Brent Borcherding : "I'd say it is true AQ."

Victor Burek : "same here"

Ken Crute : "yes up tick in purchase apps "

Adam Quinones : "im hearing more and more about an uptick in purchase activity"

Adam Quinones : "....and now youre up to speed."

Adam Quinones : "1Q Earnings seen disappointing. "

Adam Quinones : "Dudley on wires doing the same in Hong Kong."

Adam Quinones : "Fed Vice-Chair Yellen on the wires repeating dovish tone. "

Adam Quinones : "German Investor Confidence Declines. UK inflation lower than forecast but still double the BoE's target. Nuclear Crisis elevated but has become long term problem. "

Adam Quinones : "NIKKEI failed key retrace level."

Adam Quinones : "techs were teetering on all out shift to bearish bias...but held the line yesterday. "

Adam Quinones : "3.60% support holds in 10yr."

Adam Quinones : "Risk Trade Off JR."

John Rodgers : "bring me up to speed, what is going on?"

Adam Quinones : "The front month light crude contract is -0.32% at 109.57. Gold is -0.34% at 1461.70. "

Adam Quinones : "We begin the day with benchmark 10s +14/32 at 100-24 yielding 3.532%, 5.5bps lower vs. yesterday's going out marks, and the yield curve bull flattening before Treasury auctions $32 billion 3-year notes. Overnight trading volume was strong with 250,000 10yr futures contracts trading hands as of 8AM. Also on the calendar are Import/Export Prices and the International Trade Balance at 830 followed by some hawkish rhetoric from the non-voting soon to be gone Kansas City Fed President Thomas Hoenig."

Adam Quinones : "i see 5.00-5.125"

Oliver S. Orlicki : "most banks are around 5.125%. "

Mike Drews : "where are you saying B/E is?"

Oliver S. Orlicki : "we need a nice little rally to bring down the BE to at least 5%. "

Adam Quinones : "ive got FNCL 4.5s at 101-04"

Adam Quinones : "s/be better this AM "

David Z. : "Good Morning. You guys suggest waiting for todays rates? I have 10 min to lock yesterdays rates."

Adam Quinones : "all good points VB...I might add this perspective on UK inflation...it is still double the BoE's target."

Adam Quinones : "Risk Off."

Victor Burek : "lots of favorable bond data from overseas last night... inflation down big in UK, retail sales plunge in UK and economic sentiment in germany drops much more than expected"