MBSonMND: MBS RECAP

| Open MBSonMND Dashboard | ||||||||||||||

|

|

|

||||||||||||

| Pricing as of 4:01 PM EST | ||||||||||||||

Afternoon Market Updates

A recap of MBS Market Updates provided by MND Analysts and streamed live to the MBSonMND Dashboard

.

3:33PM :

New MBS Commentary Post

3:06PM :

Treasuries Hit Their Close Within Support Target

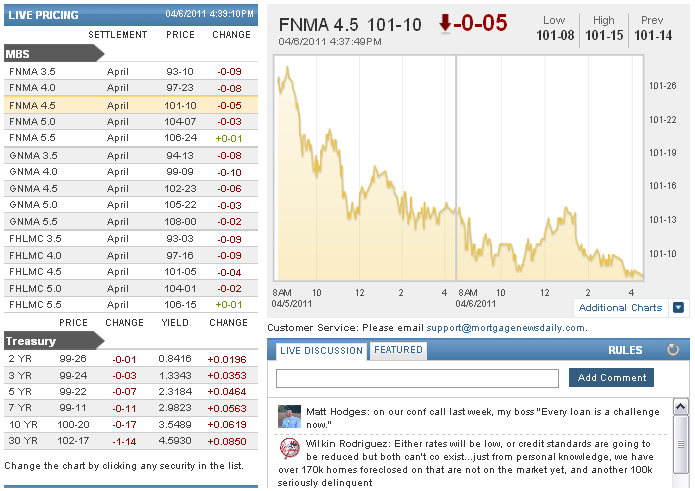

3pm... Time to mark Treasuries for the day. Despite a fairly heavy day of losses, volume has been average to light in 10yr notes and at 3pm yields just bounced at 3.55, 1 bp lower than their 3.56 target. Though near their lows of the day at 101-08, MBS have not experienced anything like the heavily directional move in benchmarks, but rather have simply returned near the lowest levels of the morning, currently down 6 ticks on the day at 101-09. Reprices for the worse remain a small possibility due to the heavy hits already seen on rate sheets over the past two days. As a reminder, Treasuries are "marked" for an official day-over-day figure at 3pm though they will keep trading. If 3.56 is tested or broken in the next 2 hours and if that occurs with relevant volume, we'll update you, but failing that, we're effectively looking at a move to a clearly defined target.

2:49PM :

Portugal says needs aid, PM to speak

LISBON, April 6 (Reuters) - Portugal's caretaker government said on Wednesday it needs financing from the European Union, marking a turnaround after resisting asking for aid for months despite sharply deteriorating financial conditions. Portugal's situation worsened last month after the government resigned, sending bond yields soaring, sparking a series of rating downgrades and a warning by local banks that they may no longer be able to buy government debt. "In this difficult situation, which could have been avoided, I understand that it is necessary to resort to the financing mechanisms available within the European framework," said Finance Minister Fernando Teixeira dos Santos. Prime Minister Jose Socrates was due to make a statement at 1900 GMT. Portugal's cost of credit has leapt since the minority Socialist government quit last month after a parliamentary defeat on tougher austerity measures, casting the country into political limbo. Earlier on Wednesday, the country issued 1 billion euros in treasury bills. The finance ministry said the auction was a confirmation of the deterioration caused by the rejection of the austerity measures. The government has held out hope previously that by steadily meeting budget goals and cutting spending it could regain investor confidence and avoid a bailout. In the latest threat to the government's resistance to seeking foreign financing, local banks warned the government on Monday that it must seek a short-term emergency loan to soothe market concerns ahead of the election, saying that under current conditions they cannot continue buying government debt. "There has been a very important signal from the banks for the future," said BNP Paribas analyst Ioannis Sokos. "Portugal can still make it through April, but probably won't get to June without a bailout." (Additional reporting by Shrikesh Laxmidas, Sergio Goncalves, Filipa Lima and Elisabete Tavares; Writing by Axel Bugge, Editing by Louise Ireland)

2:43PM :

QEII Effective at Lowering Borrowing Rates

NEW YORK – The Federal Reserve Bank of New York today released Large-Scale Asset Purchases by the Federal Reserve: Did They Work? The latest article in its Economic Policy Review series from the Research and Statistics Group.

The Federal Reserve’s large-scale asset purchases (LSAPs) made between late 2008 and March 2010 were effective in lowering longer term private borrowing rates, according to analysis in the report. While the effects of these purchases were especially noticeable in the mortgage market, they appear to be widespread, extending to markets for Treasury securities, corporate bonds and interest rate swaps. These findings suggest that monetary policy can still ease financial conditions when the Fed’s traditional policy instrument, the target federal funds rate, is set near its zero lower bound.

In this study, authors Joseph Gagnon, Matthew Raskin, Julie Remache and Brian Sack review the Federal Reserve’s experience with implementing the LSAPs between late 2008 and March 2010. They explain that the target fed funds rate was set as low as possible in December 2008. Thus, to further ease the stance of monetary policy as the economic outlook deteriorated, the central bank purchased substantial quantities of assets with medium and long maturities—housing agency debt, agency mortgage-backed securities (MBS) and Treasuries—to drive down private borrowing rates.

In their analysis, the authors show that by reducing the net supply of assets with long maturities, the purchases led to economically meaningful and long-lasting reductions in longer term interest rates on a range of securities. The reductions primarily reflect lower risk premiums, including term premiums. The LSAP programs had an especially powerful effect on longer term interest rates on agency debt and agency MBS by improving market liquidity and removing assets with high prepayment risk from private portfolios.

1:45PM :

ALERT:

Benchmarks Testing Support, May Pressure MBS

MBS have lost a few ticks recently and FNCL 4.5's are down 4 ticks on the day to 101-10. Benchmark 10yr yields tested 3.53 and has traded a few ticks higher, currently at 3.536. This weakness may be enough to ramp up risks of reprices for the worse, not widespread yet, but could get that way if MBS get to their lows at 101-08.

1:23PM :

MBS Turnin' the Screws as Bond Weakness Persists

The stock lever continues to be well-connected today. Stocks look to be putting in a reasonably firm bounce off yesterday's closing levels and bond yields are following quickly. 10'd have added over 1 basis point since stocks started to gain off the lows. MBS, however, have really ratcheted down spreads vs Treasuries. For a rough idea, 10yr notes are about 4bps higher in yield on the day while FNCL 4.5's are hovering around unchanged levels (currently 1 tick down on the day at 101-13). In terms of current coupon versus 10's, spreads are about 3bps tighter. So while the underlying movements in Treasuries are a bit of a cause for concern, the situation has not deteriorated in MBS at all. If stocks stall and 10yr yields fail to break earlier highs over 3.53, we may not be looking at any additional reprice risk, not that that's a major consolation considering how hard rate sheets have been hit over the past two days.

12:56PM :

Boehner, Obama discuss budget in phone call

WASHINGTON, April 6 12:42pm EDT (Reuters) - U.S. House of Representatives Speaker John Boehner told President Barack Obama in a three-minute telephone call on Wednesday morning that he remains hopeful that a deal can be reached to avoid a government shutdown, his office said.

"He told the President he remains hopeful a deal can be reached and that talks would continue," Boehner's office said in a prepared statement.

(Reporting by Andy Sullivan; Editing by Sandra Maler)

12:53PM :

How Many Borrowers Qualify for New ‘Safe’ Mortgage Rules?

(WSJ) About one in five mortgages purchased by Fannie Mae or Freddie Mac over the 1997-2009 period would meet the proposed standard of “safe” mortgages that would be exempted from costly new lending rules, according to a federal report published last week. Consumer advocates and the real-estate industry are preparing an all-out effort to soften new rules that they say create an overly conservative definition of “safe” mortgages that are exempted from costly new lending rules. To recap: The Dodd-Frank Act requires banks to hold 5% of the credit risk of mortgages that are bundled together and sold off as securities. The idea is that banks and other issuers of securitized loans won’t make poisonous mortgages if they have to eat some of their own cooking. But regulators also defined certain gold-standard loans that will be exempt from those rules, which were put out for public comment last week. The current debate is focusing on just where those lines should be drawn. Qualified loans would need to meet the following standards:

12:41PM :

GNMA Pooling Policy Update: Delinquent Loans

Ginnie Mae is changing its policy with regard to the pooling of Ginnie Mae mortgage-backed securities, prospectively. Ginnie Mae required any loans re-pooled in Ginnie I “X SF”, Ginnie II “M SF”, and Ginnie II “MJM” to be current at the issue date of the related securities. Effective for Single-Family securities with an issue date of June 1, 2011, and forward, all loans pooled in Ginnie Mae Single-Family securities, except for loans backing bond consolidation pools, must meet the following criteria: The mortgages in the related MBS pool may not be delinquent by more than the monthly installment of principal and interest that is due on the issue date (including the period beginning on the second day of the month preceding the issue date and ending on the issue date). For example, if the first payment due date is October 1, and if the issue date of the Single-Family security is January 1, then in order to be eligible for pooling, the October, November, and December payments must have been paid, and the only payment that may be due would be for the period December 2 through January 1.

12:17PM :

Consensus Emerges on Languishing Mortgage Apps...

“Rates were flat last week, but refinance activity fell, as the pool of borrowers who have both the incentive and the ability to qualify for a refinance continues to shrink.” said Michael Fratantoni, MBA’s Vice President of Research and Economics. Roughly 168 hours earlier, in the aptly titled piece : "Pool of Eligible Refinance Candidates Dried Up at Current Rates," we shared the following: "Recently lower mortgage rates have done little to motivate potential refinance candidates." said MND's Managing Editor Adam Quinones. "This isn't a big surprise as most qualified borrowers simply don't have an incentive to refinance because they already did last year when rates were near record lows. Other than that, qualification issues continue to prevent many folks from lowering their monthly payment. We do however expect a modest increase in purchase activity heading into the spring buying season." (incidentally, purchase apps picked up this week as refinance apps declined... Go figure...)

11:55AM :

Stocks, Bond Yields Off Highest Levels

In the absence of scheduled economic data today, stock prices and bond yields have had a fairly strong positive correlation. S&P's opened up just over 1339 but have since put in a series of lower highs and currently sit at 1333.31. Each of those lower highs corresponds with descending high yields in 10yr notes, 3.53+, then 3.52+, and most recently 3.517. MBS approve of the moderation, having gained back a few ticks, bringing the total day-over-day change in FNCL 4.5's to -0-03 at 101-11. Risks of reprices for the worse are now dwindling.

11:23AM :

US Republicans begin to chip away at Fannie, Freddie

(Reuters) - Republicans in the U.S. House of Representatives have started to chip away at mortgage finance giants Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB), taking the first legislative steps to reduce their role in the $10.6 trillion U.S. residential mortgage market. The House Financial Services subcommittee responsible for overseeing Fannie Mae and Freddie Mac approved eight narrowly crafted bills late on Tuesday and early Wednesday targeting the two firms, including one that would sharply cut the pay of their executives. Republicans are pushing hard to curtail the role the two government-controlled firms play as part of a broad effort to scale back the government's role in housing. Democrats are more sympathetic to a continued, but smaller, government role. The votes, largely but not entirely along party lines, marked the first concrete steps in what is expected to be a years-long process of winding down Fannie Mae and Freddie Mac. ((Reporting by Corbett B. Daly; Editing by Dan Grebler)

11:22AM :

New MBS Commentary Post

11:15AM :

IMF urges US budget include Fannie, Freddie costs

(Reuters) - The United States should include in its budget the cost of mortgage loan guarantees and other housing supports, the International Monetary Fund said on Wednesday in a rare criticism of its biggest shareholder. The IMF's findings may land it squarely in the middle of a hot political debate over what to do about Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB), the mortgage finance giants that back most new housing loans. The IMF also faulted the Obama administration for failing to address the tax deduction for mortgage interest, which it called "both expensive and regressive." The tax break is hugely popular, and eliminating it would no doubt cause political pain at a time when the Obama administration is already preparing for the 2012 presidential election campaign. The IMF did say that the weak U.S. housing market still needs government guarantees for securitized mortgages, and abruptly removing those support could be damaging. "However, government guarantees should be explicit and fully accounted for on the government's balance sheet," it said. (Reporting by Emily Kaiser)

Featured Market Discussion

A recap of the featured comments from the Live Discussion on the MBSonMND Dashboard

.

Matthew Graham : "let's put it this way. 3.56 has been a topic of conversation since post-Japan-related FTS left 3.25 standing as resistance, in that bonds need a retreat to higher levels and reestablish (potentially) new longs."

Chris Kopec : "Would it be an oversimplification to say the market is telling Bernanke that they don't believe his "transitory" view on inflation is accurate?"

Matthew Graham : "yeah, and their driving makes me carsick..."

Adam Quinones : "this is all driven by techs."

Matthew Graham : "Stocks slowly plodding upward. 10's only a bp away now from reaching out and touching 3.56 target"

Matthew Graham : "A lot of us have had vocal opinions on whether or not QE2 has been "good or bad" for our industry. FRBNY Economists put that topic in focus this month and it's linked in the latest live update."

Adam Quinones : "hey everyone I just put up a post on the government shutdown as it relates to housing: http://www.mortgagenewsdaily.com/04062011_government_shutdown_hud.asp"

Matthew Graham : "treasuries breaking away from stocks now... yields rising faster than stocks rally. situation possibly compounded at the moment by technical implications of S&P holding 1330's as support"

Matthew Graham : "in other news, GSE's and HUD have banned all refinances citing that it is now impossible to establish "benefit to borrower.""

Jill Statz : "so AQ said that the IRS could possibly shut down...that would bring the Mtg industry to a halt also...no way to do 4506-T's!!! "

Bromi Krock : "Hey MG, I would love to give you my best ex rate but I don't know how to read my rate sheet anymore. LMAO"

Matthew Graham : "There comes a time where even crusaders of outlying view points must acquiesce to some form of compromise in the interest of achieving as much of their goal as possible, based on the realization that ongoing ardency will largely destroy it"

Matthew Graham : "Our politicians really just don't understand the economy, or at least not to the extent that's necessary in order to play with the sort of fire they do"

Matthew Graham : "I wish I could believe it was MERELY due to politics, but I think it speaks to a more long-standing and much more devastating problem"

Matthew Graham : "hypocrisy at its finest? for the sake of political posturing?"

Matthew Graham : "the opposite?>"

Matthew Graham : "what will the result be of the stubborness?"

Bert Swyers : "it is politcal posturing nothing else"

Matthew Graham : "to, in some way, improve the economic picture?"

Matthew Graham : "what's the purported REASON behind the ardent views of proposed budget cutters"

Chris Kopec : "MG....you are not alone. Brings me back to my point about Bill Gross. He's venting on the government, just using a critique of treasuries to do it."

Matthew Graham : "Does anyone else feel like we're witnessing a quintessential example of cutting of noses to spite the face?"

Adam Quinones : "ha very funny perspective. mortgage banker trying to recruit mortgage broker: http://www.youtube.com/watch?v=qacLXkyRtIQ hat tip CD."

Adam Dahill : "Yup, need to raise the rate. It's going to suck to be a consumer. Banks are squeezing the Broker"

Jason Zimmer : "you can no longer choose to make less"

Jason Zimmer : "so what happens when if ysp goes down when you float? you have to raise rate or have borrower pay more CC."

Adam Dahill : "pull through % are going to get crushed. Investors should offer portfolio locks of 60 days upon submission. No need to float then"

MMNJ : "with the higher % of LO's locking vs floating, pullthru percentages with the investors are going to clocked with any 25 bps rally in rates"

Jason Zimmer : "true AD, but in the past we could absorb ysp if anything changes, now we can't. everything HAS to get passed to the borrower"

Adam Dahill : "Only reason to float these days is if your closing is too far out to lock and you want to protect yourself from clients wanting a better rate when they are within 30 days of closing"