We had a rush of new data on screens this morning. Below are brief recaps of the reports followed by comments and a market update.

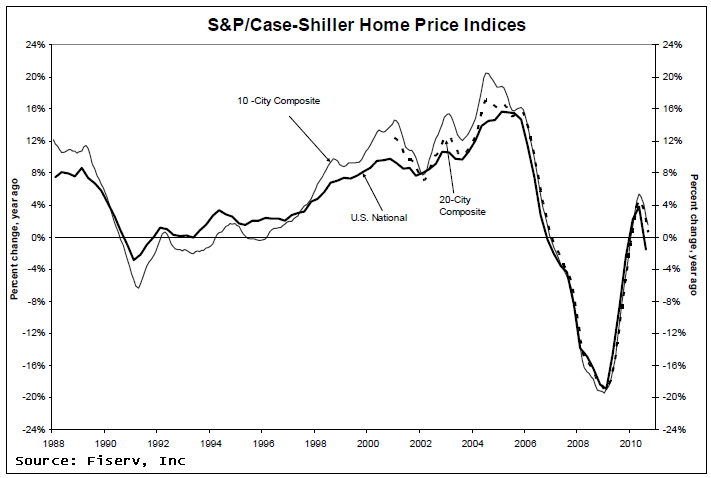

9AM S&P Case-Shiller Home Price Index....

RTRS-US SEPT HOME PRICES IN 20 METRO AREAS -0.8 PCT SEASONALLY ADJ (CONSENSUS -0.3) VS AUG'S REVISED -0.5 PCT-S&P/CASE-SHILLER

RTRS-US SEPT 20-METRO AREA HOME PRICES -0.7 PCT (CONSENSUS -0.2) VS REVISED -0.2 PCT IN AUG - S&P/CASE-SHILLER

RTRS-US SEPT 20-METRO AREA HOME PRICES +0.6 PCT (CONSENSUS +1.1 PCT) FROM YEAR AGO -- CASE-SHILLER

RTRS-US SEPT HOME PRICES IN 10 METRO AREAS -0.7 PCT SEASONALLY ADJUSTED VS REVISED -0.3 PCT IN AUG - CASE-SHILLER

RTRS-US HOME PRICES IN 10 METRO AREAS -0.5 PCT IN SEPT VS -0.1 PCT IN AUG - S&P/CASE-SHILLER

RTRS-US SEPT HOME PRICES IN 10 METROPOLITAN AREAS +1.6 PCT FROM YEAR AGO - S&P/CASE-SHILLER

RTRS-US HOME PRICES IN Q3 2010 -2.0 PCT FROM Q2 2010 - S&P/CASE-SHILLER NATIONAL INDEX

RTRS-US HOME PRICES IN Q3 2010 -1.5 PCT FROM Q3 2009 - S&P/CASE-SHILLER NATIONAL INDEX

RTRS-U.S. Sept home prices fall faster than expected

Plain and Simple: Case-Shiller says the deceleration of the home price recovery has been confirmed

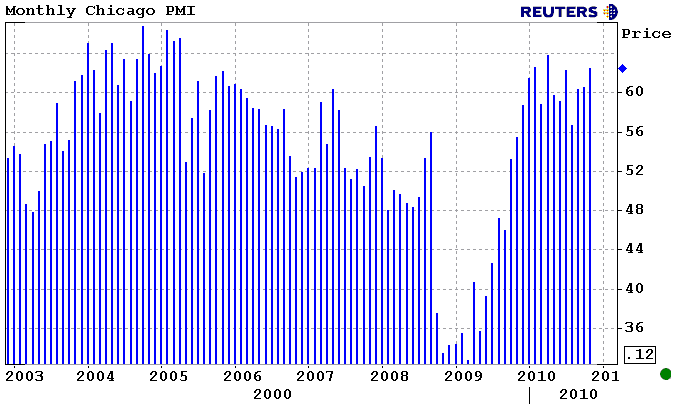

945AM Chicago Purchasing Managers Index...

RTRS-CHICAGO PURCHASING MANAGEMENT INDEX 62.5 IN NOVEMBER (CONSENSUS 60.0) VS 60.6 IN OCTOBER

RTRS-CHICAGO PURCHASING MGMT NEW ORDERS INDEX 67.2 IN NOVEMBER VS 65.0 IN OCTOBER

RTRS-CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX 70.7 IN NOVEMBER VS 68.9 IN OCTOBER

RTRS-CHICAGO PMI EMPLOYMENT INDEX 56.3 IN NOVEMBER VS 54.6 IN OCTOBER

RTRS-CHICAGO PURCHASING MANAGEMENT PRODUCTION INDEX 71.3 IN NOVEMBER VS 69.8 IN OCTOBER

RTRS-CHICAGO PURCHASING MANAGEMENT INDEX AT HIGHEST SINCE APRIL 2010

RTRS-CHICAGO PURCHASING MANAGEMENT NEW ORDERS INDEX AT HIGHEST SINCE MAY 2007

RTRS-CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX AT HIGHEST SINCE APRIL 2010

RTRS-CHICAGO PURCHASING MANAGEMENT PRODUCTION INDEX AT HIGHEST SINCE APRIL 2005

Plain and Simple: the Fed's GDP outlook indicates we should be expecting an uptick in economic activity in the year ahead. This data is a precursor to that prediction. The problem is retailers and product sellers don't have much pricing power (must sell at discounts) nor do they have stable demand. With unemployment stubbornly high, the rising cost of inputs can't be passed along to the consumer level and firms will be forced to trim other expenses (temporary hiring) or accept thinner profit margins. READ MORE ABOUT THE FED'S ECONOMIC PROJECTIONS

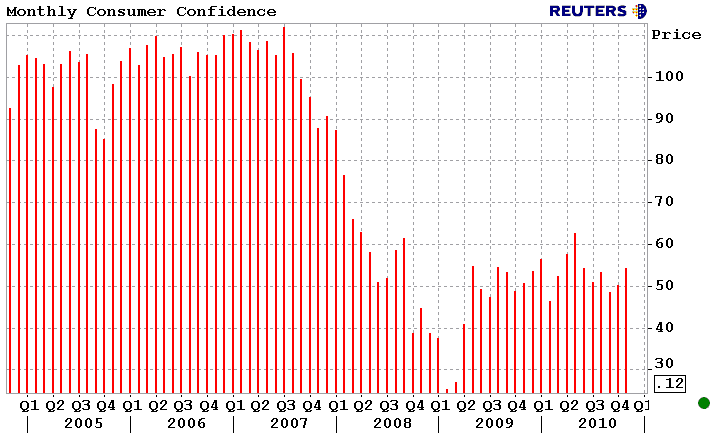

10AM Consumer Confidence...

RTRS-US NOVEMBER CONSUMER CONFIDENCE INDEX 54.1 VS OCT REVISED 49.9 (PREVIOUS 50.2) - CONFERENCE BOARD

RTRS-US CONSUMER CONFIDENCE INDEX MEDIAN FORECAST FROM REUTERS FOR NOVEMBER WAS 52.6

RTRS-US CONSUMER PRESENT SITUATION INDEX IN NOV 24.0 VS OCT REVISED 23.5 (PREVIOUS 23.9)

RTRS-US CONSUMER EXPECTATIONS INDEX 74.2 IN NOV VS OCT REVISED 67.5 (PREVIOUS 67.8) -- CONFERENCE BOARD

RTRS-US JOBS HARD-TO-GET INDEX 46.5 IN NOV VS OCT REVISED 46.3 (PREVIOUS 46.1) -- CONFERENCE BOARD

RTRS-US 1-YEAR CONSUMER INFLATION RATE EXPECTATIONS 5.1 PCT IN NOV VS OCT 5.0 PCT

RTRS-US NOVEMBER CONSUMER CONFIDENCE INDEX AT HIGHEST SINCE JUNE 2010

RTRS-US CONSUMER EXPECTATIONS INDEX AT HIGHEST SINCE MAY 2010

Plain and Simple: the housing market benefits from rising consumer confidence. The bad news is we don't think housing has hit a bottom in many markets, this is expected to prevent the purchase market from making substantial positive progress in the winter months. Think of it this way....The recovery is a mountain and we're all jammed into one Ford Festiva, trying to reach the top. The housing market is a grand piano and it's strapped to our bumper. The same can be said about the labor market. READ MORE

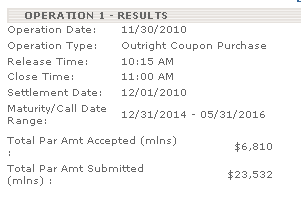

1015AM QEII Treasury Purchases...

RTRS-NY FED SAYS BUYING TREASURIES WITH MATURITIES RANGING FROM DECEMBER 2014 TO MAY 2016

Plain and Simple: Don't miss the Plain and Simple's above.

Market Reaction...

Although we experienced a modest rally retracement heading into the release of Case-Shiller and following Chicago PMI and Consumer Confidence, the overnight flight to safety rally remains in tact. We're not far from the best levels of the session but the 10yr note has already failed to breach 2.75% resistance twice and bullish momentum has faded into higher price levels.If stocks can muster the energy to bounce from 2-week lows, we could see rates backup from here and retest 2.79/2.80. The stock lever is affecting the flight to safety into the bond market.

Production MBS coupon prices are off their best levels of the day as well. The cash FNCL 4.0 is currently +5/32 at 101-21, down from a high of 101-27. "Rate sheet influential" MBS coupons are lagging benchmark TSYs as swaps gap out vs. the curve, but we're off the wides of the day thanks to a fast$ down in coupon MBS bid (into the bull flattener). Rob (Chrisman) and I had a conversation last night about the poor loan pricing that was offered by lenders yesterday, we both came to the conclusion that desks overhedged last week and passed along higher hedging costs to consumers yesterday. Lock desk hedging has been slow recently and trading desks report much buying back of hedges, this is likely a factor of secondary overselling their position last week. Not to worry...I haven't updated my model yet but anecdotal feedback indicates loan pricing is greatly improved today.

Again..beware of the stock lever. Just in case you missed the Plain and Simple after Chicago PMI data, here it is again...

Plain and Simple: the Fed's GDP outlook indicates we should be expecting an uptick in economic activity in the year ahead. This data is a precursor to that prediction. The problem is retailers and product sellers don't have much pricing power (must sell at discounts) nor do they have stable demand. With unemployment stubbornly high, the rising cost of inputs can't be passed along to the consumer level and firms will be forced to trim other expenses (temporary hiring) or accept thinner profit margins. READ MORE ABOUT THE FED'S ECONOMIC PROJECTIONS