The Thanksgiving slowdown prevented me from posting the Federal Reserve's updated economic forecast.

The Fed's Summary of Economic Projections are released once a quarter. They are attached to the minutes of four of the Committee’s FOMC meetings and are intended to convey information about FOMC participants’ assessments of their statutory economic targets.

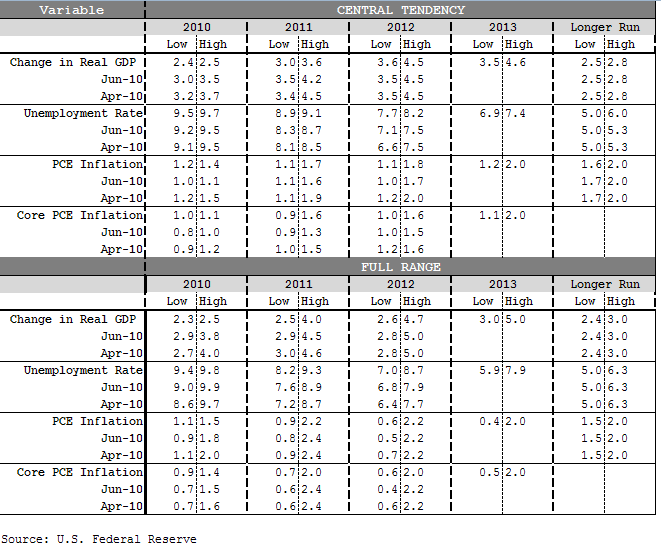

Projections are provided for output growth, unemployment, and inflation for the years 2010 to 2013 and over the longer run. They are based on information available through the end of the meeting and on each participant’s assumptions about factors likely to affect economic outcomes, including his or her assessment of appropriate monetary policy. Longer-run projections represent each participant’s assessment of the rate to which each variable would be expected to converge over time under appropriate monetary policy and in the absence of further shocks. “Appropriate monetary policy” is defined as the future path of policy that each participant deems most likely to foster outcomes for economic activity and inflation that best satisfy his or her interpretation of the Federal Reserve’s dual objectives of maximum employment and stable prices.

FOMC participants’ projections of economic activity over the next several years indicated that they expected the economic recovery to continue, with unemployment declining slowly and inflation remaining subdued. Relative to their previous projections in June, participants saw weaker real activity this year and expected a somewhat more gradual economic recovery over the next several years.

Most participants expected the unemployment rate would slowly decline over the forecast horizon, while the rate of inflation would edge up but stay subdued. Participants generally indicated that the pace of expansion in real gross domestic product (GDP) would rise over the projection period to one that was somewhat above their assessment of the economy’s longer-run rate of growth. They judged that the pickup in economic activity would be spurred in part by accommodative monetary policy and a gradual easing in credit conditions that would help buoy spending by consumers and businesses. Stronger spending, in turn, would lead to improved confidence in the economy, a pickup in hiring, and a further improvement in credit conditions—forces that would continue to support spending.

But participants thought that several factors would likely continue to restrain economic growth for a while, including a high degree of caution exhibited by consumers and businesses, persistent weakness in the residential and commercial real estate sectors of the economy, and still-tight credit conditions. Somewhat more than half of the participants judged that, in the absence of any additional shocks to the economy, the economy would converge fully to its longer-run rates of output growth, unemployment, and inflation within about five or six years; the rest indicated that it could take longer for unemployment to fall back to its longer-run rate or for inflation to rise back to the level they deemed desirable in the longer run.

Participants continued to attach an unusually high degree of uncertainty to their projections

The table below summarizes the FOMC's range of projections. The first row of data under each variable is the most recent estimate. The central tendency excludes the three highest and three lowest projections for each variable in each year. The range for a variable in a given year consists of all participants’ projections, from lowest to highest, for that variable in that year. Longer-run projections for core PCE inflation are not collected.

NOTE: Projections of change in real gross domestic product (GDP) and in inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated. PCE inflation and core PCE inflation are the percentage rates of change in, respectively, the price index for personal consumption expenditures (PCE) and the price index for PCE excluding food and energy. Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated. The June projections were made in conjunction with the meeting of the Federal Open Market Committee on June 22–23, 2010.

Plain and Simple: Although they cut their output forecast, the Fed still expects a noticeable GDP improvement in 2011 from 2010. This uptick in total output is expected to occur without a major recovery in the labor market or an increase in core inflation metrics (no pricing power). This means, if the Fed is right, we will be leaving some folks behind on the road to recovery. That's why I am calling it a "segmented recovery". My point is, the Fed is pretty optimistic about an uptick in activity during 2011, if this forecast isn't met, we might be talking about more Quantitative Easing sometime down the road, especially if the unemployment rate stays in the 7-10% range into 2012. Last but not least, notice the last sentence in the SEP excerpt..."Participants continued to attach an unusually high degree of uncertainty to their projections"...this is one of the main reasons why market participants are reluctant to allocate capital to long term projects and investments. UNCERTAINTY IS ABUNDANT!!! It's a trader's world, we're just living in it.....

FOMC Minutes: The Road to Recovery is Long and Paved with Uncertainty