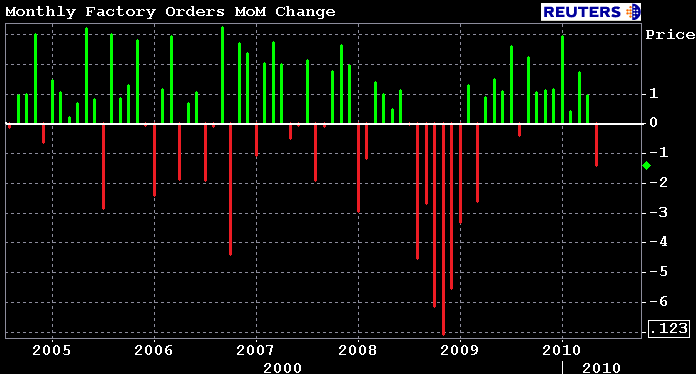

The final economic release of the week is out. New Factory Orders in May declined 1.4% after a 1.0% improvement in April. This was worse than expected (-0.5%) and the biggest drop in new orders since March 2009. That headline may seem bearish but as the chart below shows, this was first month over month contraction since August 2009. Other than that the manufacturing sector steadily recovered in 2009 into 2010. But will it continue...

Here is a recap of the rest of the report.

Price action has been whippy since NFP data was released. If you factor out choppy movements, stocks are still viewed from a bearish perspective and interest rates are retaining the risk averse flight to safety bid.

S&Ps are currently -6.25 at 1015.50. While this is a new intraday low, S&Ps are still within the the range seen yesterday.

The 10 year note is behaving in a similar manner, chopping about a contained range. The long term trendline and fibonacci fan I called attention to last week have served as inflection points all week. Support is steady at 2.98%. A break of this level would lead to a test of 3.02%.

Mortgages are trading in light volume with minimal supply on screens. The range trade is obvious in the chart below. The August delivery Fannie Mae 4.0 MBS coupon is -0-01 at 100-30. The August delivery Fannie Mae 4.5 MBS coupon is -0-01 at 103-07. The secondary market current coupon is less than one basis point lower at 3.817%. Current coupon yield spreads are unchanged vs. TSYs and slightly tighter vs. swaps.

All week the FN 4.0 has shown signs of exhaustion, especially as prices attempted to break into the 101 handle. MBS prices are rich and due a relief sell-off (relief from the threat of negative convexity)...if they don't get that relief you should expect mortgage rates to lag benchmark rate rallies. READ MORE

I'm getting mixed reads on loan pricing this morning. The lenders I study (majors) improved rebate marginally but originator accounts say otherwise. Either way loan pricing is still stupid aggressive. I offered THIS EXPLANTION last night. Secondary has likely added extra margin to rates this morning...they need some time to sort through all the new locks this week.

Investor attention is clearly focused on holiday festivities and soccer games. This is apparent via below average trading volumes. Wave in the weekend already!