- JULY FNCL 4.0: +02 at 101-11 (101.344) AUGUST FNCL 4.0: +02 at 101-00 (101.00)

- Secondary Market Current Coupon: -0.9 bps at 3.82%

- CC Yield Spreads:+86.6bps/10yTSY. +79.0bps/10yIRS. SPREADS CLOSED WIDER BUT WELL OFF WIDES OF DAY

- UST10YR: +2.0bps at 2.954%. 2s/10s: 1bp FLATTER at

232bps. 3YR NOTE= WORST PERFORMER

- S&P CLOSE: -0.32% at 1027.37 HIGH: 1033.63 LOW: 1011.52 WORST SECTOR: Financials -0.85%

While stocks plunged and benchmark 10yr note yields fell to levels not seen since the end of the world was seemingly upon us last spring...the August FN 4.0 looks to have found a firm ceiling in the 101-00 handle. Production MBS coupons are now exhibiting the behavior of a worn out warrior. Valuations have been falling further behind as the week has progressed (yield spreads are wider!). Sigh. Exhaustion!

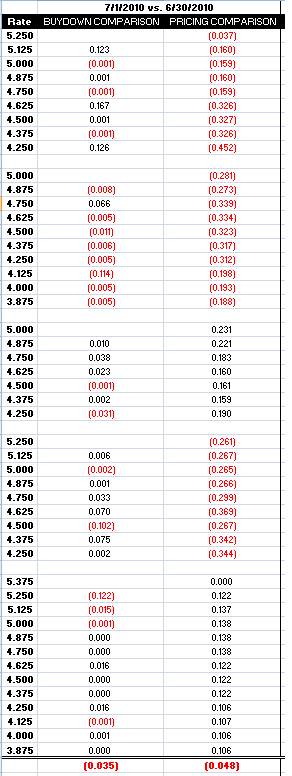

Below is a snapshot comparison of loan pricing today vs. loan pricing yesterday. Notice interest rate rebate reductions and buydown cost increases were most significant in the lower note rates. Also notice that rebate improvements were most significant in note rates above 4.75%.

This is because note rates at or below 4.75 are being sold forward into 4.0 MBS coupons....these coupons are the most sensitive to a back up in benchmark rates at the moment.

If you're floating you should be conscious of this observation, especially if you're writing a note rate close to par. These mortgage rates are the most sensitive to falling "rate sheet influential" MBS prices. The further away you're priced from par, the less sensitive your rebate will be to falling MBS prices.

If we're really headed for a double dip recession, interest rates will surely move lower. I'm just not sure mortgage rates will follow...

WHY?

It's a factor of how mortgage notes are delivered into MBS coupons. The lowest note rate that can be used to fulfill a 4.0 trade: 4.25%. If the lender wants to sell forward a 4.125% note rate in the TBA MBS market, they'd have to sell it as a 3.50 MBS coupon. Well, because there was never liquidity in the 3.5 MBS market, at least not for anyone looking to sell forward their pipeline "IN SIZE", mortgage rates haven't been able to make a solid push toward 4.00%. Read liquidity as: A seller being able to find a willing buyer without having their offer price hit badly because there were no other willing buyers (buyer's market).

Right now the 3.50 MBS market is considered "phantom" (8 tick bid ask spread?), there aren't enough buyers out there who are willing to take on the added extension risk, so the lowest rate lenders are offering consumers : 4.25%! In the short term, mortgage rates are above 4.25%, so there is room to improve if 10s keep on rallying.

Besides all out depression, I'm not sure what would drive the TBA MBS market to trade 3.50 MBS (the Fed?). My best guess: 10s need to range trade somewhere between 2.65% and 2.85% (probably closer to 2.50% once the street realizes refinances aren't what they've been expecting). Even then I find it hard to believe dealers would be willing to take on that much extension risk without tagging sellers with a hefty price discount.

What does all this mean?

The risks of floating greatly outweigh the rewards.

Tomorrow is the start of a long weekend and the JV team will be manning the desk as decision makers exit early to jockey for position on the Jitney. So from an administrative point of view, tomorrow doesn't look like the right time to catch the falling knife (stocks). I bet secondary would love to see MBS prices take a breather though...I can't imagine long standing pipeline hedges (pull-through) are performing all that well at the moment. With that in mind, even if benchmark yields rally and MBS prices follow from a widening distance....you should expect to see a fatter pipeline control cushion baked into your loan pricing (if MBS prices move higher). See thoughts above re: falling MBS prices.